“AI jitters”

We noted last month that it was possible that fiscal year-end window dressing contributed to the sharp tech outperformance we saw in October. Most stock funds end their fiscal years on October 31.

The idea was that fund managers were scrambling to add top performers (especially AI winners) to their portfolios by the end of the month. To the extent that happened, it raises the possibility that this non-fundamental demand driver disappeared in November.

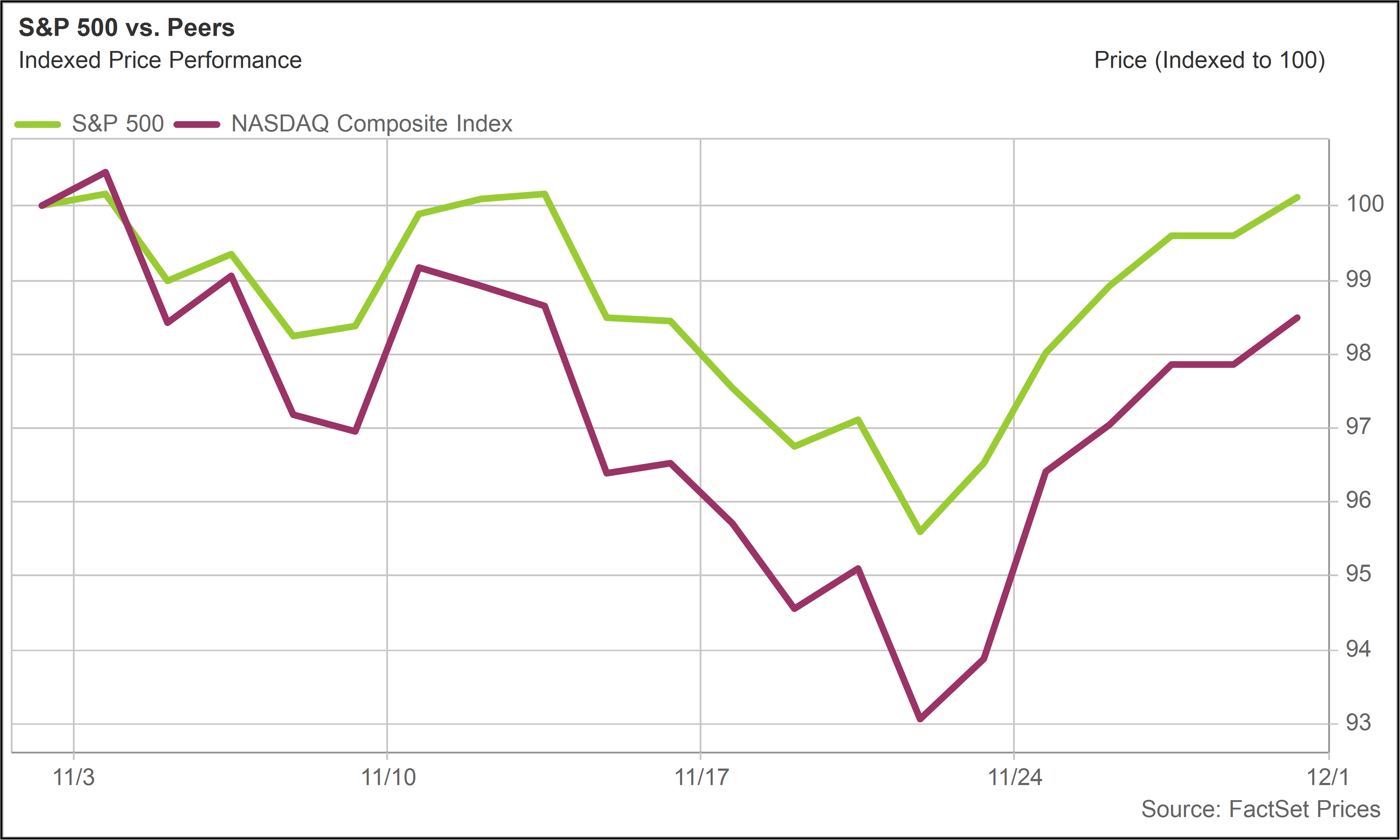

It is sometimes hard to read what exactly drives market movements. This month was arguably more difficult than others.

Often, there are clear market events that we can point to, such as the Liberation Day tariff announcements that sent stocks reeling in early April. In November, there was not an obvious or direct explanation for the tech-led mid-month sell-off.

Many financial media headlines made reference to “AI jitters”—in other words, the market reconsidering the sustainability of the AI infrastructure boom.

But even after NVIDIA (NVDA) reported genuinely strong earnings results on November 19, which initially lifted markets, the selling pressure continued, at least for another day, before seeming to exhaust itself.

The AI bubble debate resurfaced in November. This could have been either a cause or a result of the decline in tech stocks… or a little of both.

In other words, were investors selling stocks because they feared an AI bubble? Or were they talking about an AI bubble simply because tech stocks were correcting after several months of strong outperformance?

What matters ultimately is how these companies perform in the years ahead, not what the market mood meter read at some point along the way. Investors should always anchor to long-term expectations for profitability.

Are rate cuts done?

Alongside AI-related anxiety, the market became preoccupied in November with statements from various Federal Reserve officials. Ever since the Jackson Hole meeting in August, investors have been counting on a trajectory of incremental rate cuts. But in November, doubts surfaced.

The S&P 500 actually peaked at the very end of October, just prior to the most recent Fed meeting. Although the Fed cut rates another quarter point at that meeting, Fed Chair Jerome Powell made one comment in particular that bothered the market—that it was “not a foregone conclusion, far from it” that we would see another rate cut in December.

Following this discouraging tidbit, several Fed officials in November made hawkish comments.

St. Louis Fed President Alberto Musalem added that the Fed has “limited room” to reduce rates further without becoming overly accommodative.

Minneapolis Fed President Neel Kashkari revealed that he did not support the October rate cut and remains undecided about December. He is not a voter this year but is scheduled to rotate onto the Committee in 2026.

All of this hawkish rhetoric weighed on markets for the first few weeks of November, coinciding with the persistent bearish sentiment toward AI.

New York to the rescue

A turning point finally came when John Williams, the President of the New York Fed, said: “I still see room for a further adjustment in the near term to the target range for the federal-funds rate to move the stance of policy closer to the range of neutral.”

In English, he was saying interest rates are still at such a high level that they are needlessly slowing the economy down, so there is room to cut.

Williams’ comments were interpreted as signaling that all this talk of no more rate cuts had gone too far. Technically, all voting members of the Federal Open Market Committee (FOMC) have equal input, but the President of the New York Fed carries extra weight.

The FOMC has 12 voting members at any given time: seven Governors, four regional Fed Presidents who get rotated in, and the President of the New York Fed (a permanent seat). The New York Fed is also responsible for operational control of monetary policy.

In terms of how power really flows behind the scenes, Fed watchers informally refer to the troika, which consists of the Fed Chair, the Fed Vice Chair, and the New York Fed President. Collectively, they set the agenda.

So when Williams spoke, it was interpreted as Fed leadership attempting to keep market expectations for more rate cuts intact. Williams’ comments came on November 21, the day after stocks bottomed for the month, and are largely responsible for the strong finish.

Short-term rates move slightly

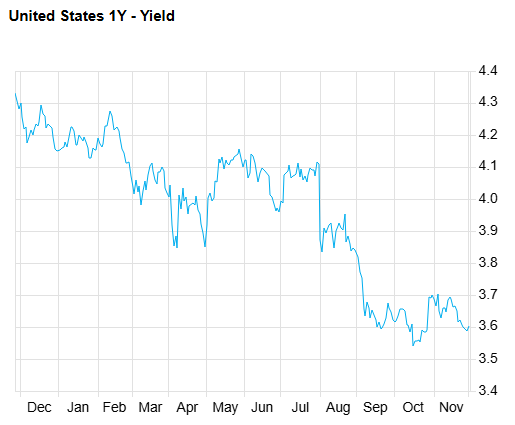

While the rhetoric around rate cuts may have been driving stock market sentiment, the impact on government bond yields was actually mild. One-year Treasuries, which reflect near-term rate cut expectations, approached 3.7% after the Fed meeting and declined toward 3.6% by the end of November.

It is worth noting that one-year Treasury yields have generally fluctuated between 3.6% and 3.7% for the past three months, suggesting no major shift in the trajectory of anticipated rate cuts.