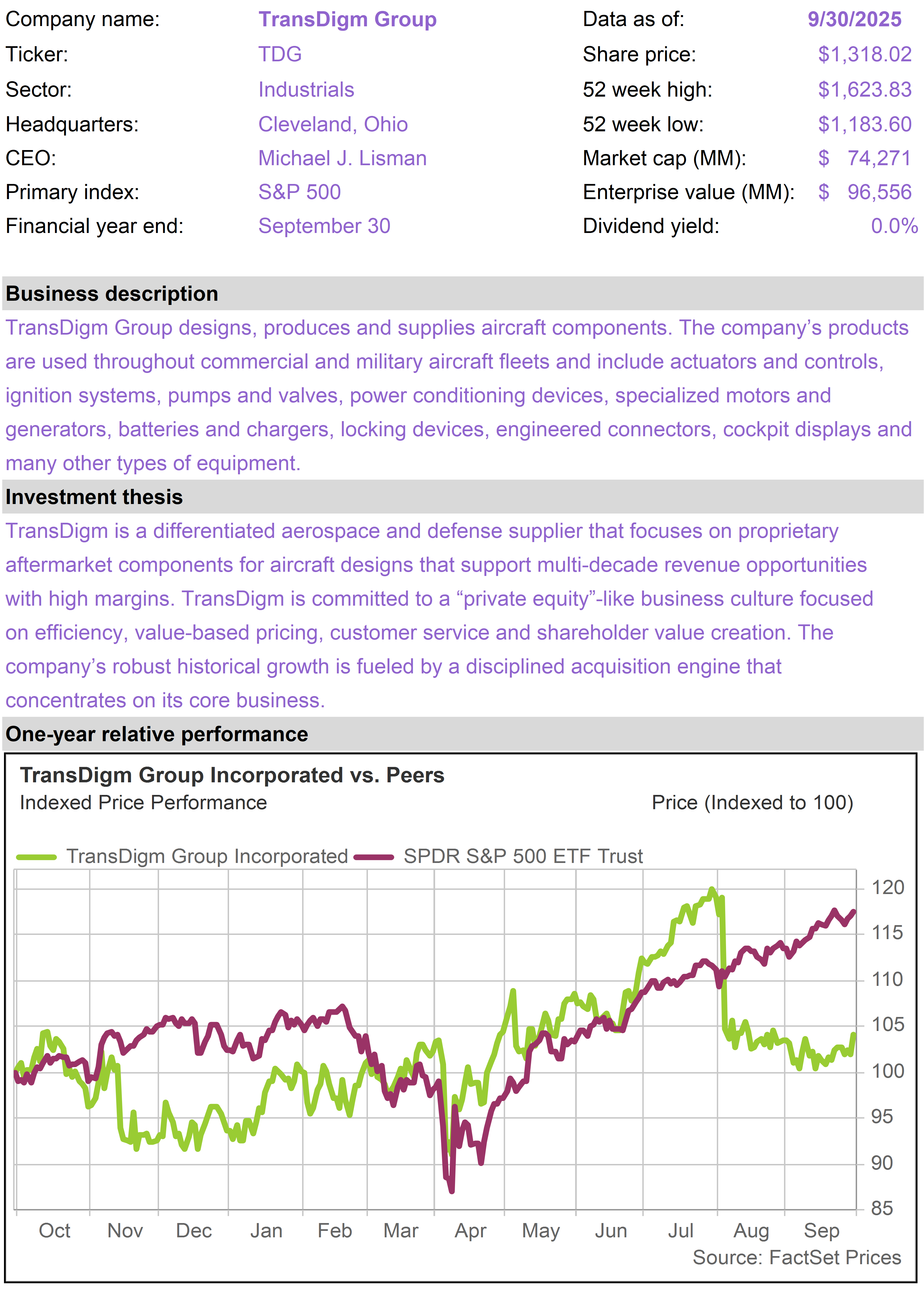

|

|

| Inflation Protection Model Portfolio |

|

| Monthly Portfolio Review: September 2025Publication date: October 3, 2025 |

|

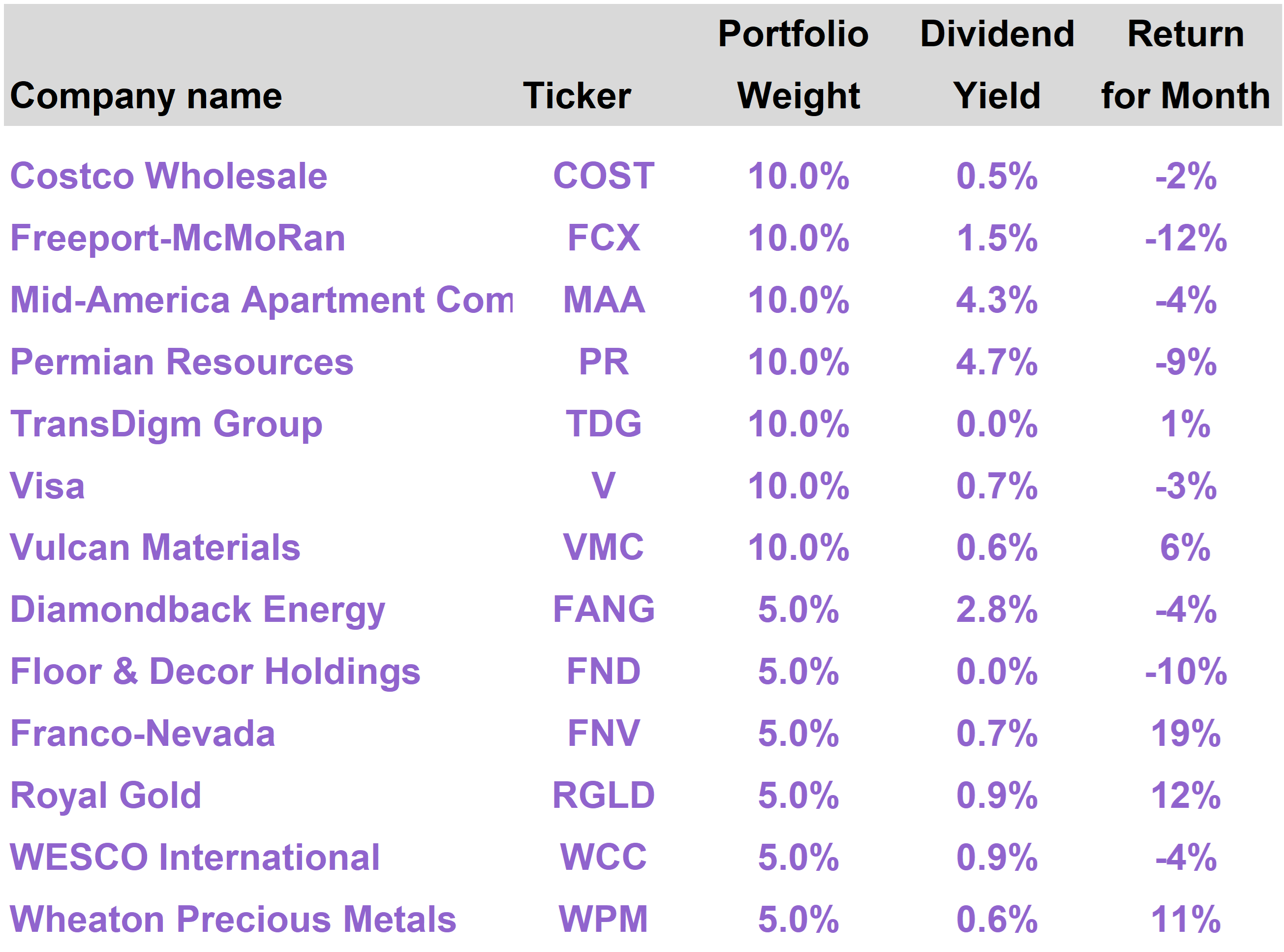

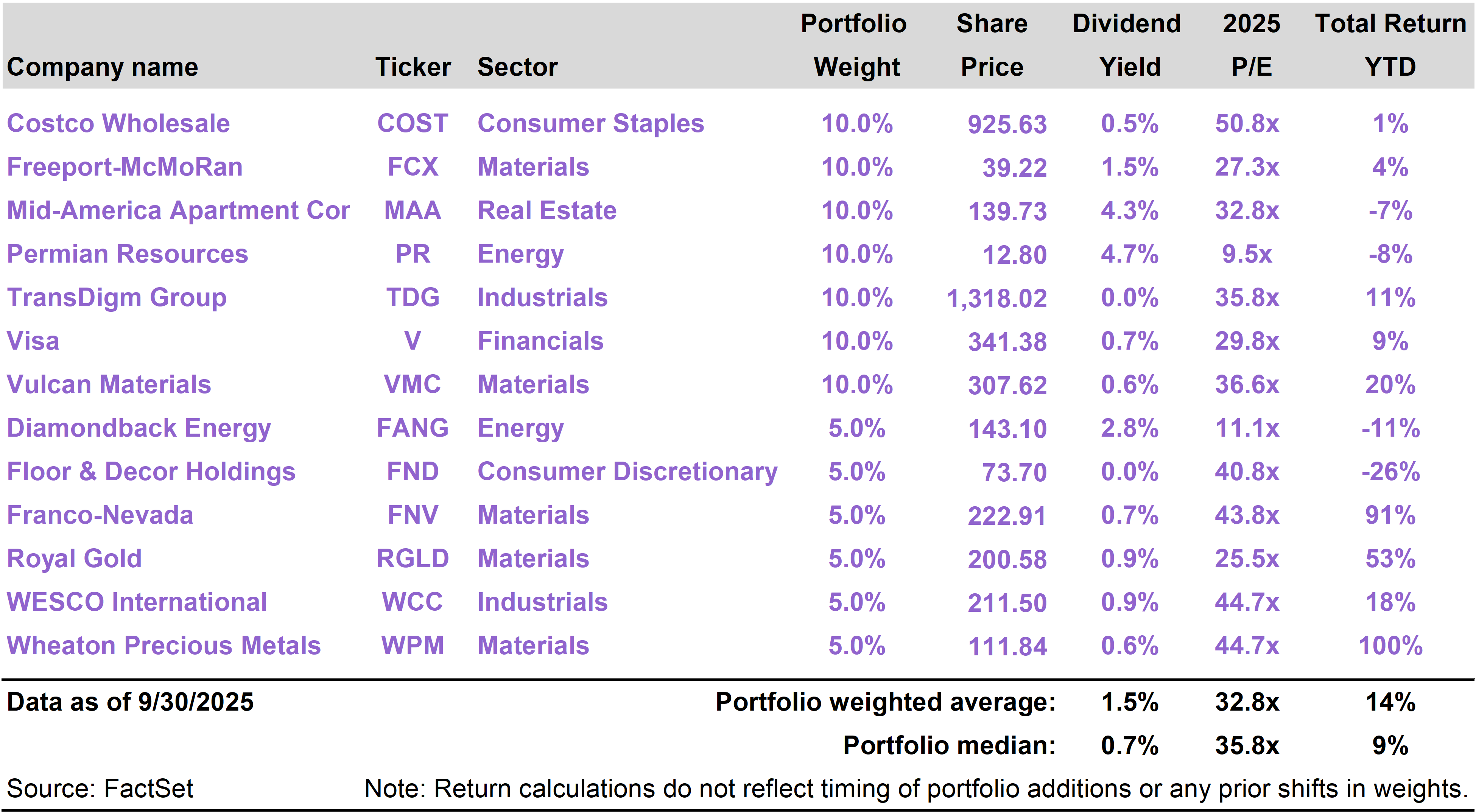

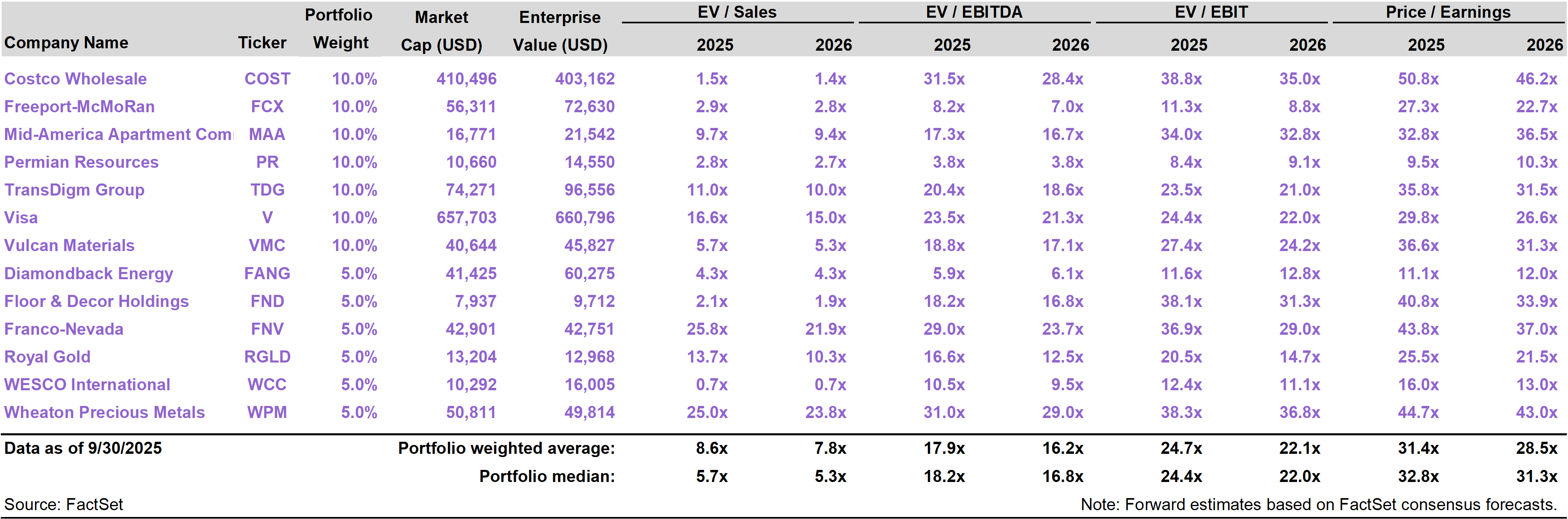

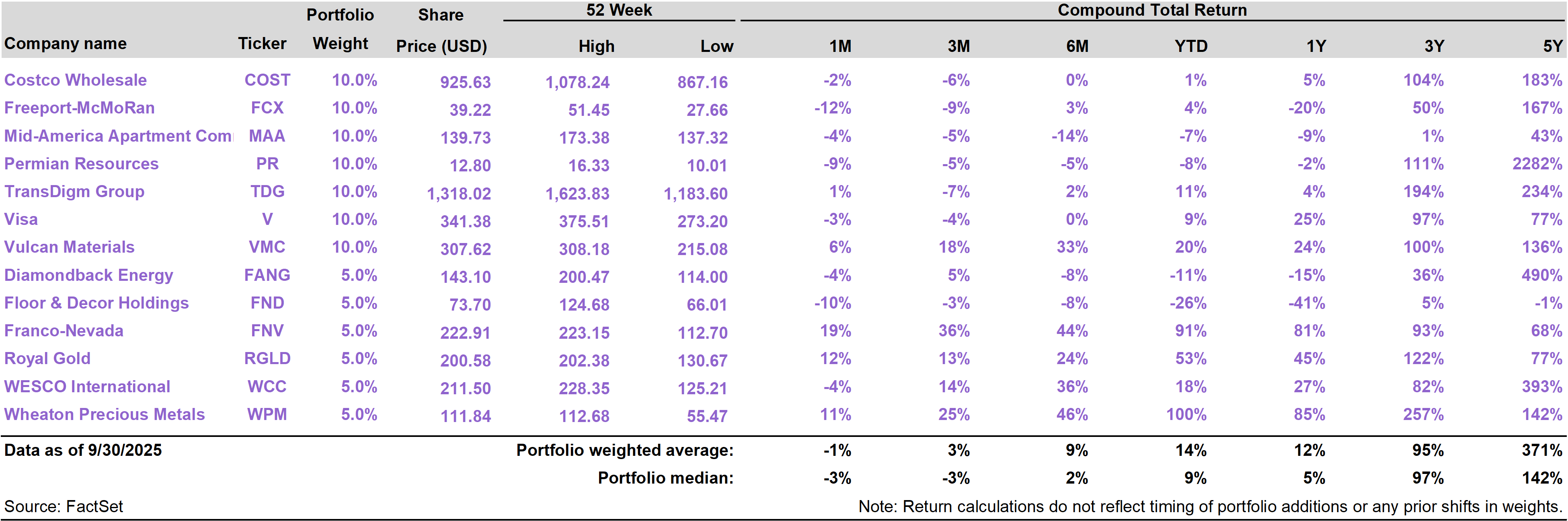

| | | Current portfolio holdings |

|

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

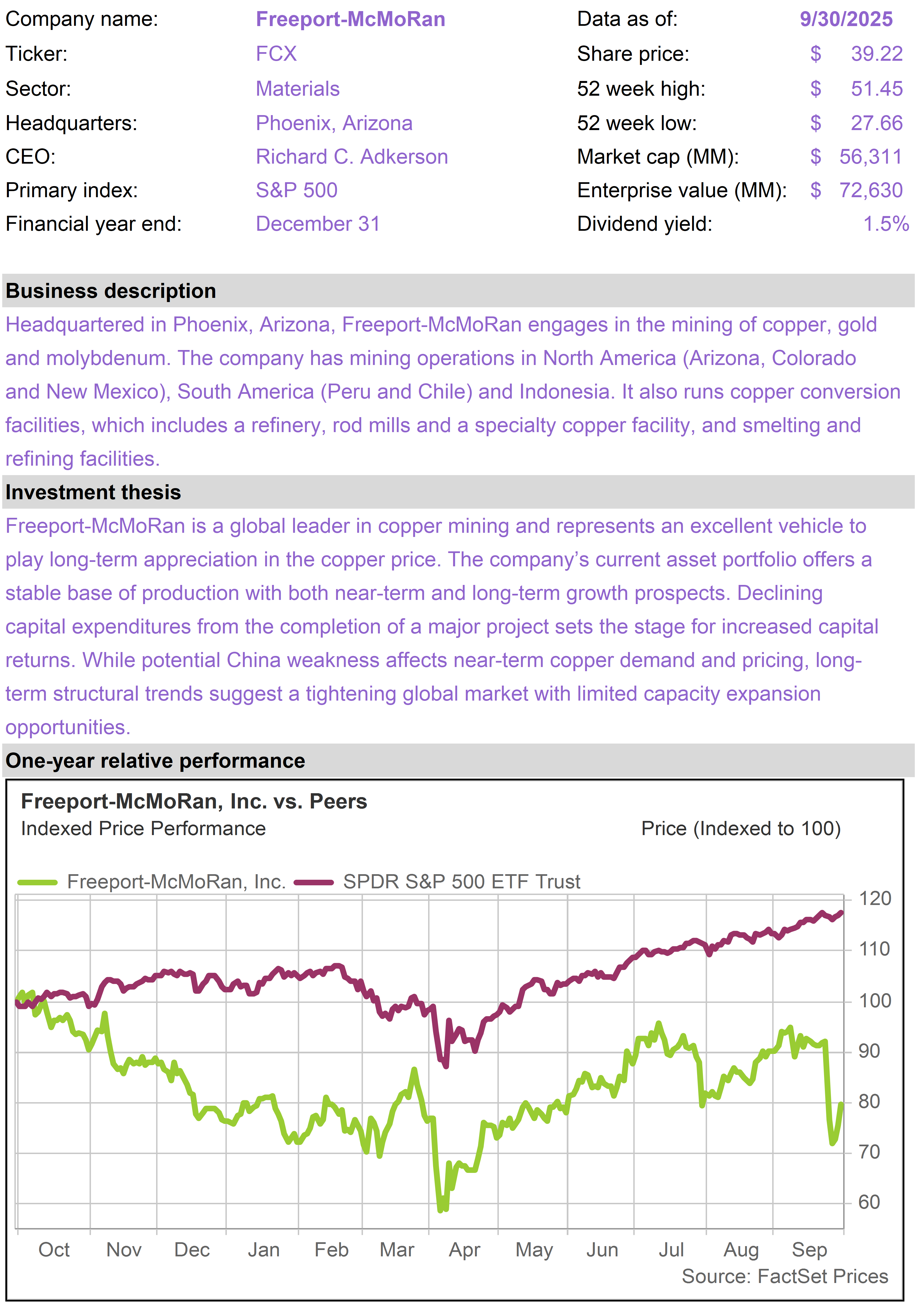

| | | Tech stocks led the market higher in September as investors rediscovered conviction in the AI theme. Anticipated interest rate cuts also helped stocks, although the key variable driving lower rates—labor market weakness—is a concern. Gold has responded quite positively to expected shifts in U.S. monetary policy and advanced 12% in September. The portfolio’s gold streaming stocks outperformed gold this month and on a year to date basis have generated returns from 50% to 100%. We remain positive on these stocks and the portfolio in general, as the debasement trade gains traction. Portfolio returns were impacted this month by a mining accident at Freeport-McMoRan (FCX), which declined 12%. Despite the setback, we continue to like FCX as a long-term copper play.

|

|

| | | The Inflation Protection portfolio returned -1.2% in September, versus a total return of 3.6% for the S&P 500 Index. On a year to date basis through the end of September, the portfolio has generated a total return of 10.4%, versus a 14.8% return for the S&P 500.

The portfolio’s top performing stocks this month were Franco-Nevada (FNV), which returned 19%; Royal Gold (RGLD), which returned 12%; and Wheaton Precious Metals (WPM), which returned 11%.

The portfolio’s worst performers were Freeport-McMoRan (FCX), which returned -12%; Floor & Decor (FND), which returned -10%; and Permian Resource (PR), which returned -9% . |

|

|

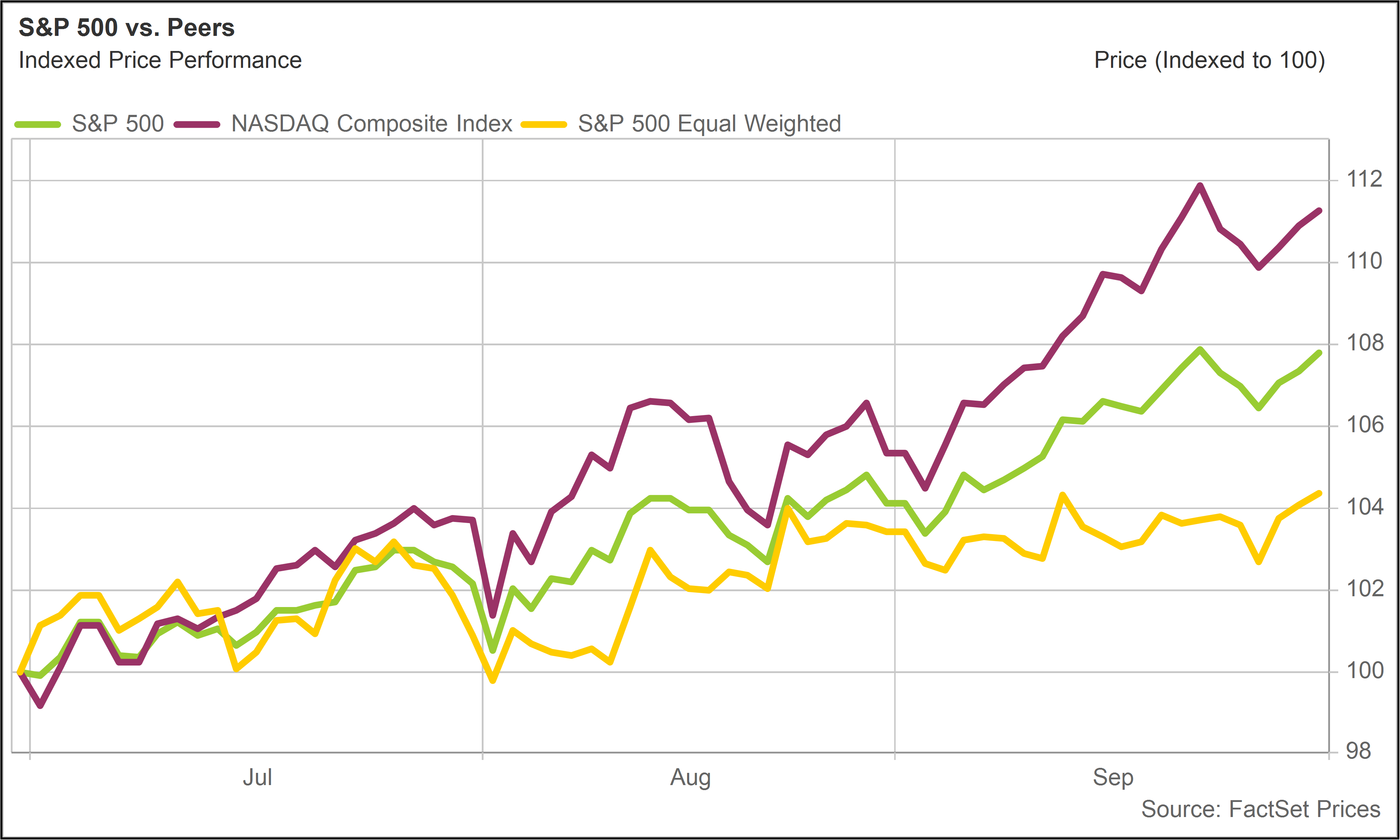

Tech-Led Performance

September was a month in which the market’s high level of tech sector concentration had a significant impact on index performance.

The tech-heavy Nasdaq Composite Index returned 5.7%. This was driven by strong returns from a handful of very large market-cap stocks.

Among the top performers in September were Tesla (TSLA), which gained 33%; Alphabet (GOOGL), which gained 14%; and Broadcom (AVGO), which gained 11%.

By contrast, the S&P 500 Equal Weight Index returned 1.1%. This index is much less affected by the Magnificent Seven and other mega-cap stocks that now dominate the market-cap weighted S&P 500. |

|

|

|

S&P 500, NASDAQ, S&P 500 Equal WeightTotal Return (6/30/25 - 9/30/25) |

|

|

Recovery in AI

We noted last month that stocks linked to the AI theme experienced a bit of a wobble and underperformed the market. Many of these AI-related stocks performed much better this month.

In addition to the mega-cap names mentioned above, American Resilience portfolio holding Oracle (ORCL) was a top performer.

ORCL stunned the market on September 9 after disclosing growth in its Remaining Performance Obligations (a measure of contracted future business) that exceeded 200% in just one quarter.

If you missed our 76report note, please refer to Oracle Flying High on AI Tailwinds.

This revelation sent shares of ORCL immediately soaring—and briefly made founder Larry Ellison the richest man in the world (before TSLA later rallied, putting Elon Musk back on top).

The ORCL news also helped restore broader conviction in the idea that vast sums will continue to get allocated in the years ahead to the global AI data center buildout.

Later in the month, NVIDIA (NVDA), also an American Resilience holding, made an announcement that had implications for ORCL and other AI infrastructure stocks.

The dominant supplier of AI Graphic Processing Units (GPUs) announced a proposed investment in OpenAI, which operates ChatGPT, the leading AI chatbot.

The NVDA deal (see Implications of OpenAI/NVIDIA Mega Deal) is relevant for ORCL in that it provides substantial financial support to OpenAI, which has been identified as the largest customer driving ORCL’s order backlog.

These two events, along with some other favorable developments, helped restore confidence in AI and send share prices higher across the tech landscape.

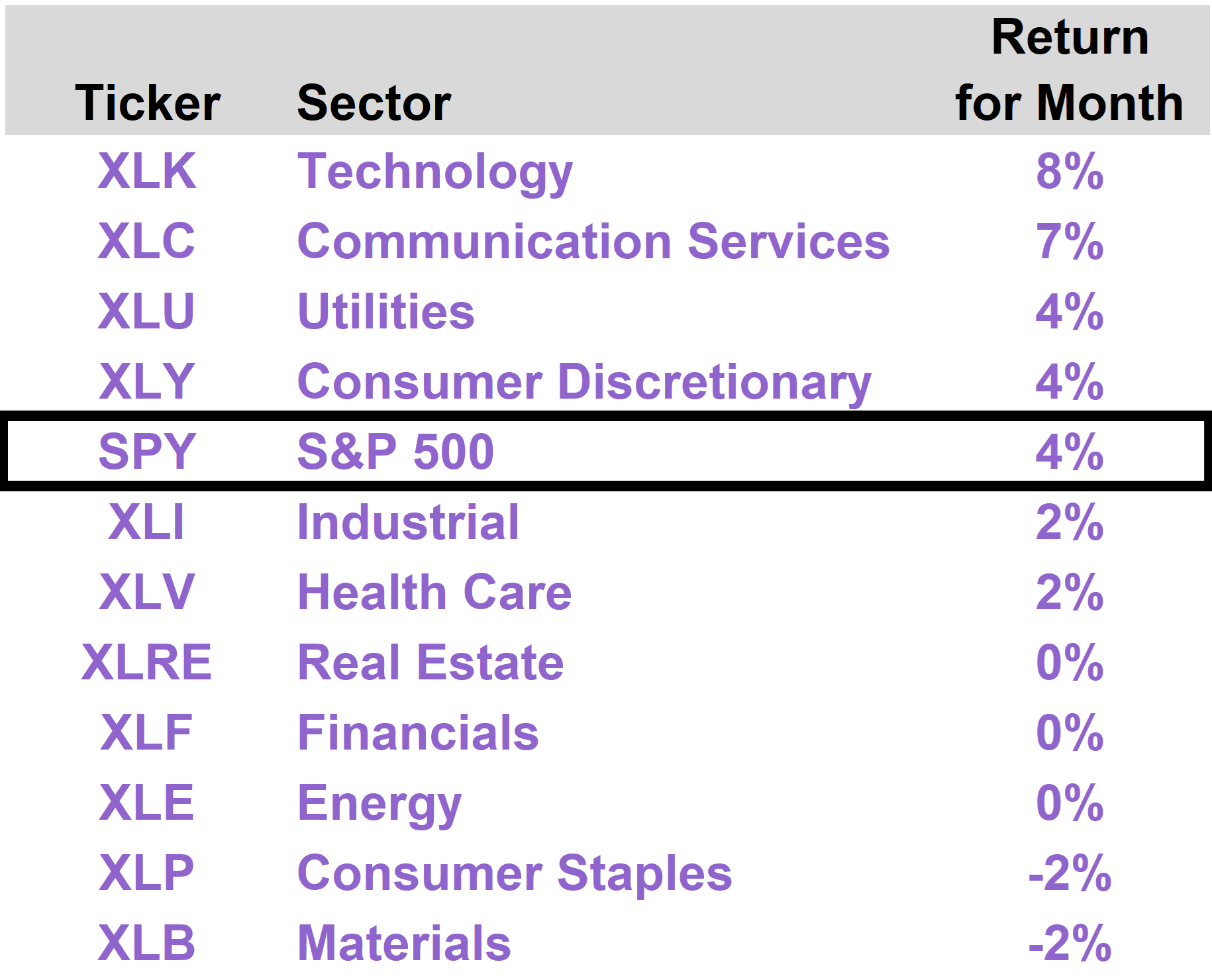

Technology was in fact the best performing sector in September, advancing 8%. It was followed by Communication Services, up 7%, which was led by GOOGL, the stock that has the largest allocation within that sector. |

|

|

| | Interest rate cuts were another narrative helping the market, with particular impact on the rate-sensitive Utilities sector, which advanced 4%. Electric power utilities also benefited from the improved sentiment towards AI, given the immense power demands coming from AI data centers.

Consumer Discretionary stocks benefited from TSLA exposure, which represents more than 20% of the market cap of that sector.

Rate cuts

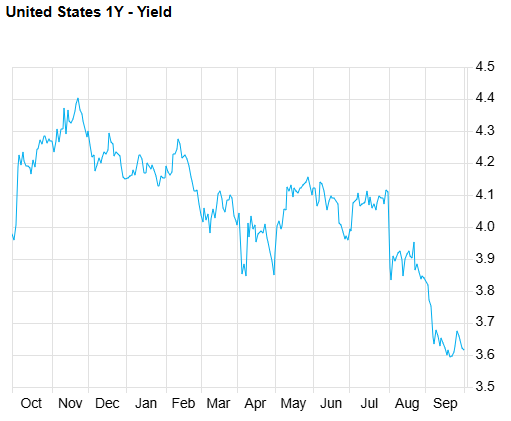

Ever since the Fed’s Jackson Hole meeting in late August, when Jerome Powell communicated his concerns about labor market conditions, market expectations have shifted in the direction of lower rates.

The yield on 1-Year Treasuries now sits around 3.6%, approximately a half-point lower than where it was mid-summer. This reflects the 25 basis point cut in the Fed funds rate that occurred on September 17 (The Fed Gives Trump His First Rate Cut) as well as two incremental 25 basis point cuts that are widely anticipated over the remainder of the year. |

|

|

| 1-Year Treasury Yield(Last 12 Months) |

|

|

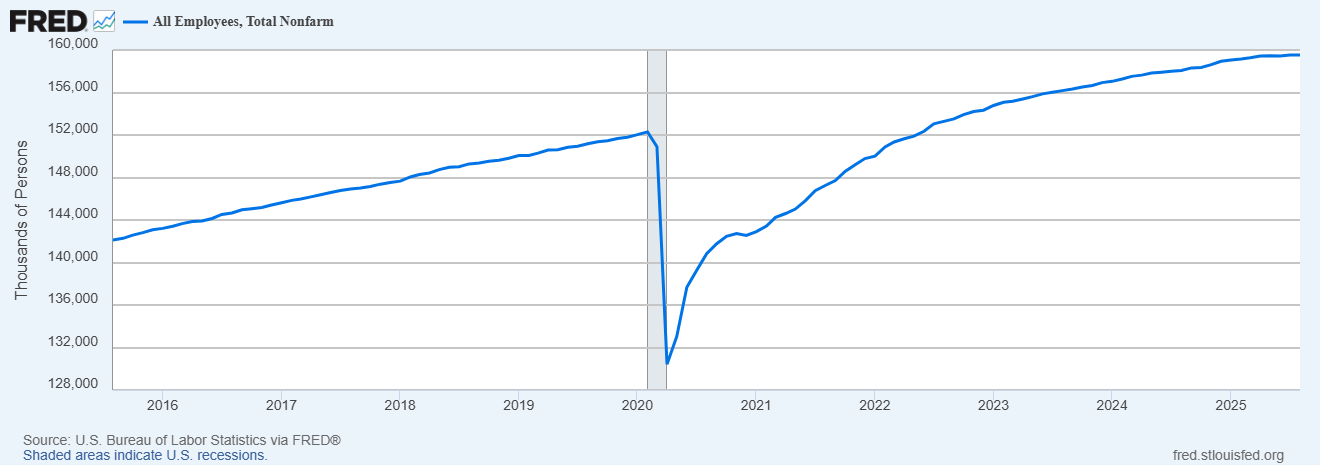

While future rate cuts are a positive for the market, the underlying reasons for rate cuts are not necessarily good.

Unemployment surged with the onset of the pandemic, but overall employment levels have gradually reverted to the long-term trend line, a process that mostly played out between 2020 and 2024. |

|

|

|

Total Employment(Last 10 Years) |

|

|

The economy is now arguably back to full employment levels. With monetary policy still restrictive and ongoing reductions in government headcount (potentially exacerbated by the recent shutdown), hiring has slowed considerably.

The most recent ADP payroll report showed a net decline in private sector jobs of 32,000 last month.

So while stocks are benefiting from anticipated rate cuts and easier monetary policy, there is some concern about the overall health of the economy, with unemployment rates expected to tick up.

From a stock market standpoint, one positive offset to the negative demand impact of rising unemployment and lower consumer confidence is that it puts less upward pressure on wages. Rising unemployment is bad for sales but helpful for operating expenses.

Concerns around the general health of the economy and the consumer likely contributed to the divergence we saw in sector performance.

As AI stocks advanced on reassuring news flow, stocks in sectors that are more cyclical, like Energy, Consumer Staples and Materials, stagnated or retreated.

The “circularity critique”

While AI stocks in general performed well in September, skeptics of the AI boom note that much of the demand for AI has been generated by the AI companies themselves.

For example, NVIDIA’s proposed arrangement to invest in OpenAI—which involves commitments by OpenAI to purchase NVIDIA equipment—has been described by some as a prime example of “circular” funding of the AI buildout.

Parallels have also been made to “vendor financing,” with the suggestion being that there is not authentic customer demand. Other examples include NVDA funding AI startups.

While we acknowledge the criticism, we interpret NVDA’s recycling of its vast profits into downstream AI business models as a rational and strategic use of its resources, especially given how it reinforces its own technological grip on the industry.

By making minority investments in these companies, NVIDIA is able to avoid antitrust scrutiny, while still creating favorable conditions for itself as the dominant supplier.

Lower rates either way?

We are optimistic that we are still in the early stages of spending on AI infrastructure, but it is true that AI-related capital spending has become a key pillar of the economy, as other parts of the economy (such as the public sector and housing) have weakened.

To the extent the AI spending boom decelerates, this should only intensify the need for easier monetary policy to offset lower investment demand.

On the other hand, all of this AI spending—should it be sustained or even accelerate—has the potential to drive a disinflationary productivity boom. Knowledge workers will effectively be replaced by much cheaper AI agents.

So even in the context of sustained heavy investment in AI, which would only be justified by real productivity gains, the conditions are created for easier monetary policy.

These are longer term considerations. Meanwhile, in the here and now, unemployment rates are ticking up and Trump is preparing to install a new Fed Chair by next May who will undoubtedly be inclined to cut interest rates.

With long-term and short-term indicators pointing in the direct of easier monetary policy, we are not surprised to see gold and Bitcoin attracting capital.

Both of these hard money alternatives—one ancient, one still a teenager—performed well in September.

Gold crossed $3,900 per ounce and is up more than 45% year to date through the end of September. After some recent weakness, Bitcoin is reapproaching all-time highs and has crossed $120,000 as October begins, up nearly 30% year to date. |

|

|

|

S&P 500, Gold, Bitcoin - Total Return(Year to Date through 9/30/25) |

|

|

We remain enthusiastic about the AI opportunity set and have been increasingly viewing all investments through the lens of long-term AI-driven changes to the economy.

We want all of our investments to benefit one way or another from AI-related change, but it is important at the same time to have investments that are not totally reliant on the AI buildout.

If the biggest risk to the AI story is that capital spending expectations are excessive, stocks with secure cash flows across different sectors look attractive in that scenario, especially as monetary policy gets easier.

Investors should stay positioned in core AI plays but also stay diversified, which includes, in our view, allocations to gold and Bitcoin. |

|

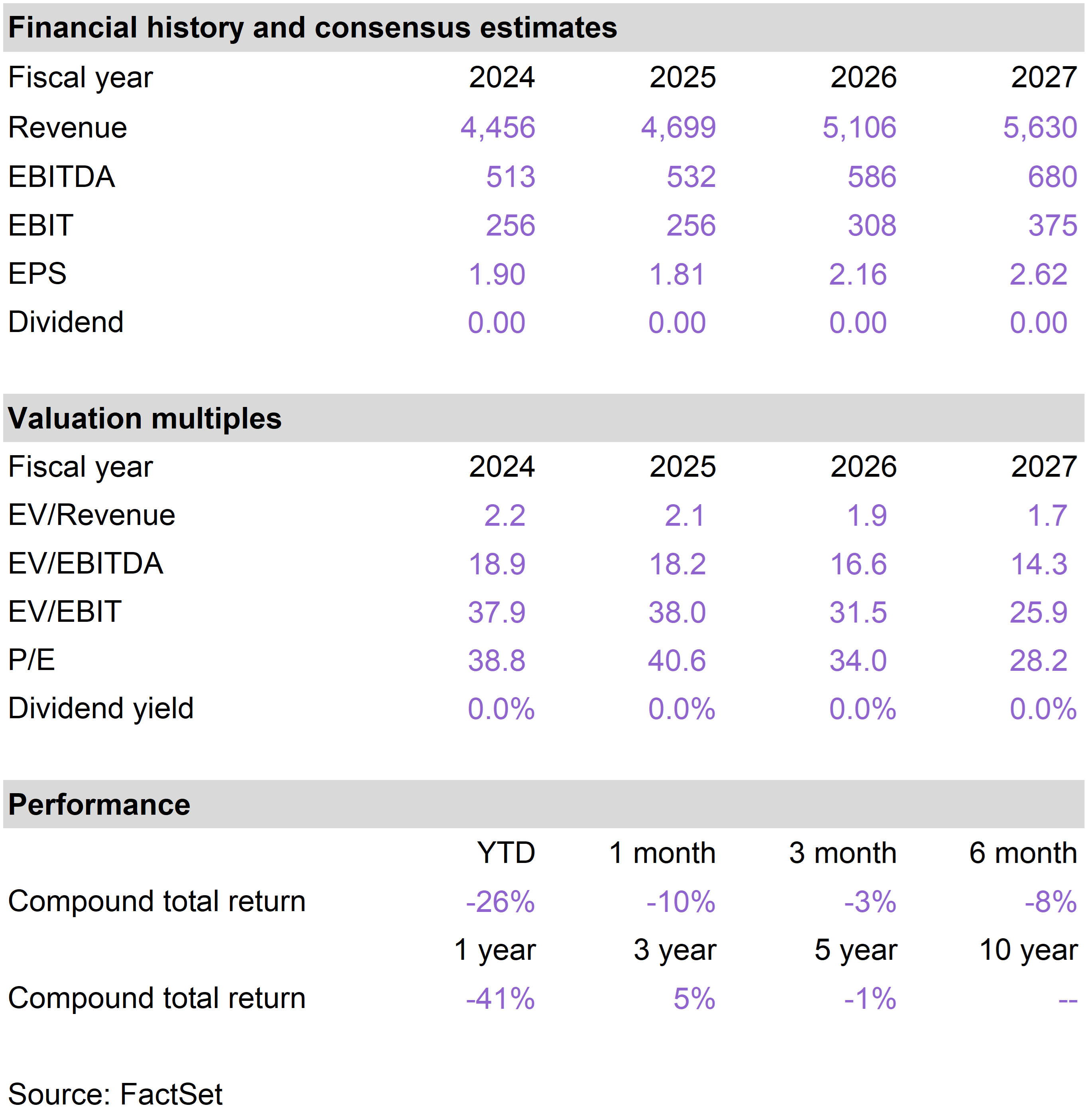

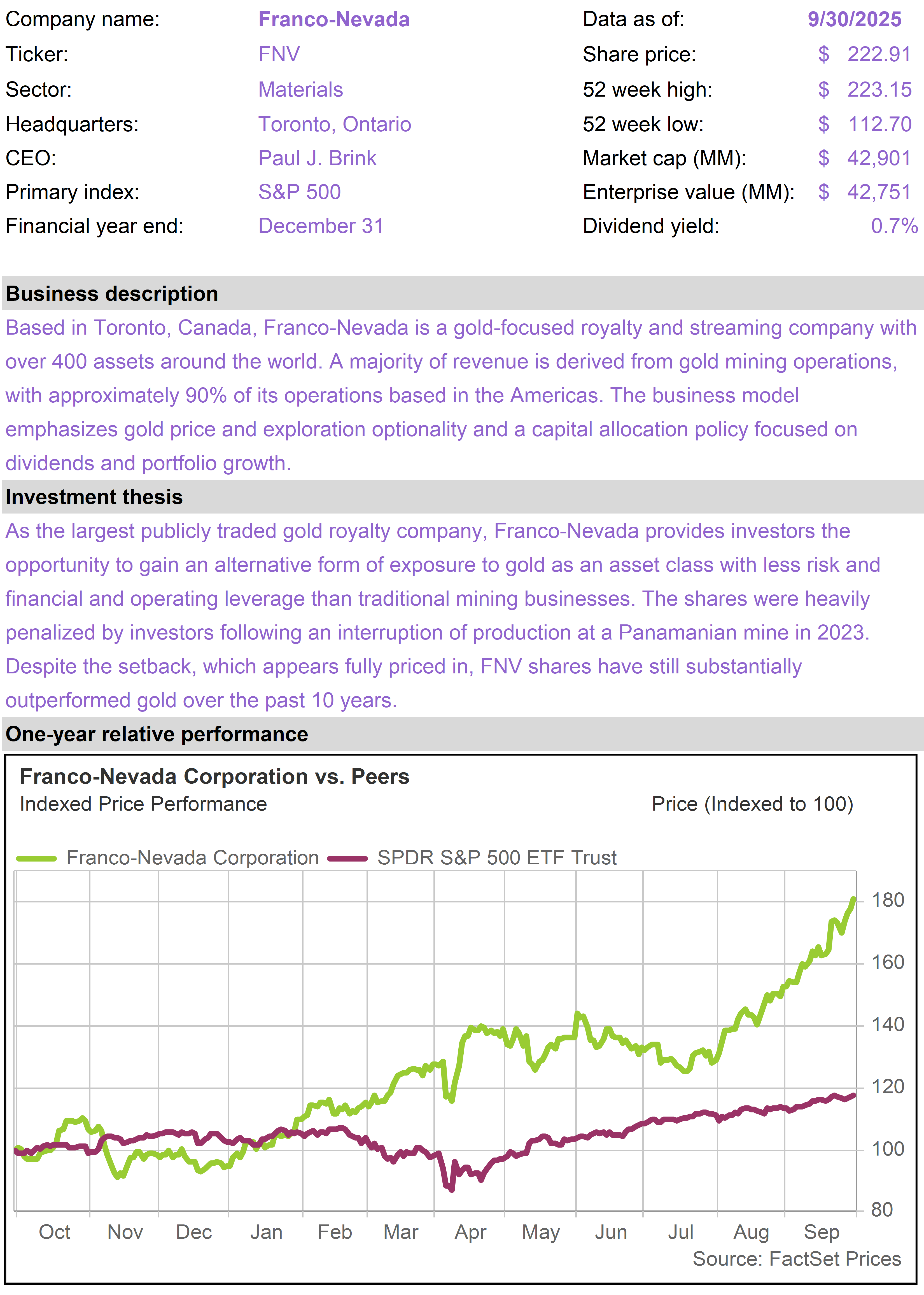

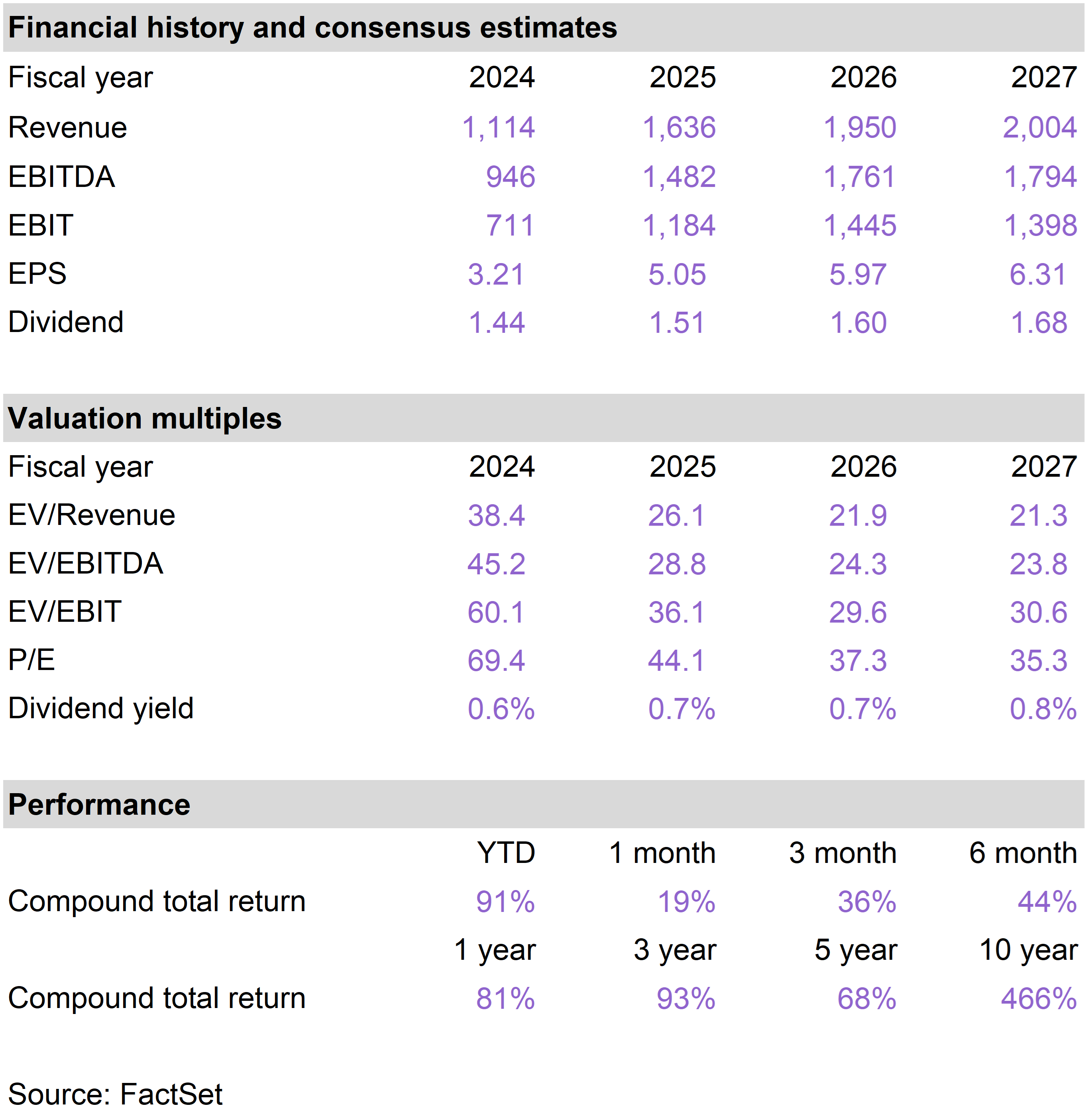

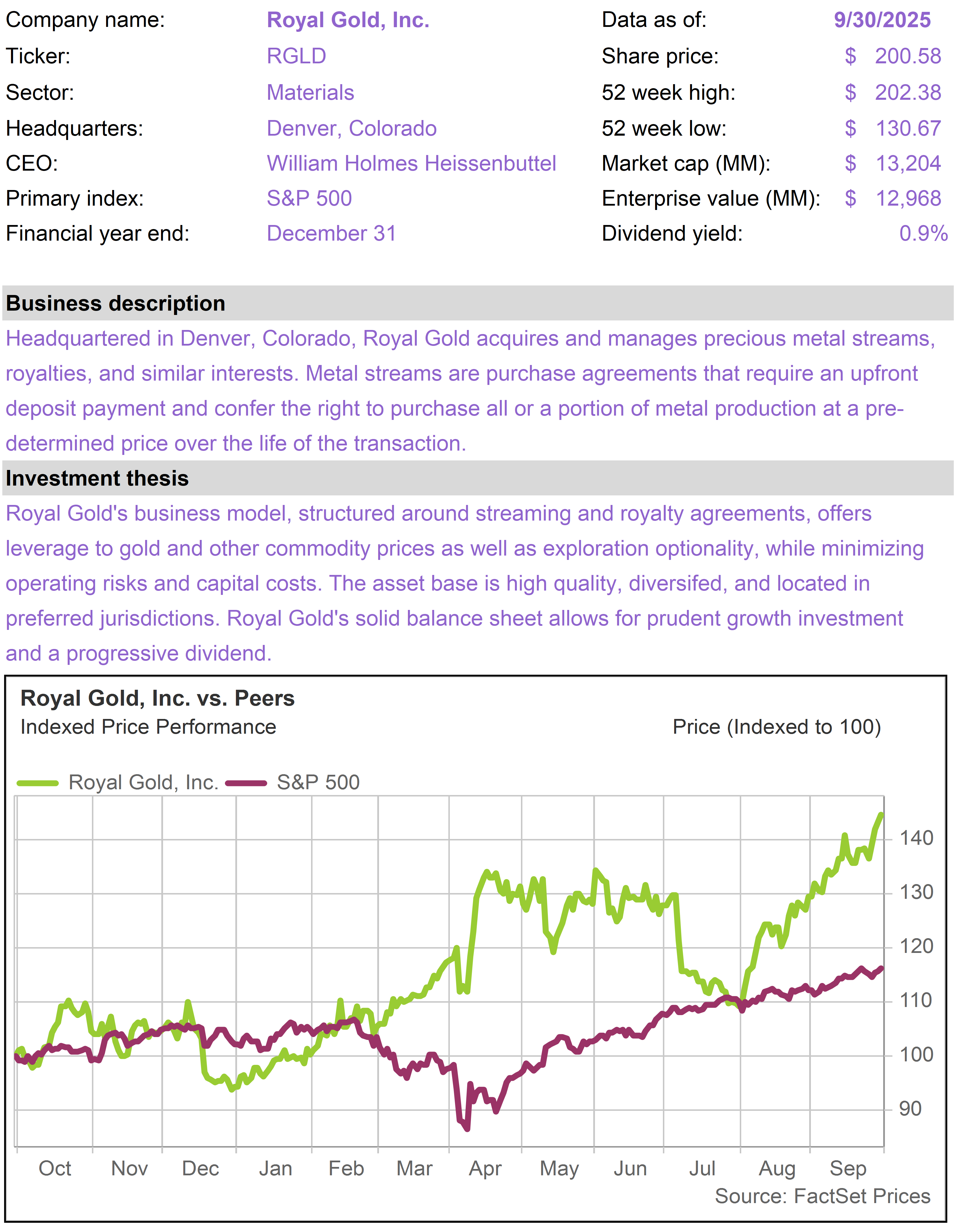

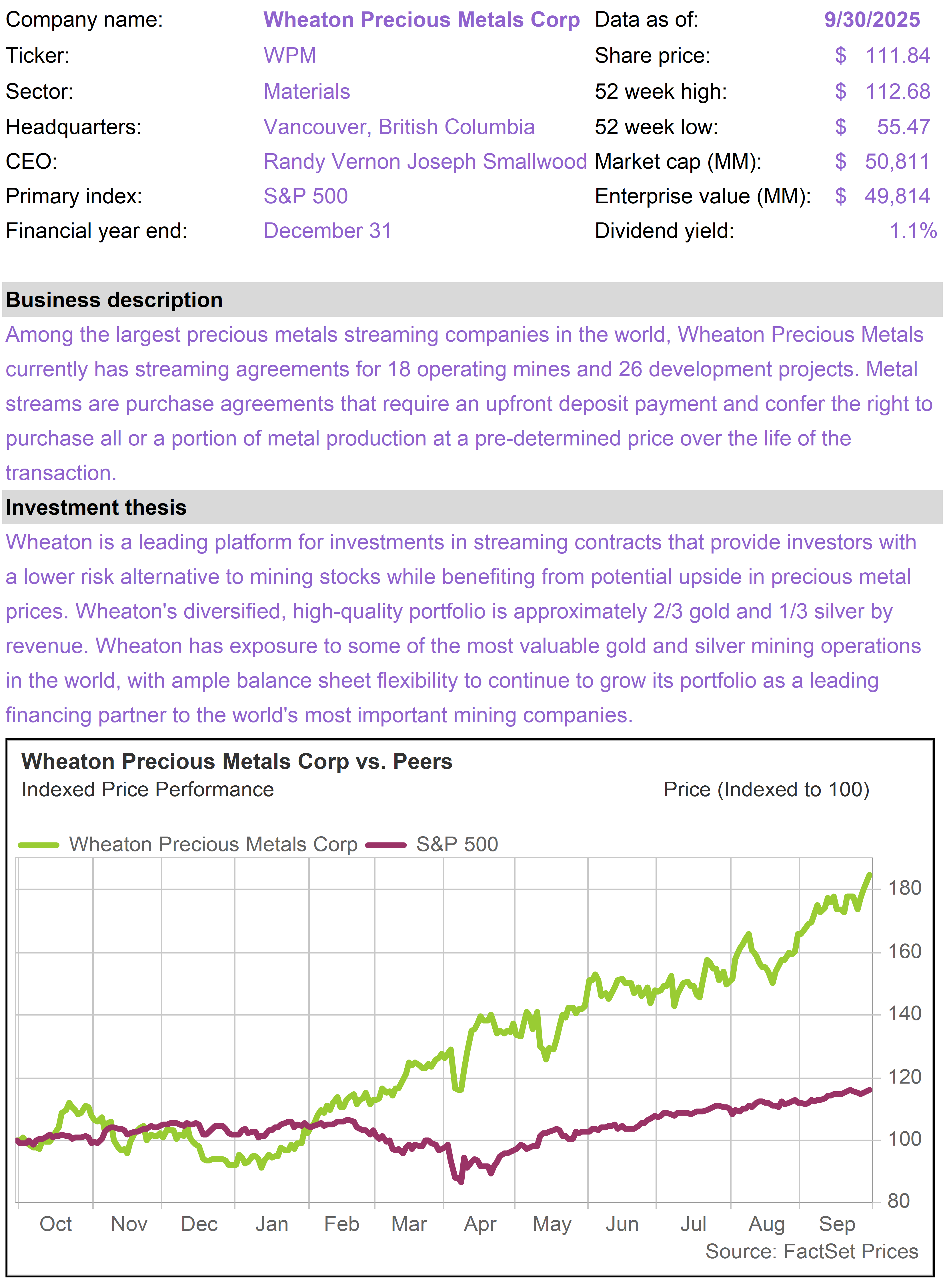

| | | The top performing stocks in the Inflation Protection portfolio this month were Franco-Nevada (FNV), which returned 19%; Royal Gold (RGLD), which returned 12%; and Wheaton Precious Metals (WPM), which returned 11%.

The worst performing stocks in the portfolio were Freeport-McMoRan (FCX), which returned -12%; Floor & Decor (FND), which returned -10%; and Permian Resources (PR), which returned -9%. |

|

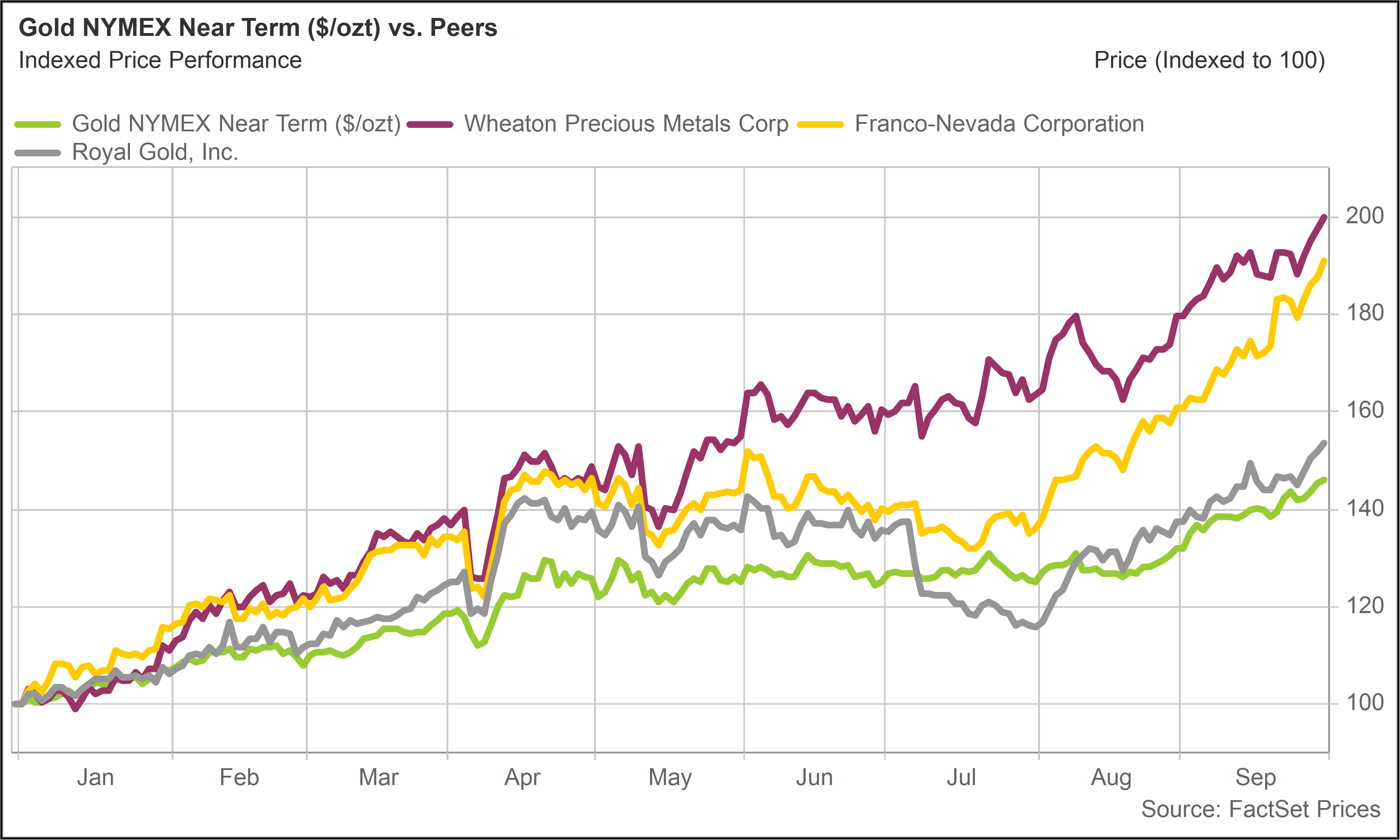

| As gold closes in on $4,000 per ounce, the portfolio’s gold streaming plays—FNV, RGLD, and WPM—remain the top performers this year.

The gold price advanced approximately 12% in September, closing the month just shy of $3,900. On average, the portfolio’s gold streaming stocks delivered somewhat higher performance, consistent with our expectation that they should deliver amplified returns to the gold price.

On a year to date basis, these stocks have been exceptional performers. Since the start of the year through September 30, gold has returned 46%. WPM, FNV and RGLD have respectively delivered total returns of 100%, 91%, and 53%. |

|

|

| Gold vs. WPM, FNV, RGLD(Total Return - Year to Date) |

|

| Gold and gold-related assets are among the leading investments in what the investment community is increasingly referring to as the “debasement trade.”

The debasement trade is the investment thesis that governments, especially the U.S., are eroding (or “debasing”) the real value of their currencies through persistent deficits, rising debt, money supply growth, and inflationary policies.

Investors who believe in this thesis position their portfolios to benefit from the gradual loss of purchasing power of fiat currencies.

The Inflation Protection portfolio strategy was created to present investors with opportunities in the stock market that align with this thesis. These may supplement investments outside of the stock market, such as direct investments in commodities like gold and Bitcoin.

As the Fed shifts gears towards less restrictive monetary policy, we expect the debasement trade to continue to gain traction among investors.

While the gold price ebbs and flows, we view the long-term trajectory as up and continue to favor our gold streaming stocks, which inherently become more valuable as gold appreciates.

The portfolio was adversely affected this month by a serious incident at one of the key mining operations of FCX. There was a “mud rush” accident at the Grasberg mine in Indonesia which forced a halt in underground operations, damaged infrastructure, and cut off access routes.

FCX shares fell sharply after it reduced its copper and gold sales guidance, warning that fourth-quarter output from the affected areas could be “insignificant.”

The temporary closure of the mine will have a financial impact on FCX, but we believe it is more than accounted for by the decline in the share price, which has been recovering.

A silver lining is that the problem at the mine has caused tightness in global copper supplies, which contributed to a 6% gain in the copper price in September.

The incident is a reminder of the importance of diversification with stocks. Company-specific mishaps, like an accident at a facility, are unpredictable but do occur.

We continue to view FCX as an excellent long-term play on copper price appreciation.

On the supply side, our constructive view on copper is underpinned by the difficulty associated with copper mining and the extremely long lead times (10 years +) associated with launching new mines. Meanwhile, naturally occurring copper reserves have a tendency to be located in politically and technically challenging jurisdictions, like Indonesia.

On the demand side, copper, because of its conductive properties, is arguably the key metal associated with the electrification theme. This investment theme pre-dates AI, but AI has now become a major component of it.

Put simply, the world needs more and more electrical wiring, and there is no plausible substitute to copper. And, like all commodities, copper prices also benefit from the debasement trade.

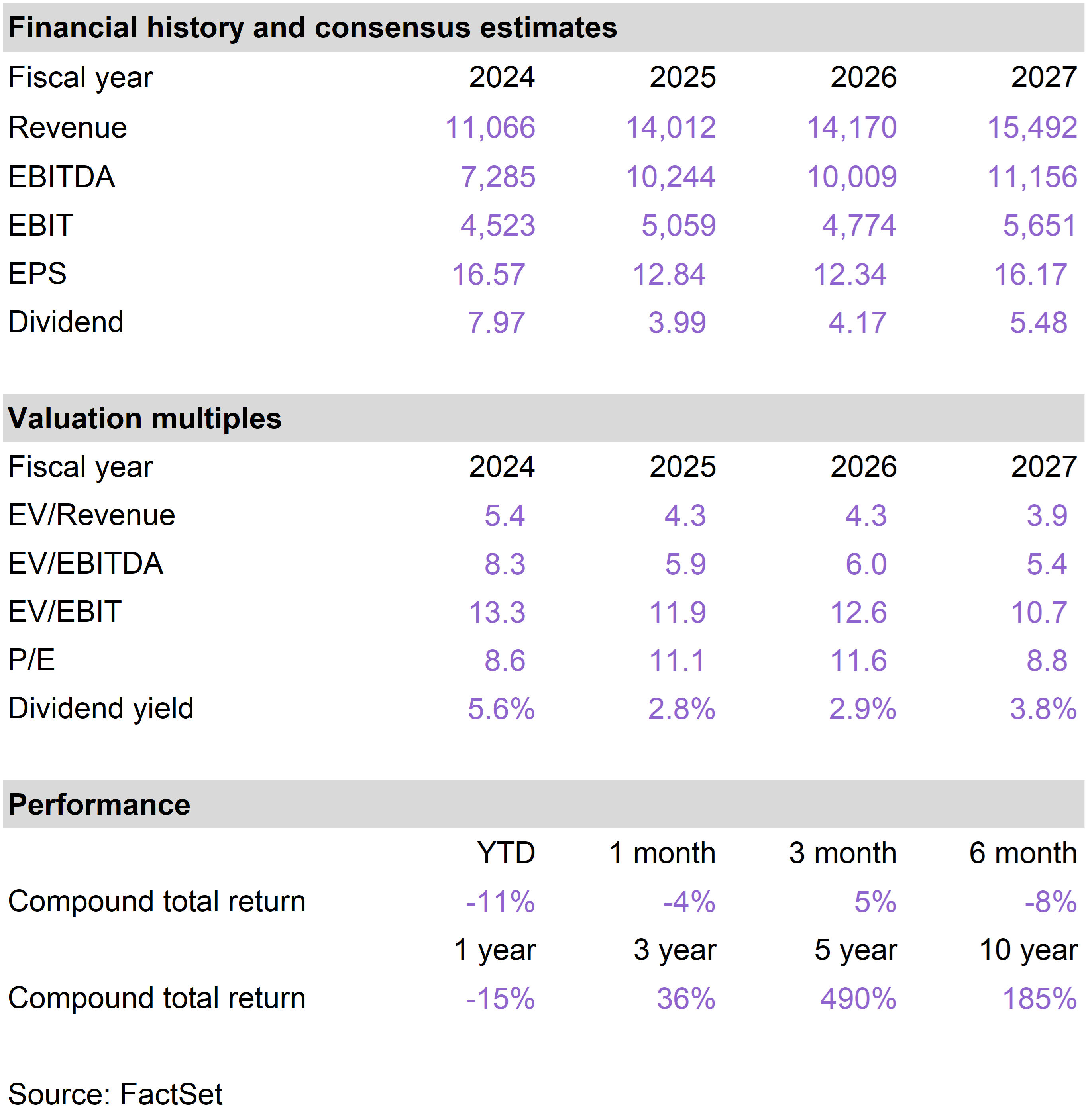

FND, which is closely linked to the housing sector, underperformed in September with weak housing market data, although falling interest rates should be a long-term catalyst.

We continue to like FND as a structural growth opportunity in the context of a meaningful housing shortage in the U.S.

Shares of PR slid in September with oil price weakness. In early September, the company announced solid second quarter earnings results. Management continues to execute well but cannot control the oil price.

The shares are likely to remain out of favor so long as oil prices are soft, but they appear quite undervalued, even if one assumes a continuation of low oil prices.

By conventional valuation approaches, PR could fundamentally be worth as much as double its current share price. The company, which is relatively small, with very attractive oil and gas reserves, is also a long-term buy-out candidate. |

|

| | |

| | |

| | |

| | | |

|

| | |

|

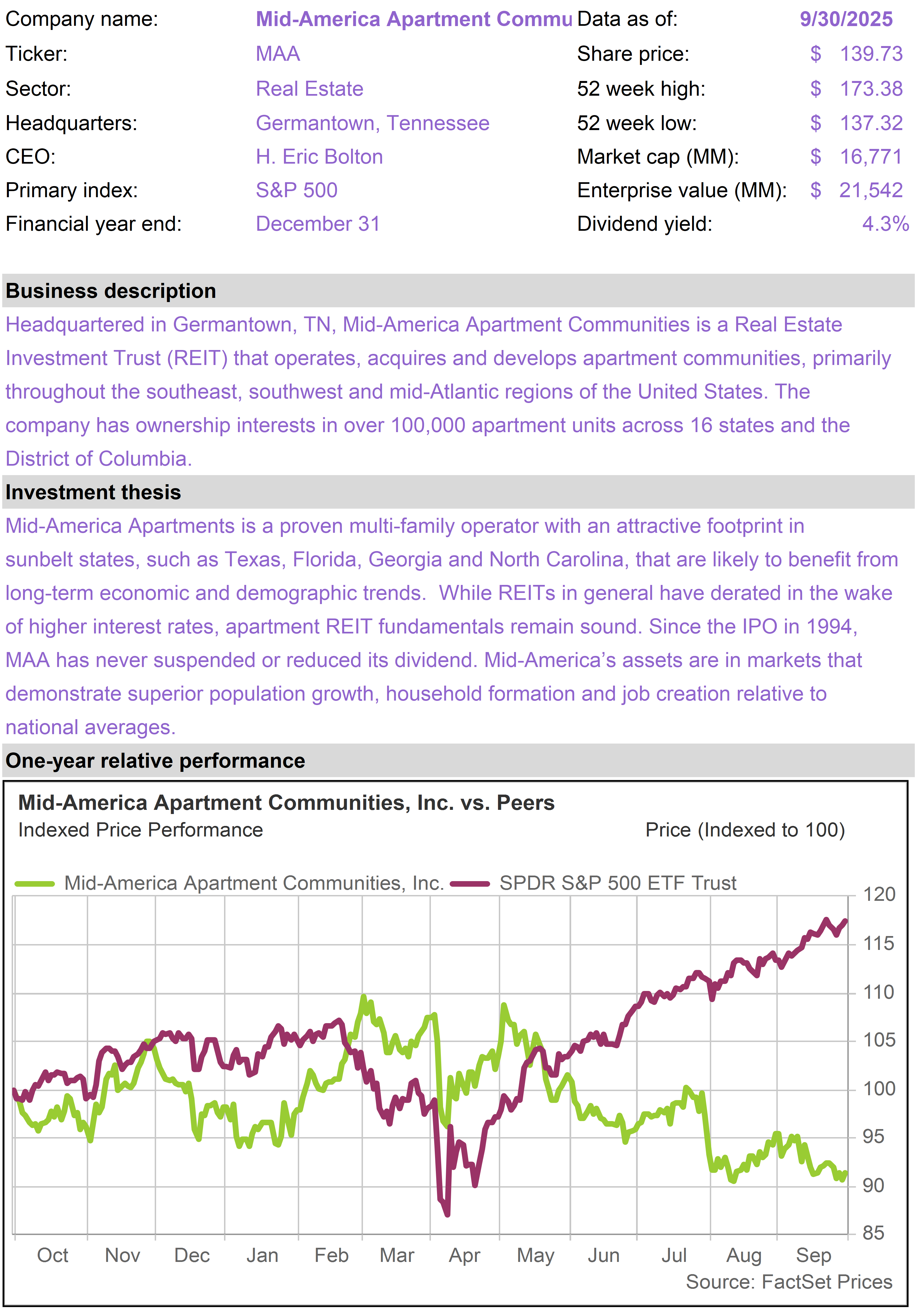

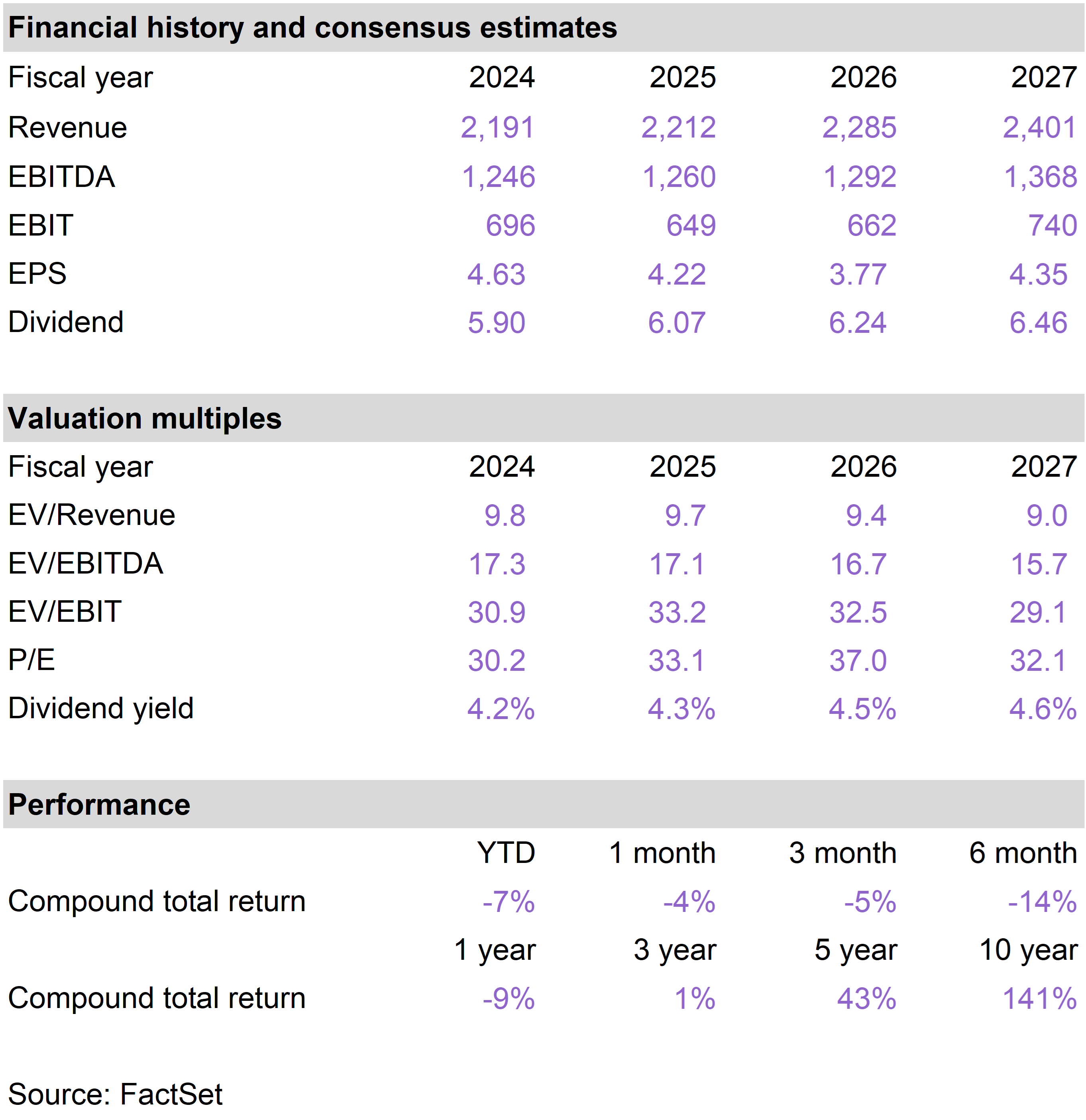

| | Mid-America Apartment (MAA) |

|

|

|

| |

|

| | |

|

| | |

|

| | |

|

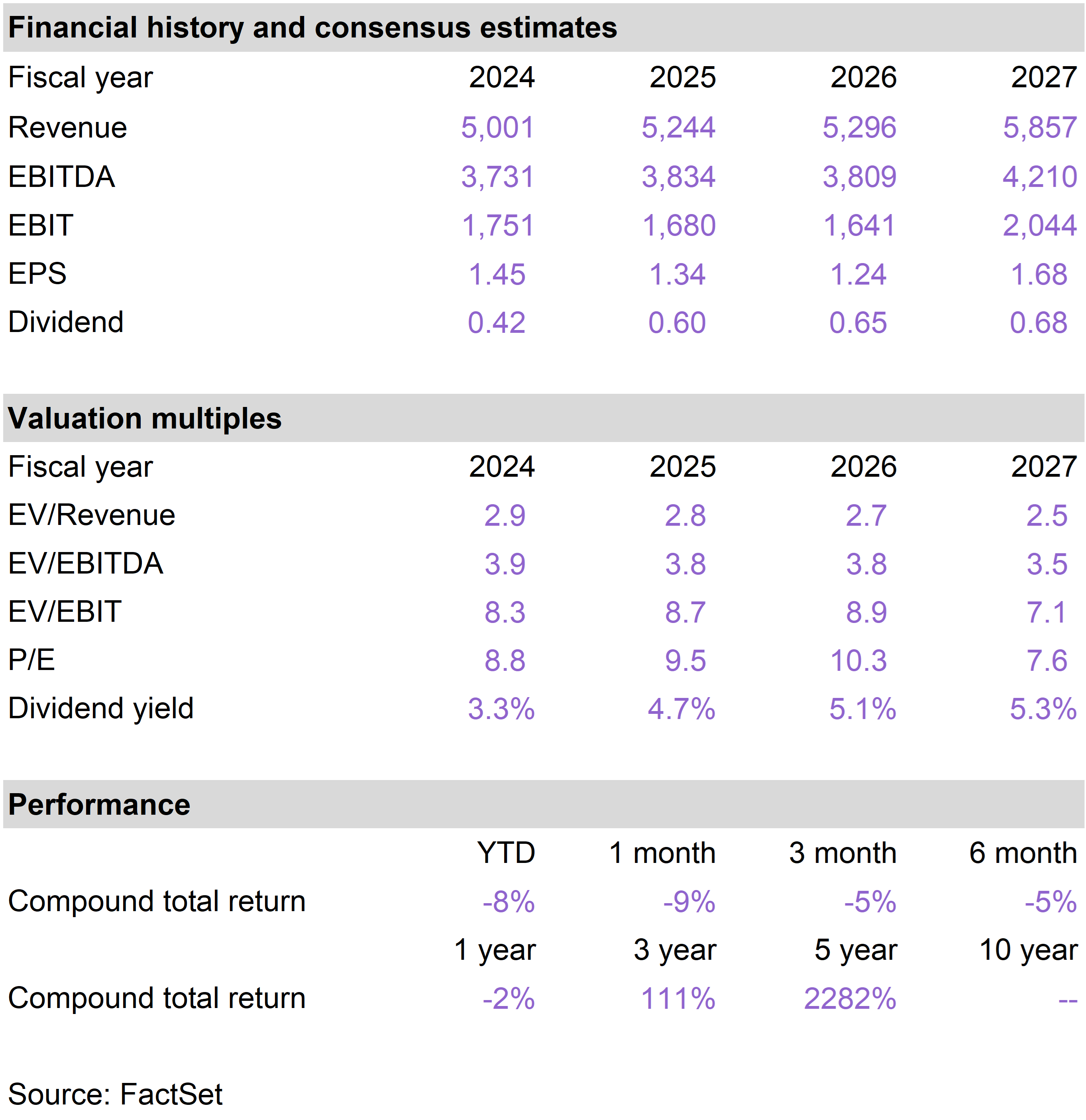

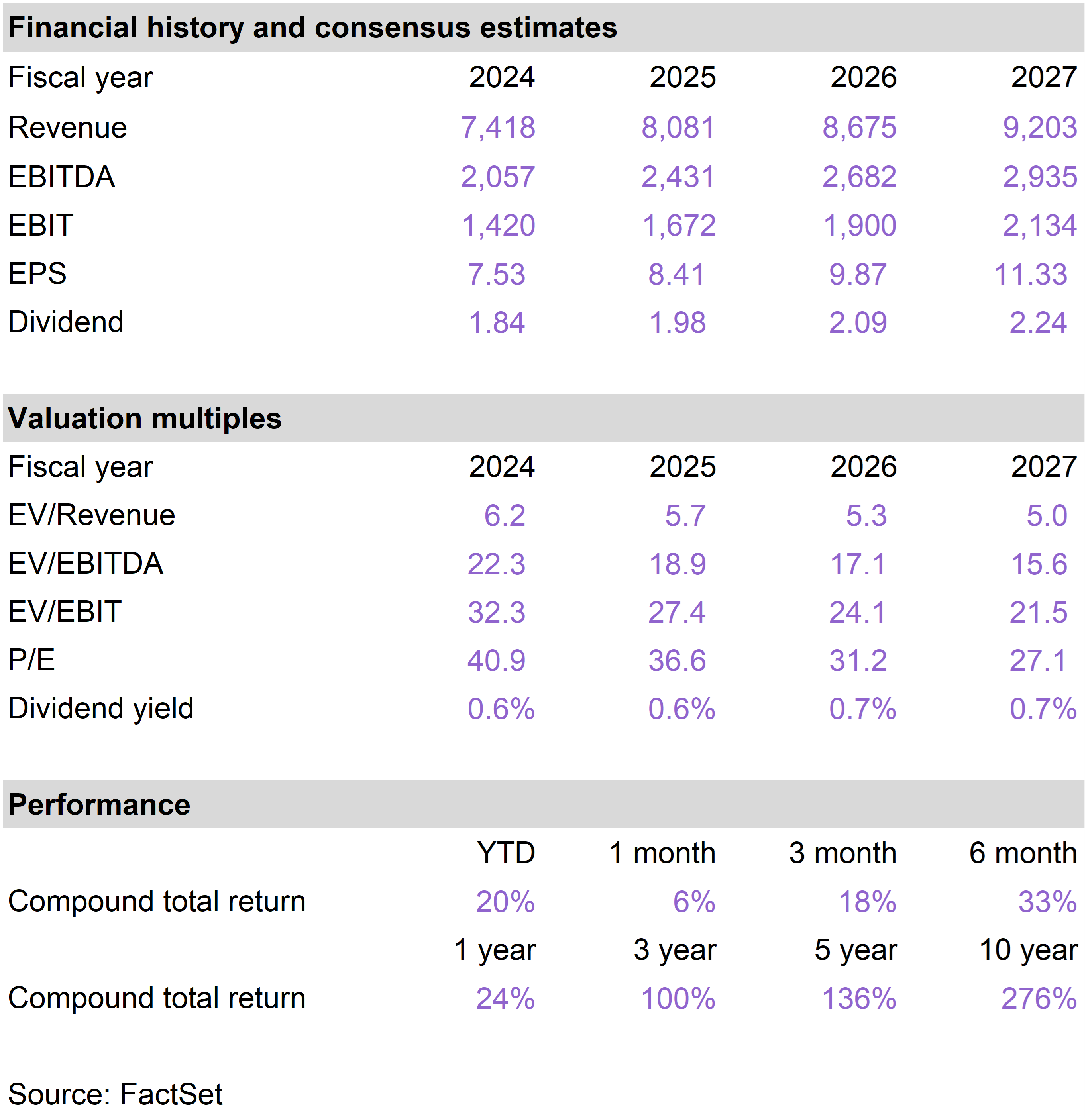

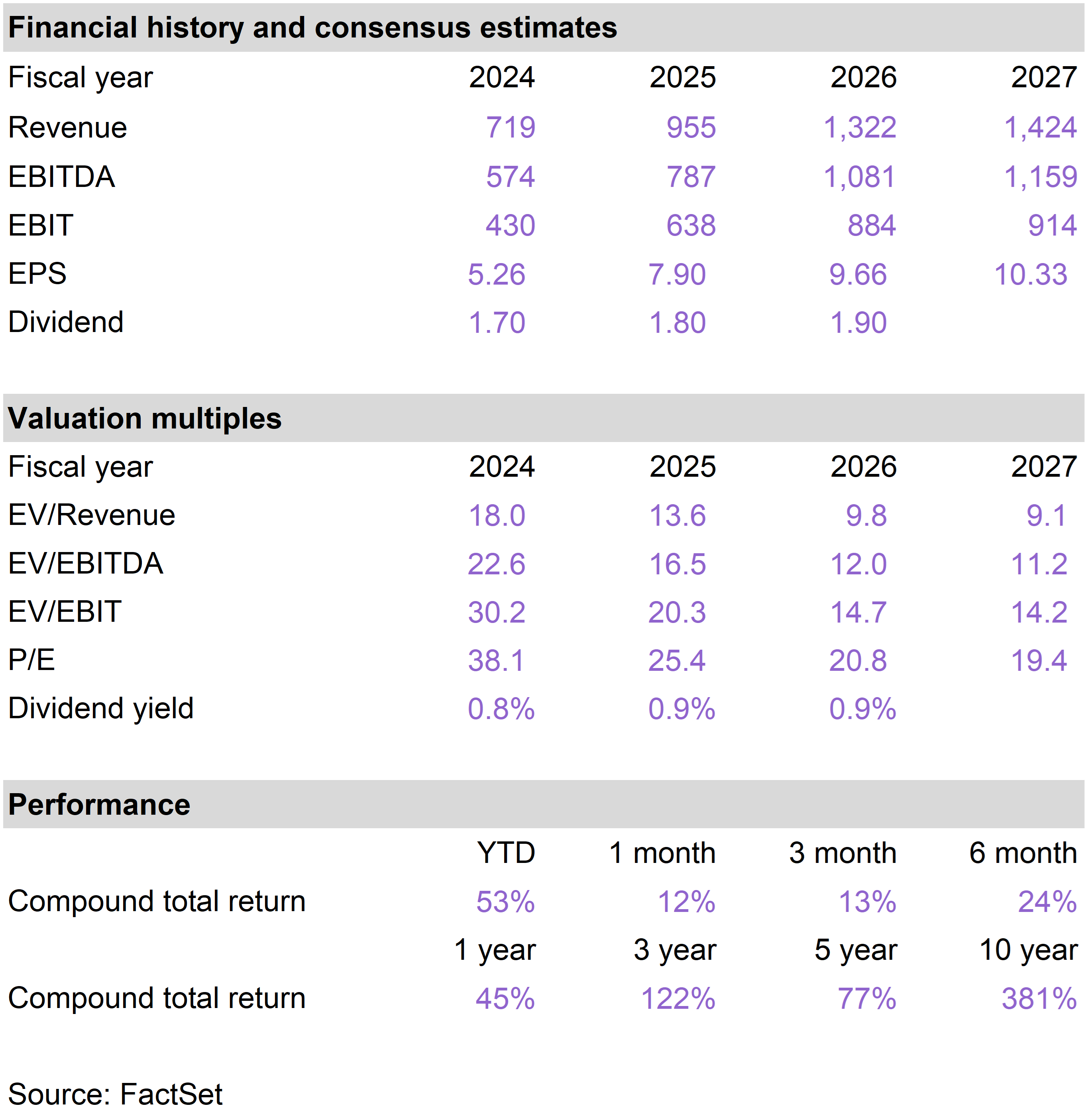

| | Diamondback Energy (FANG) |

|

|

|

| | Floor & Decor Holdings (FND) |

|

|

|

| | |

|

| | |

|

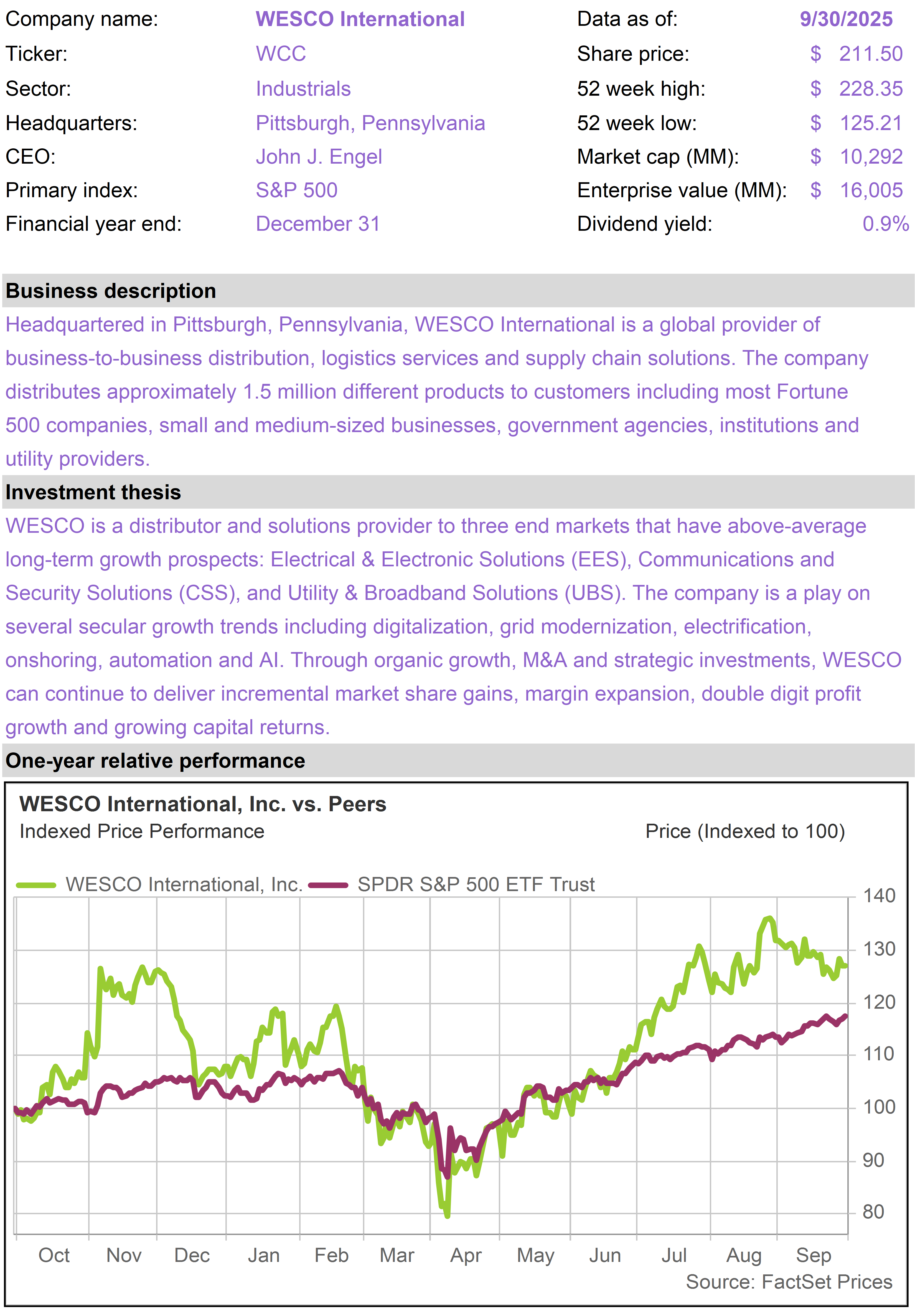

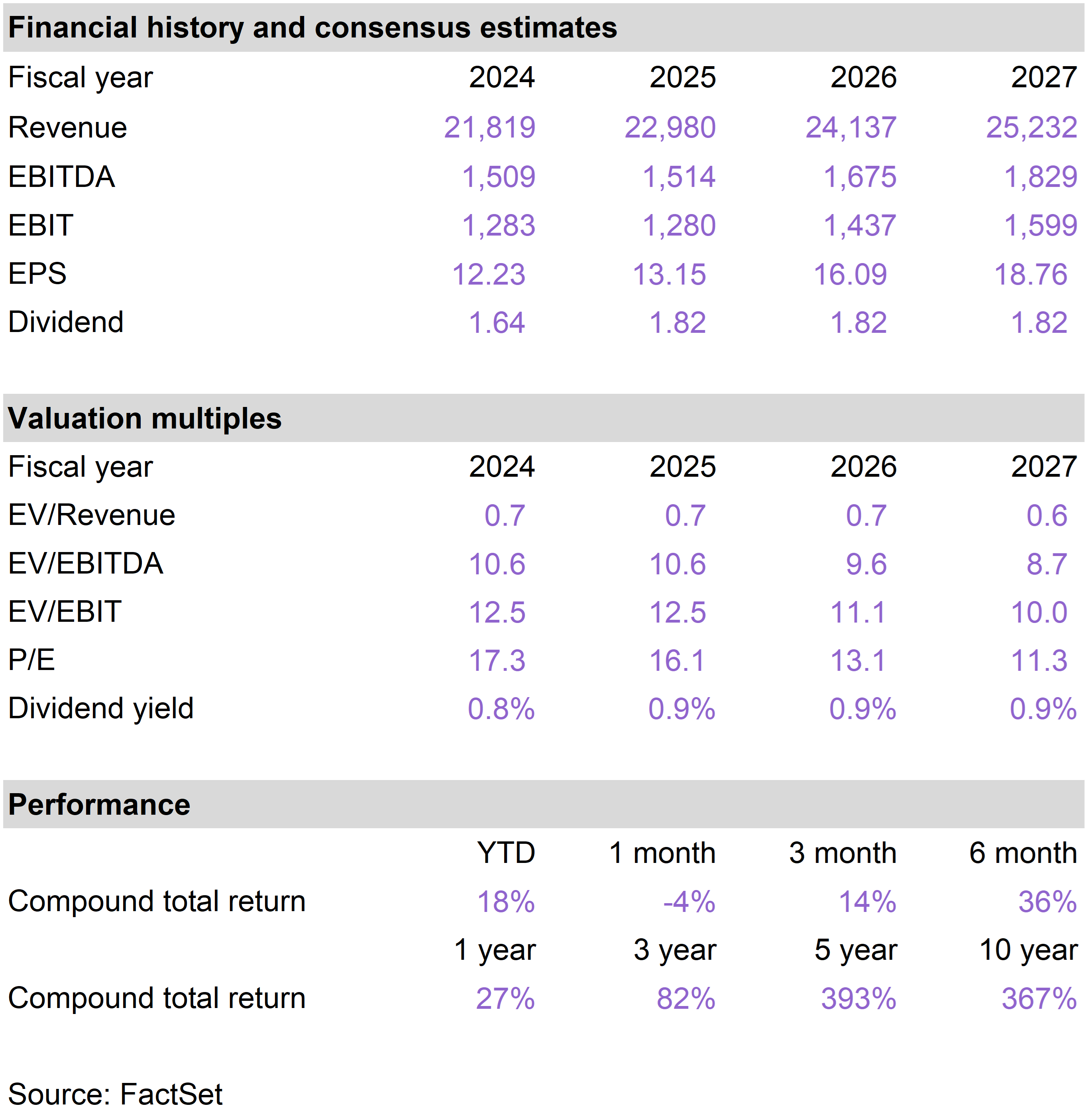

| | WESCO International (WCC) |

|

|

|

| | Wheaton Precious Metals (WPM) |

|

|

|

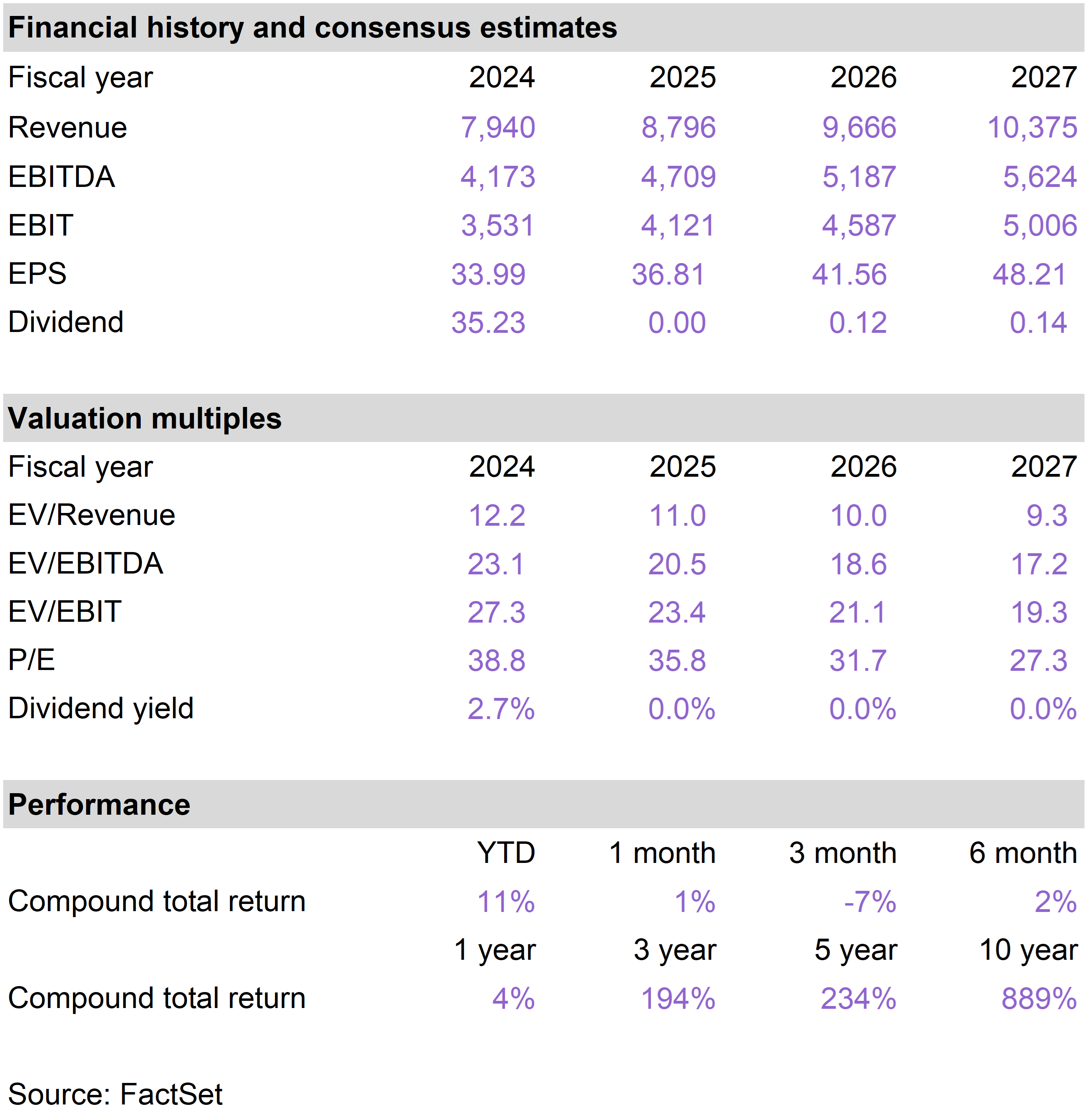

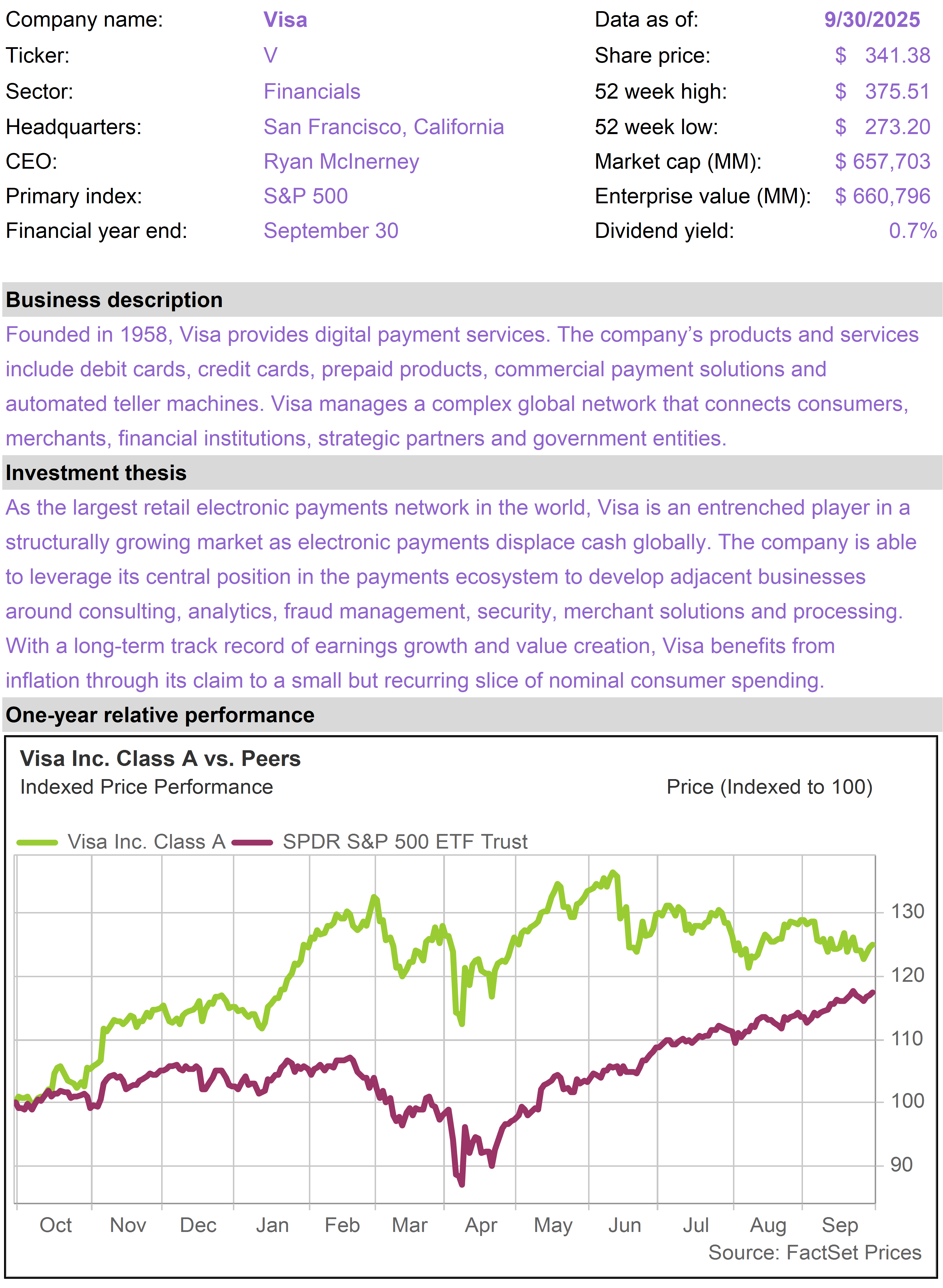

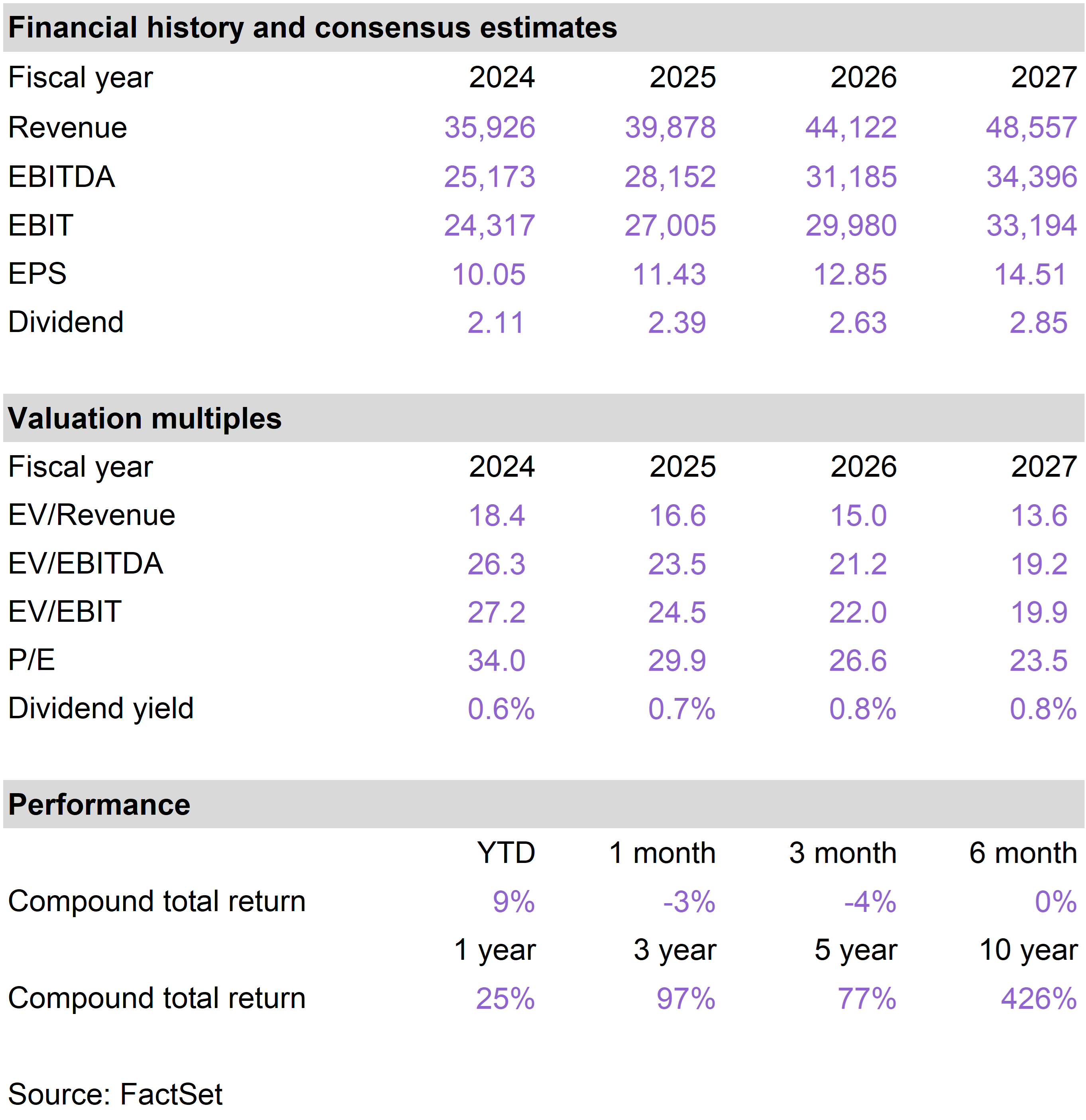

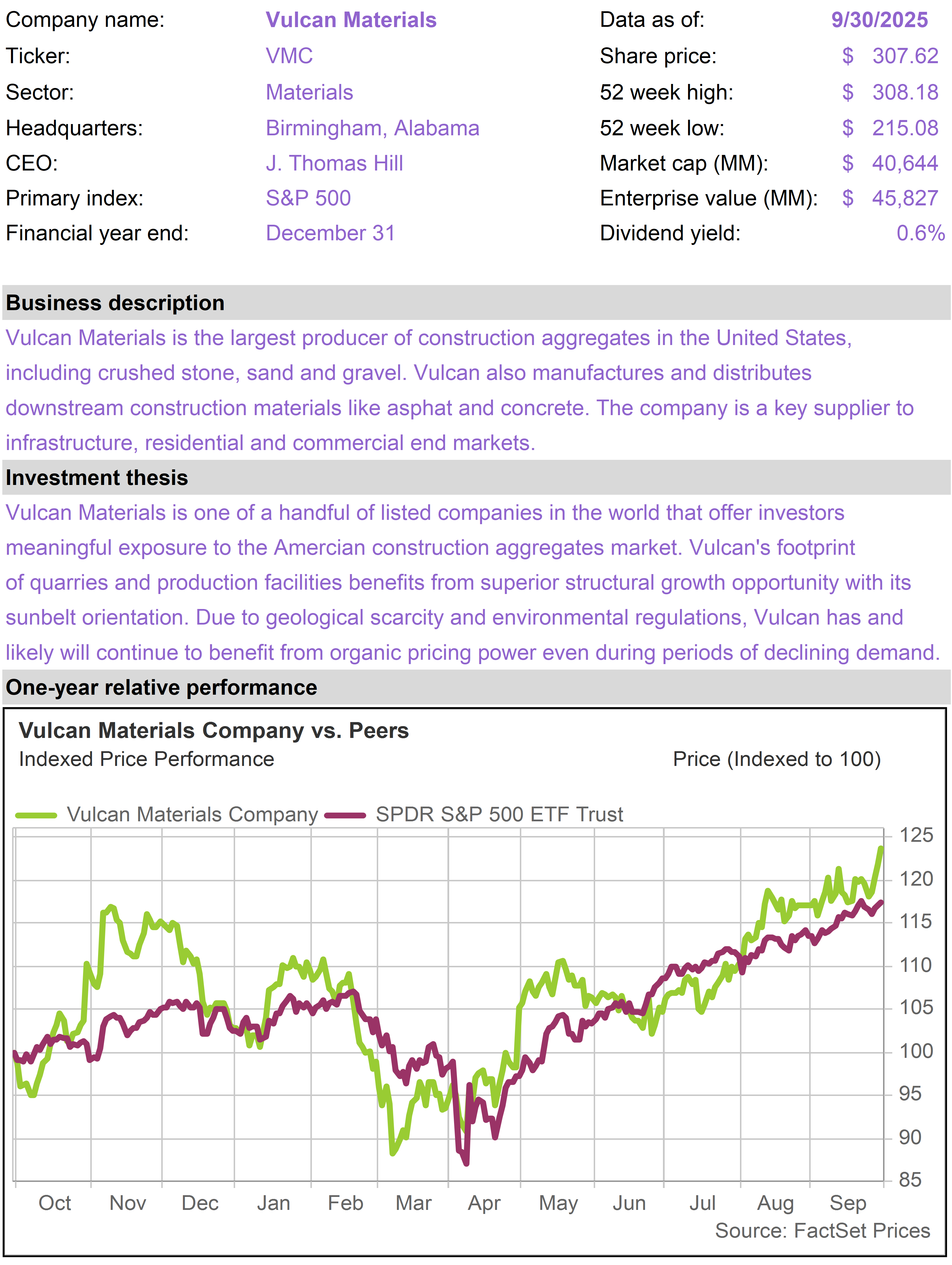

| | The 76research Inflation Protection Model Portfolio emphasizes business models that benefit from inflationary pressure. Holdings are typically selected from industries based on supply constrained real assets, including commodity and energy businesses, or companies that otherwise demonstrate superior pricing power. Drawing from an investable universe of expected inflation beneficiaries, specific holdings are chosen based on valuation and general business quality, growth and risk considerations. |

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | |

|

|

|

|

| |

|