As we noted above, tech stocks can be quite volatile. When bad news surfaces, tech investors often shoot first and ask questions later.

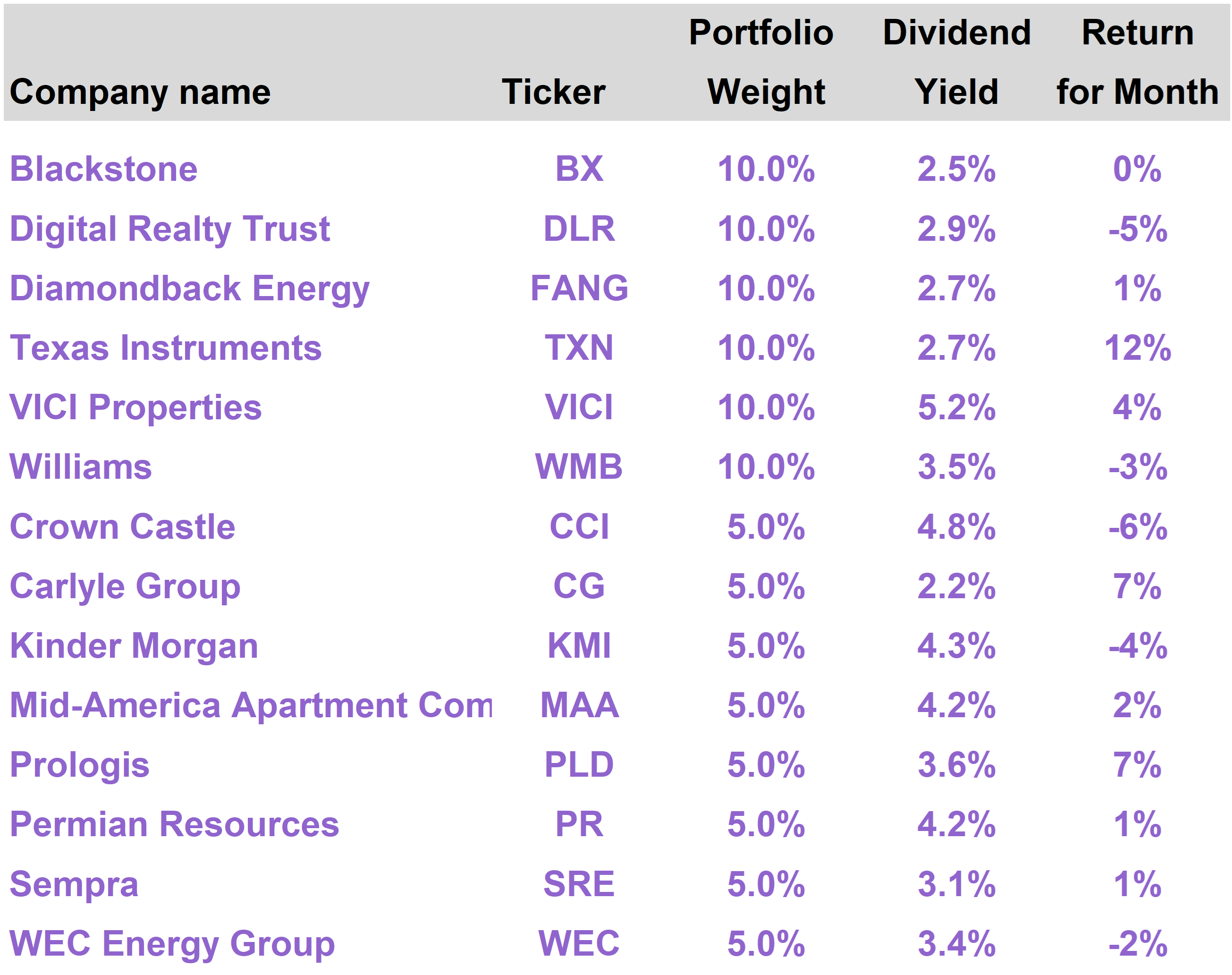

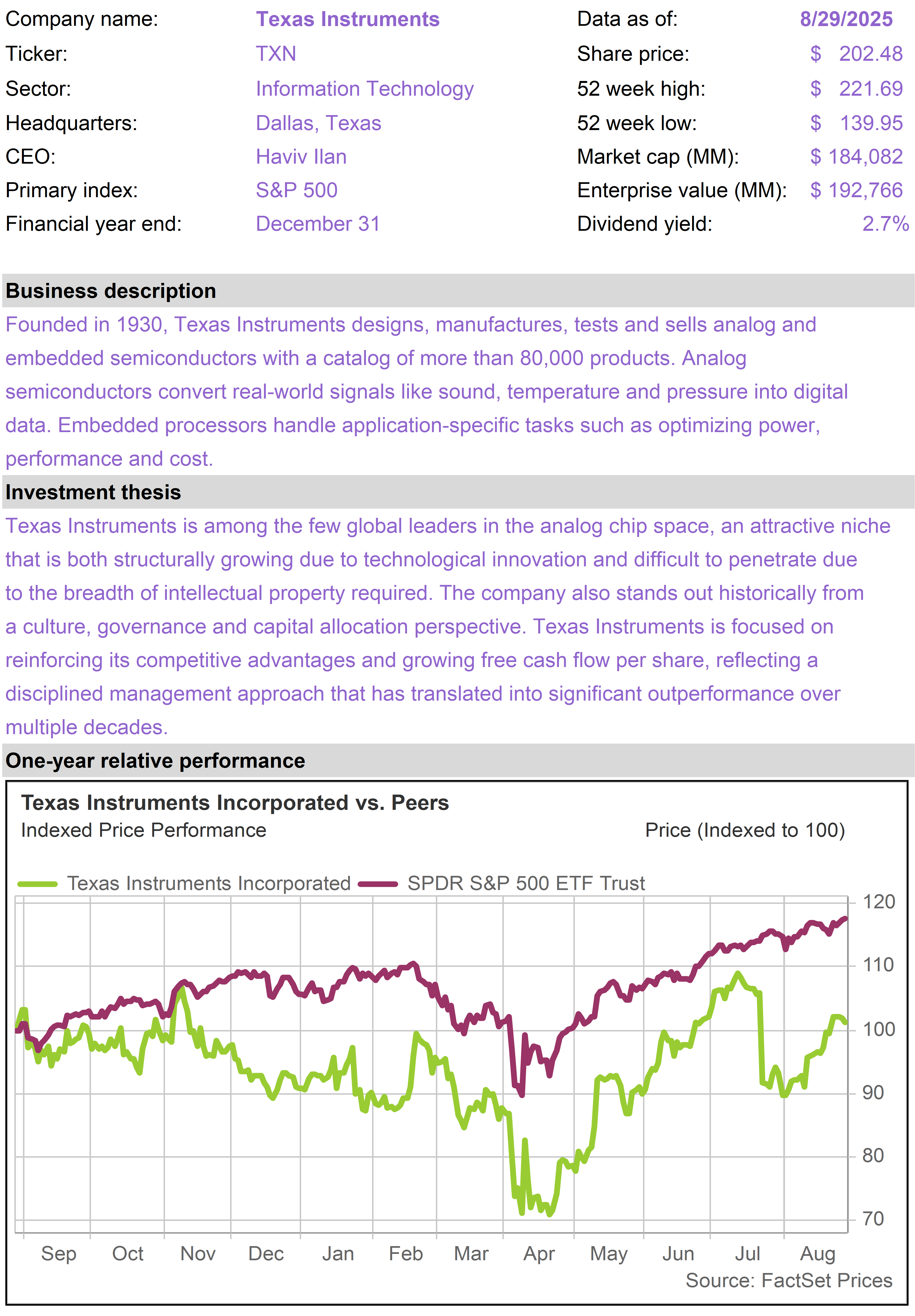

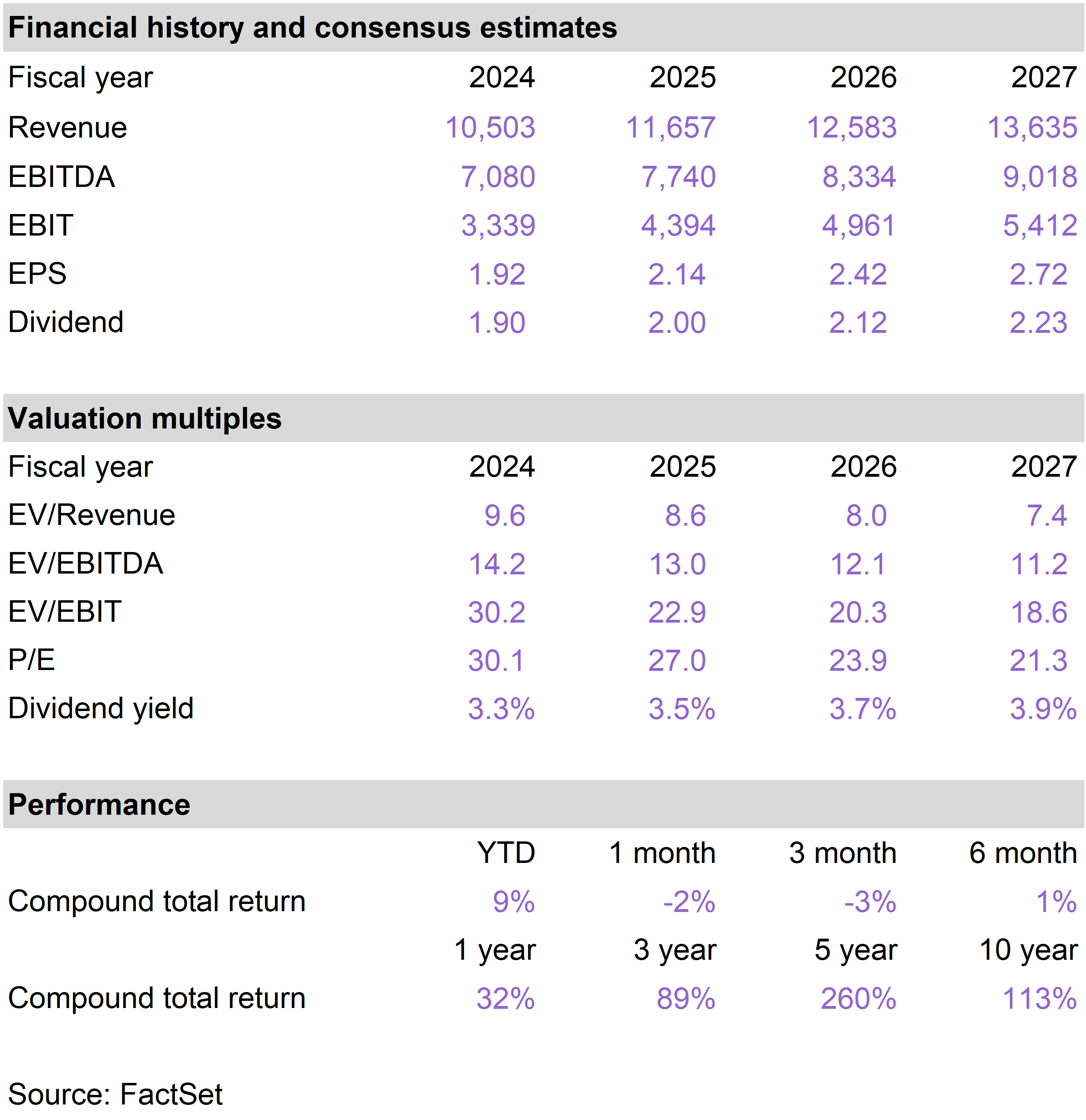

As we explained last month, shares of TXN saw weakness after its earnings report. We interpreted this as an overreaction to the company’s slightly cautious view on next quarter’s revenue. The main issue was whether or not sales in China saw a pre-tariff bump that would then reverse.

TXN recovered sharply in August and benefited from a few helpful developments. Its smaller analog semiconductor peer Analog Devices (ADI) reported a solid quarter and traded higher. This gave investors comfort on broader market conditions for players in the space.

There was also a report mid-month from a widely followed analyst at Sanford Bernstein that TXN has boosted prices on tens of thousands of products in its catalog, which should directly benefit profit margins.

TXN sells low-cost analog semiconductors and processors with a product portfolio that exceeds 80,000 distinct options. The company enjoys dominant market share along with other technological advantages, which gives it the flexibility to impose price increases as needed.

We continue to view TXN as a structural beneficiary of AI-related innovation. The more AI finds its way into factories, homes, equipment and vehicles, the more demand there will be for TXN’s vast product portfolio.

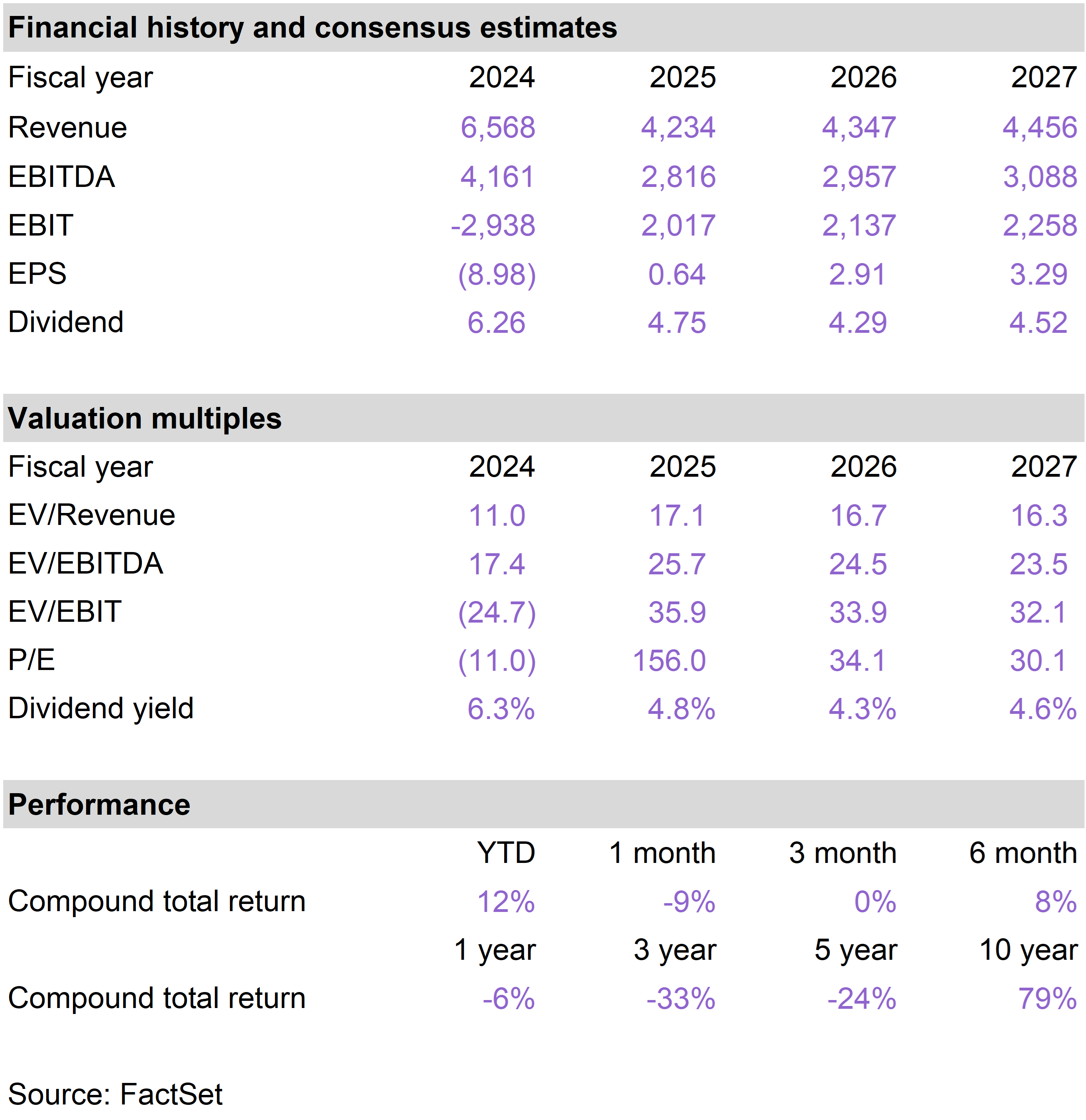

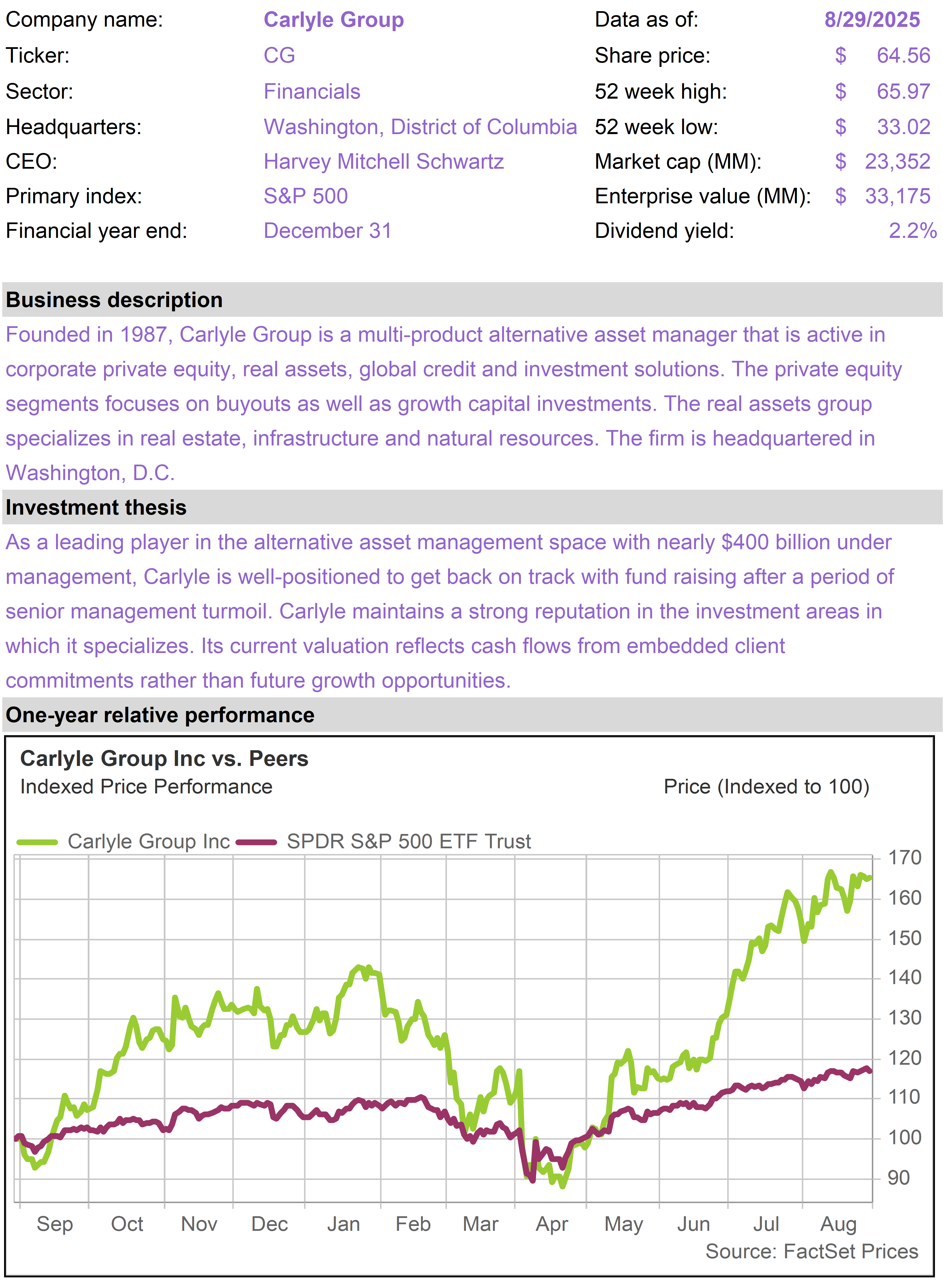

CG has emerged as the star of the portfolio this year, having now returned 30% on a year to date basis. Although a rising share price has raised the bar in terms of expectations, CG saw additional upside after reporting very impressive second quarter earnings earlier in August.

One of the nice things about asset managers is that they have the ability to scale up their business at fast rates if they perform well. CG has been executing quite well in recent quarters and is now growing at a much faster pace.

Fee-related earnings reached record levels during the most recent quarter with year over year growth of 18%. CG also boosted its fundraising guidance for the year from $40 billion to $50 billion.

CG is growing its asset base across multiple investment categories. As assets under management increase, so does its earnings power, justifying the higher valuation.

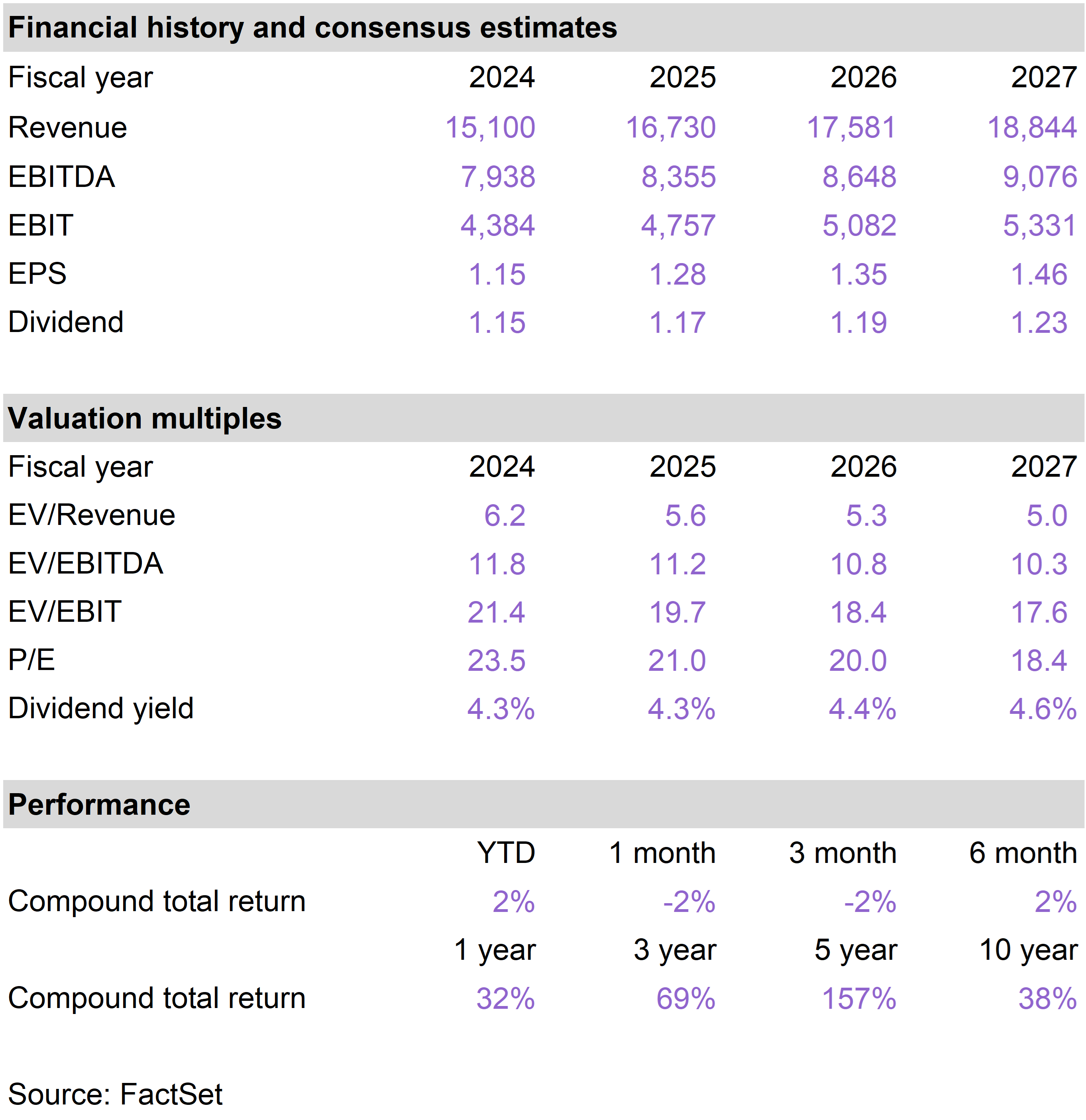

PLD shares performed well following a solid second quarter earnings result and with incrementally growing optimism towards the logistics space.

The core issue with PLD is finally moving beyond the excess capacity in industrial real estate (warehouses) from the pandemic era—when e-commerce operators invested heavily.

More recently, tariff uncertainty has tended to delay decision-making among customers and has impacted their willingness to make large commitments.

As spare capacity burns off and tenants become more comfortable with the tariff outlook, PLD is well-positioned to get back towards historical growth rates.

The company notes that market rents are now 20% below replacement cost rents (the rent required for a new project to earn an acceptable return).

This is a positive sign in that new capacity growth should remain constrained because it is not economically viable. It also sets the stage for significant rent increases once the spare capacity situation finally becomes tight.

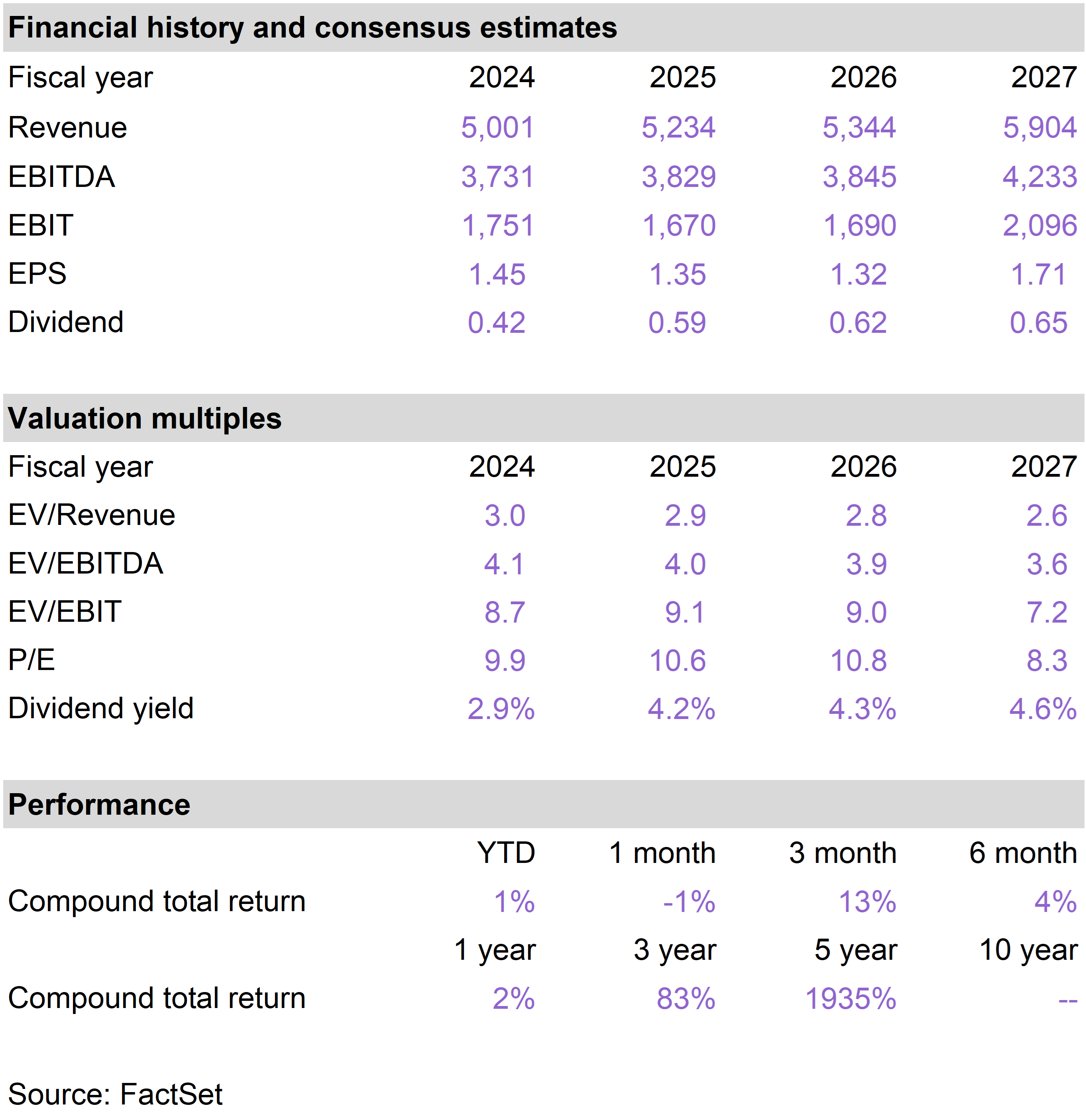

CCI’s core tower business remains in solid shape, underpinned by long-term contracts with escalators, but with a newly announced CEO and a pending divestiture of its fiber business, the stock is not attracting a lot of investor interest.

In the meantime, investors can benefit from a nearly 5% dividend yield, even after the dividend was downsized to reflect reduced cash flows from the fiber sale.

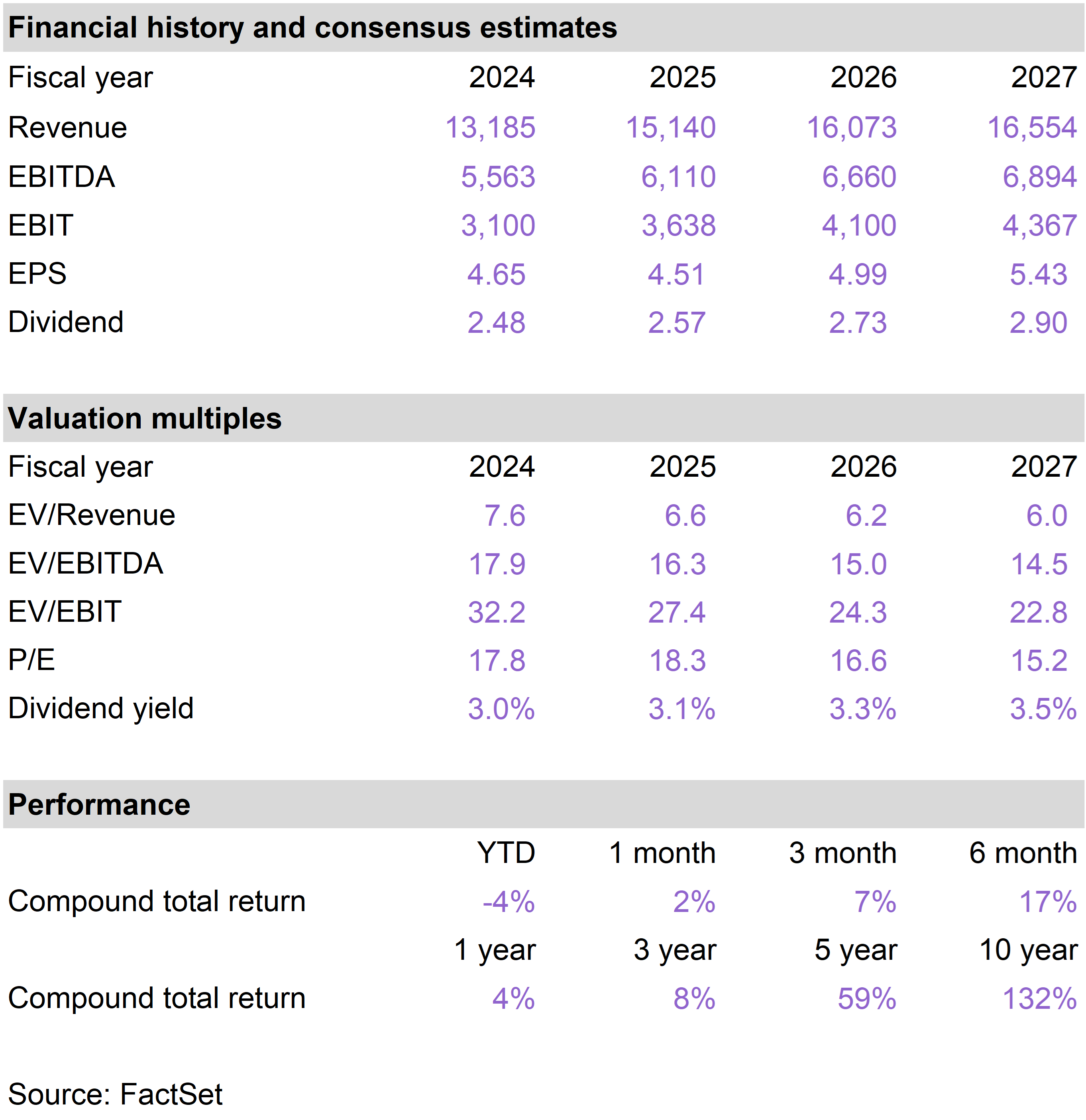

Despite delivering strong earnings and an encouraging outlook at the end of July, shares of DLR languished somewhat in August. In the absence of incremental news, this may relate to weaker sentiment towards the AI data center opportunity.

While investor sentiment may have ebbed a bit lately, we remain very optimistic about DLR’s long-term positioning as one of the world’s largest owners of data centers, where spare capacity is extremely tight and should remain so.

Through formal partnerships with some of the leading players in AI, including Oracle (ORCL) and NVIDIA (NVDA), DLR also has enormous development opportunities in the years ahead, leveraging its landbank and technical expertise.