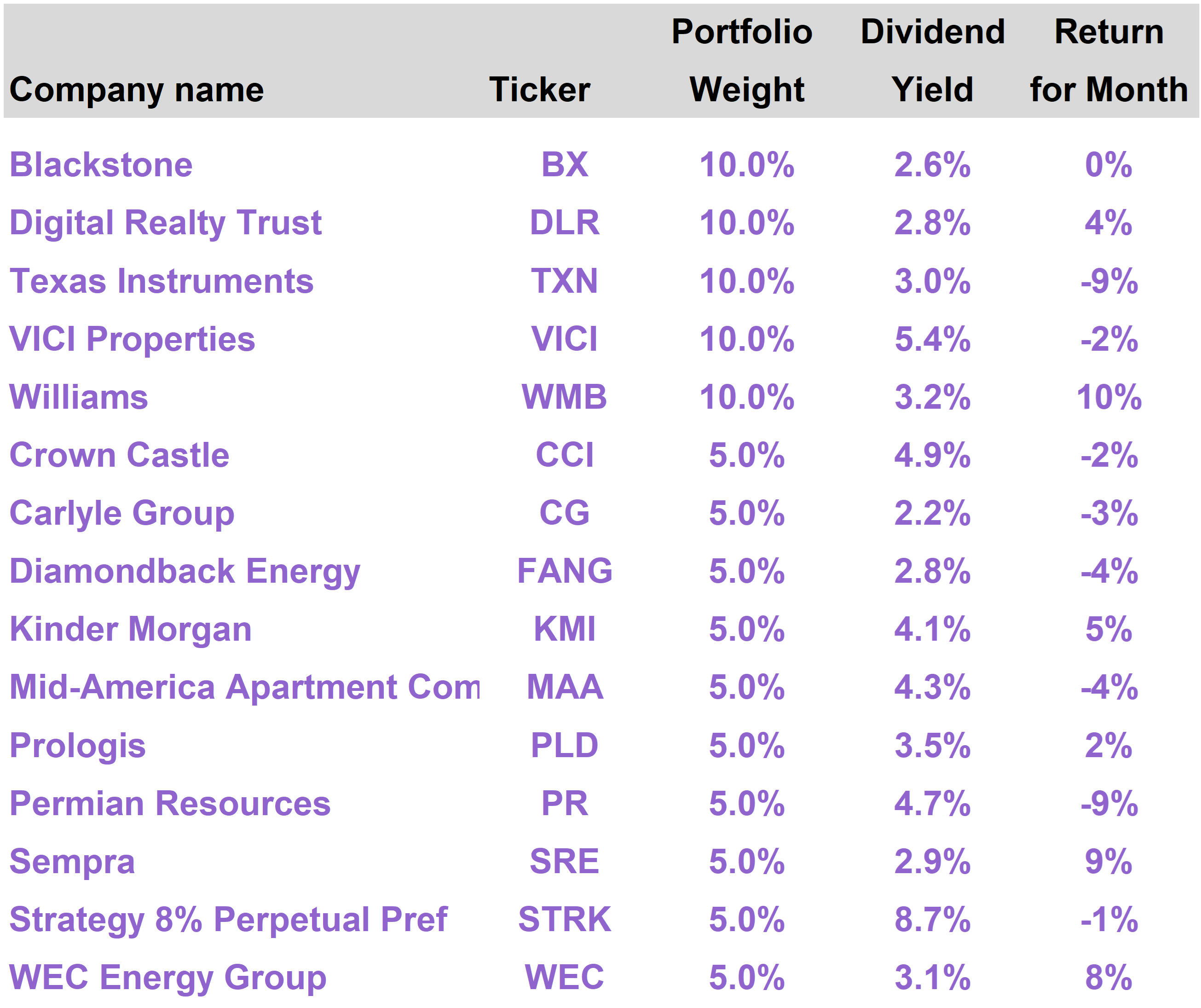

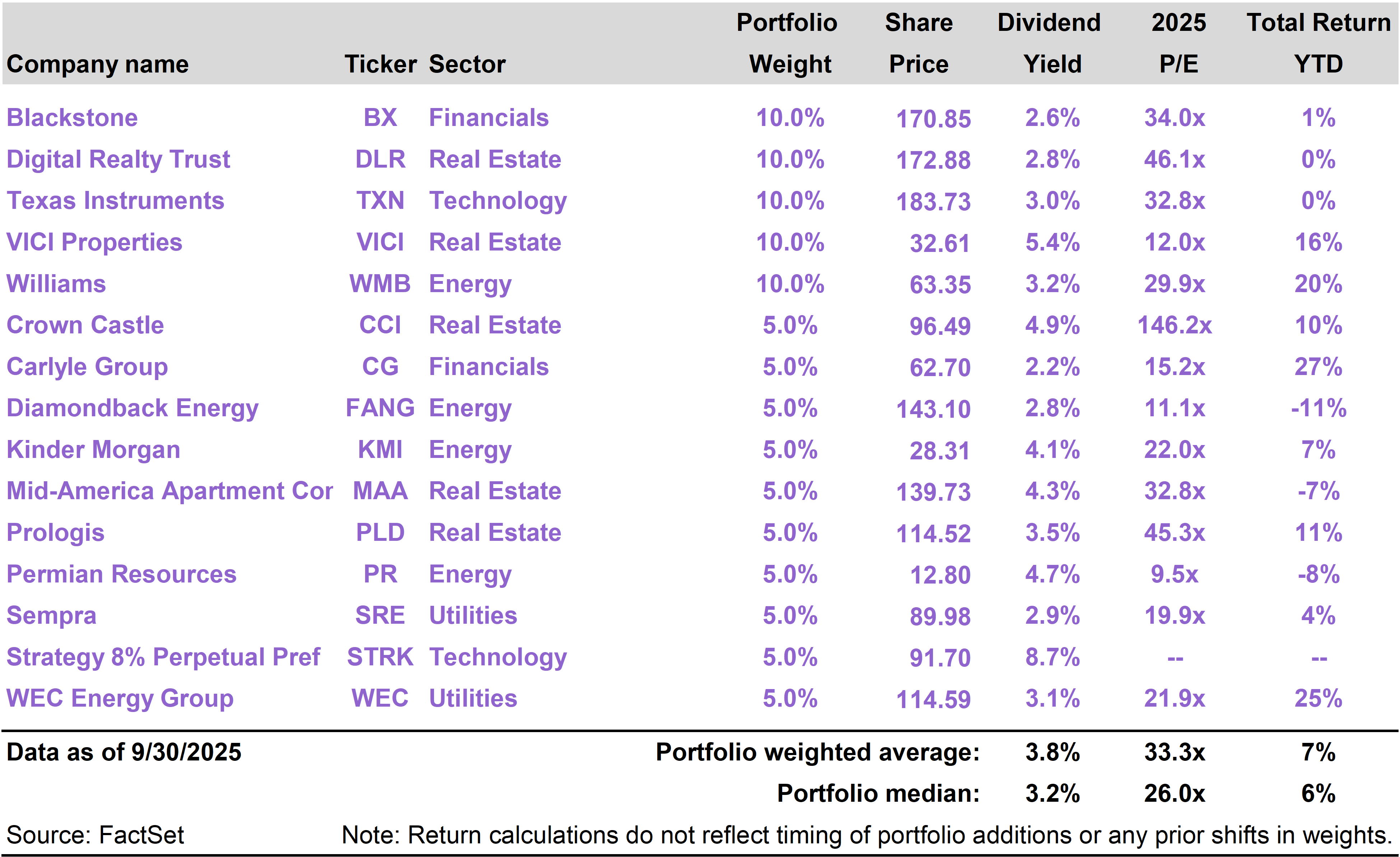

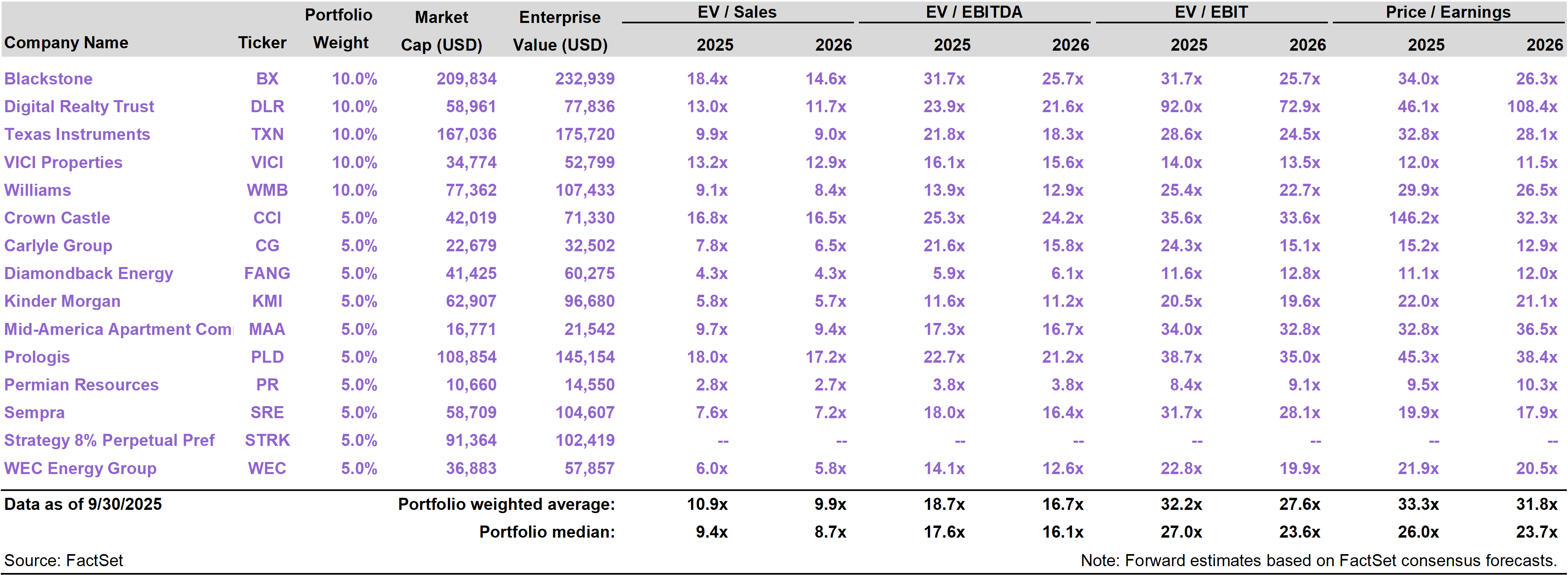

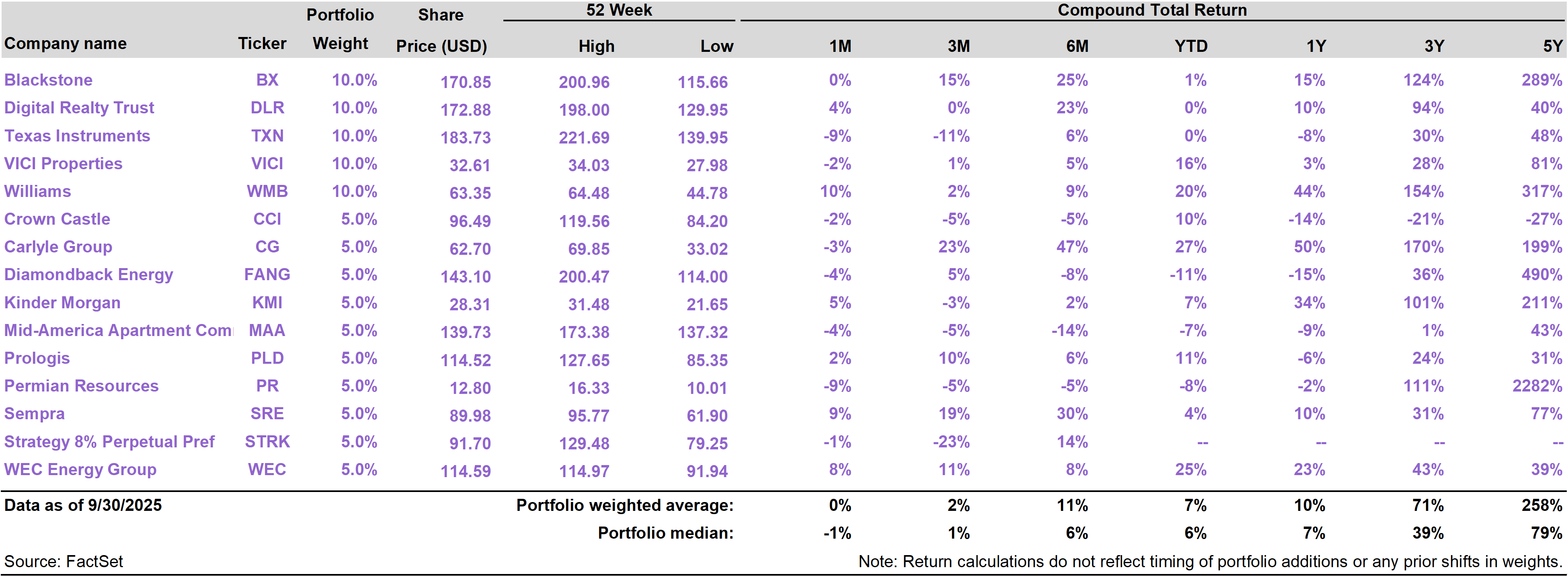

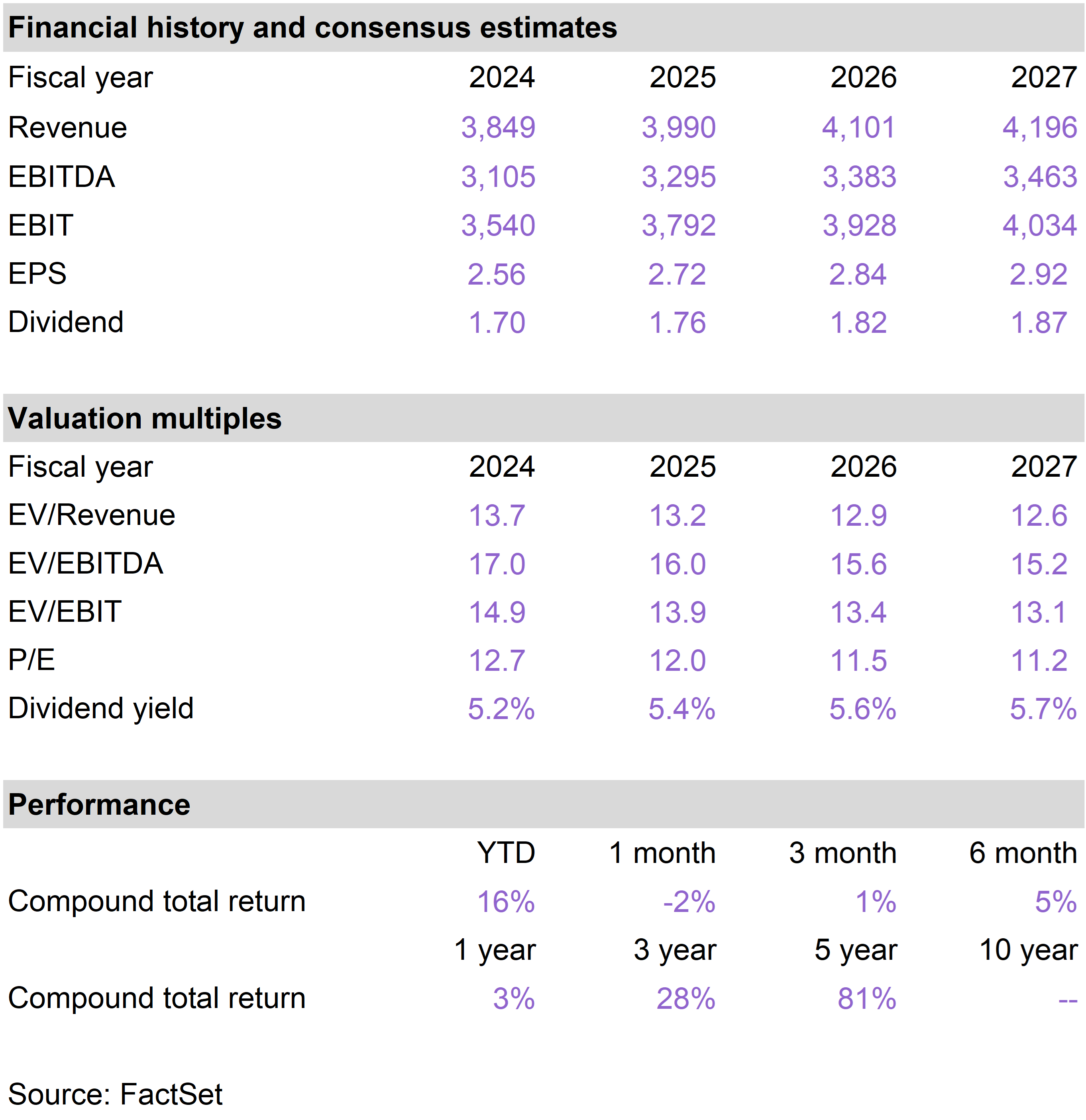

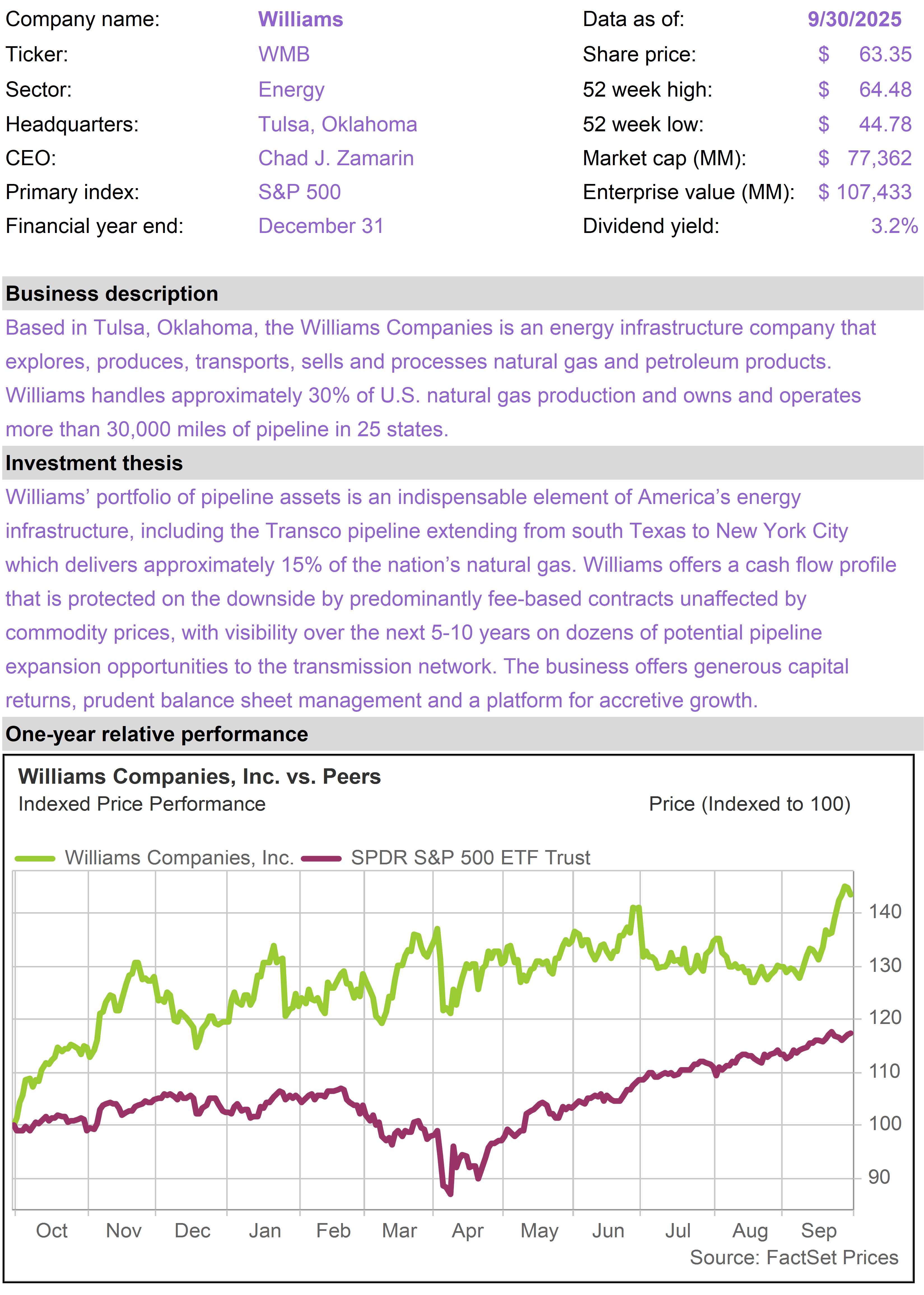

WMB performed well in September, reaching new all-time highs, on the heels of a well-received early September presentation at an investment conference that led analysts to boost medium-term expectations for the company.

As the leading natural gas infrastructure player in the U.S., WMB owns irreplaceable assets and has many things going for it in the current environment.

The urgent power demands from AI data centers under construction are creating investment opportunities for WMB—adjacent to its core pipeline assets—at high (20+%) rates of return.

The permitting environment since Trump came into office has significantly improved. In addition to AI-driven projects, WMB has ample growth opportunities in Liquefied Natural Gas (LNG) exports.

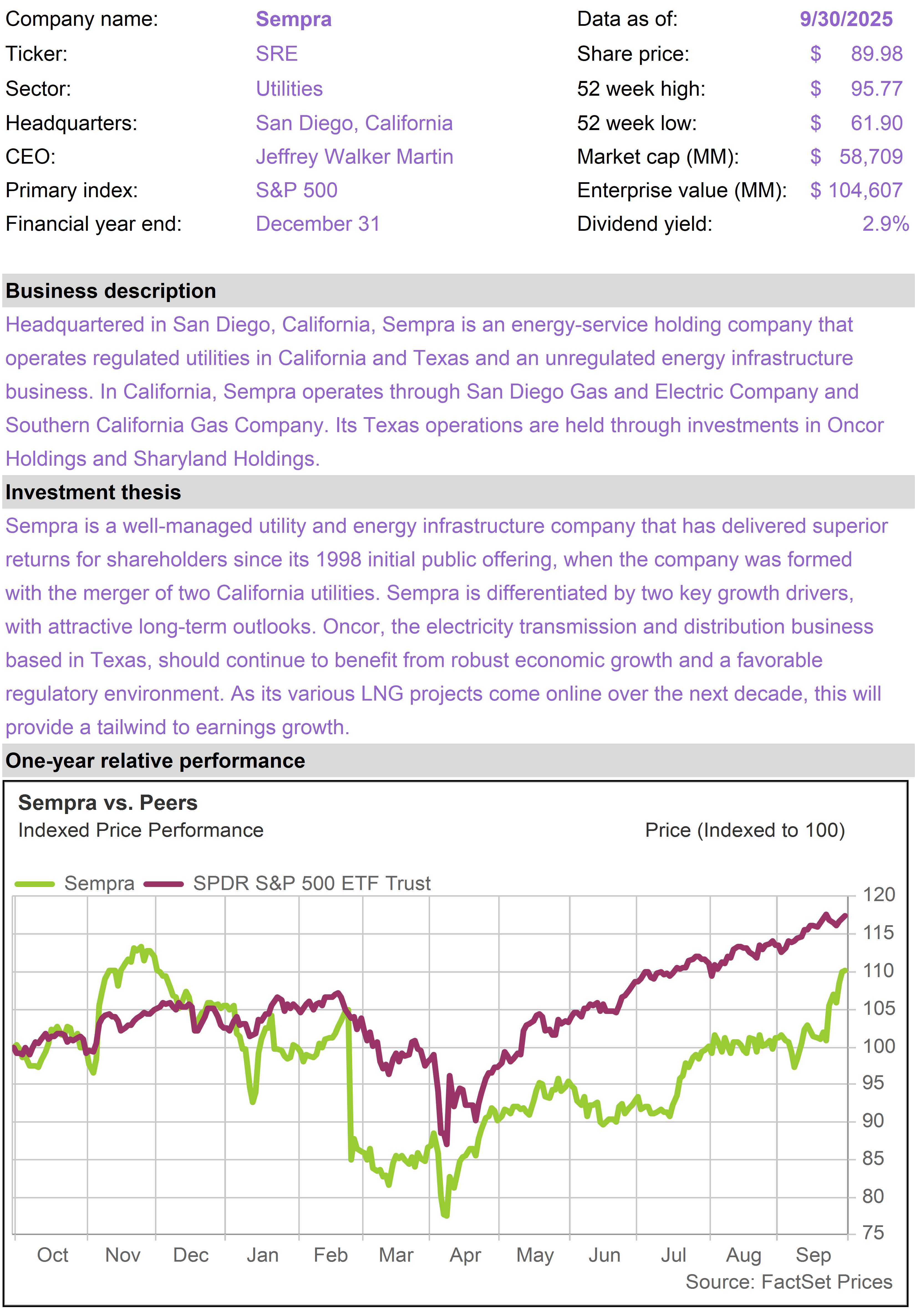

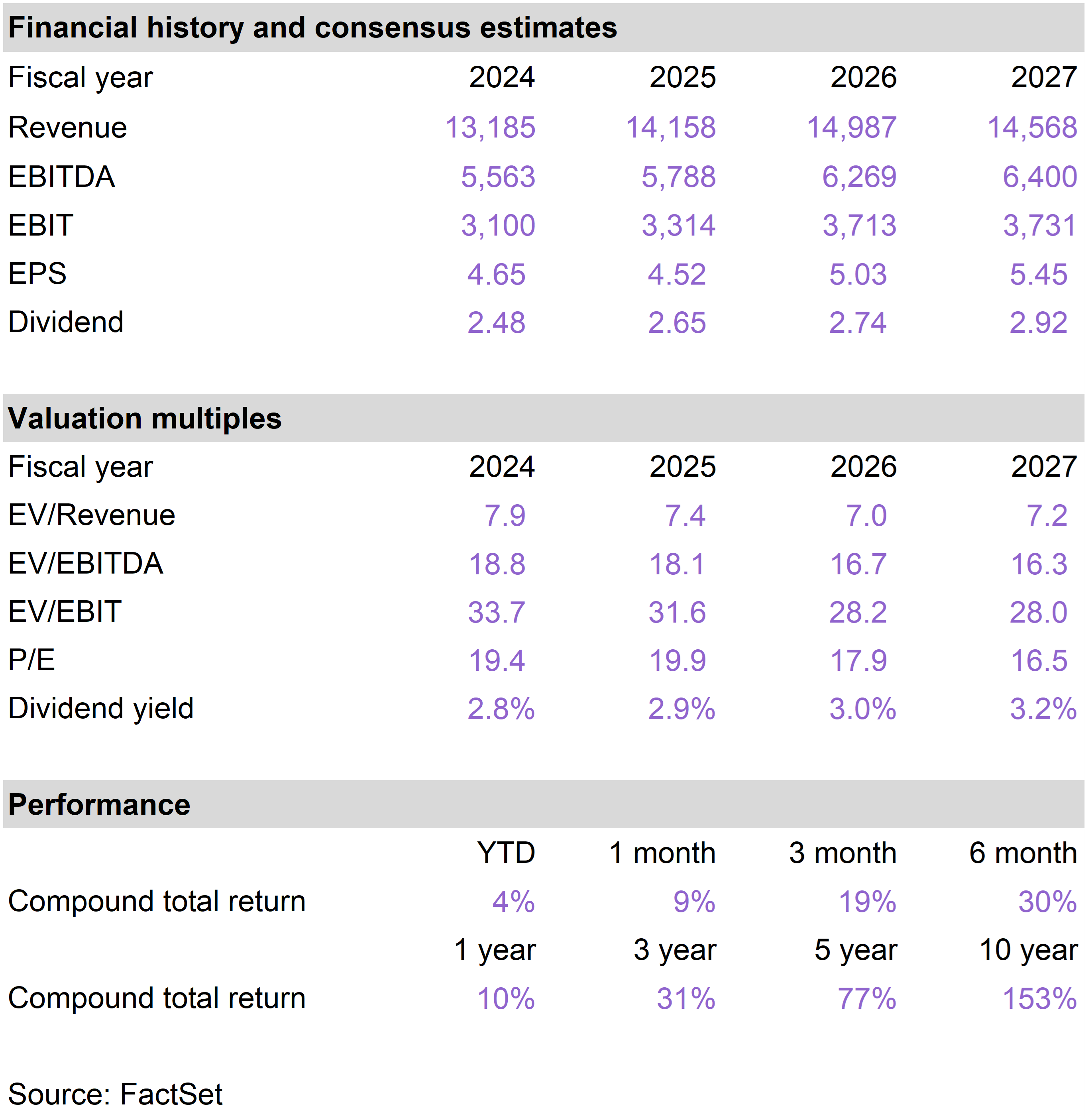

LNG is also part of the reason shares of SRE advanced this month. SRE announced that it is selling 45% of its stake in Sempra Infrastructure Partners (SIP) to private equity players at an attractive valuation.

While the bulk of SRE’s business consists of regulated utilities in Texas and California, SIP owns unregulated LNG, natural gas pipeline and other energy infrastructure assets.

In addition to the high valuation that was obtained, the market responded positively to the company’s expectation that the deal will be materially accretive to earnings and improve its credit metrics.

We continue to view SRE as an attractive defensive stock with growth potential in both its regulated electric utility segment and through its unregulated infrastructure activities.

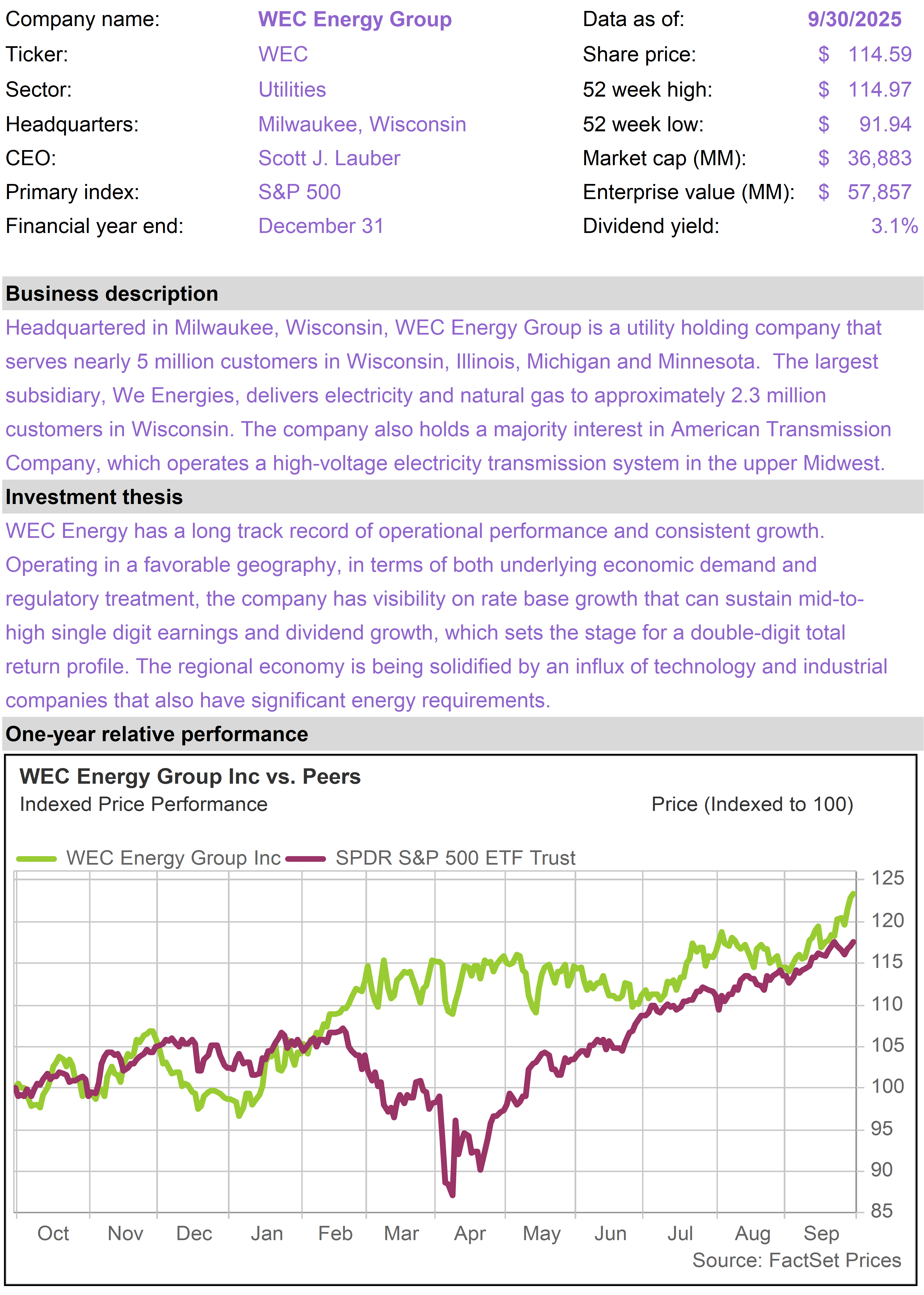

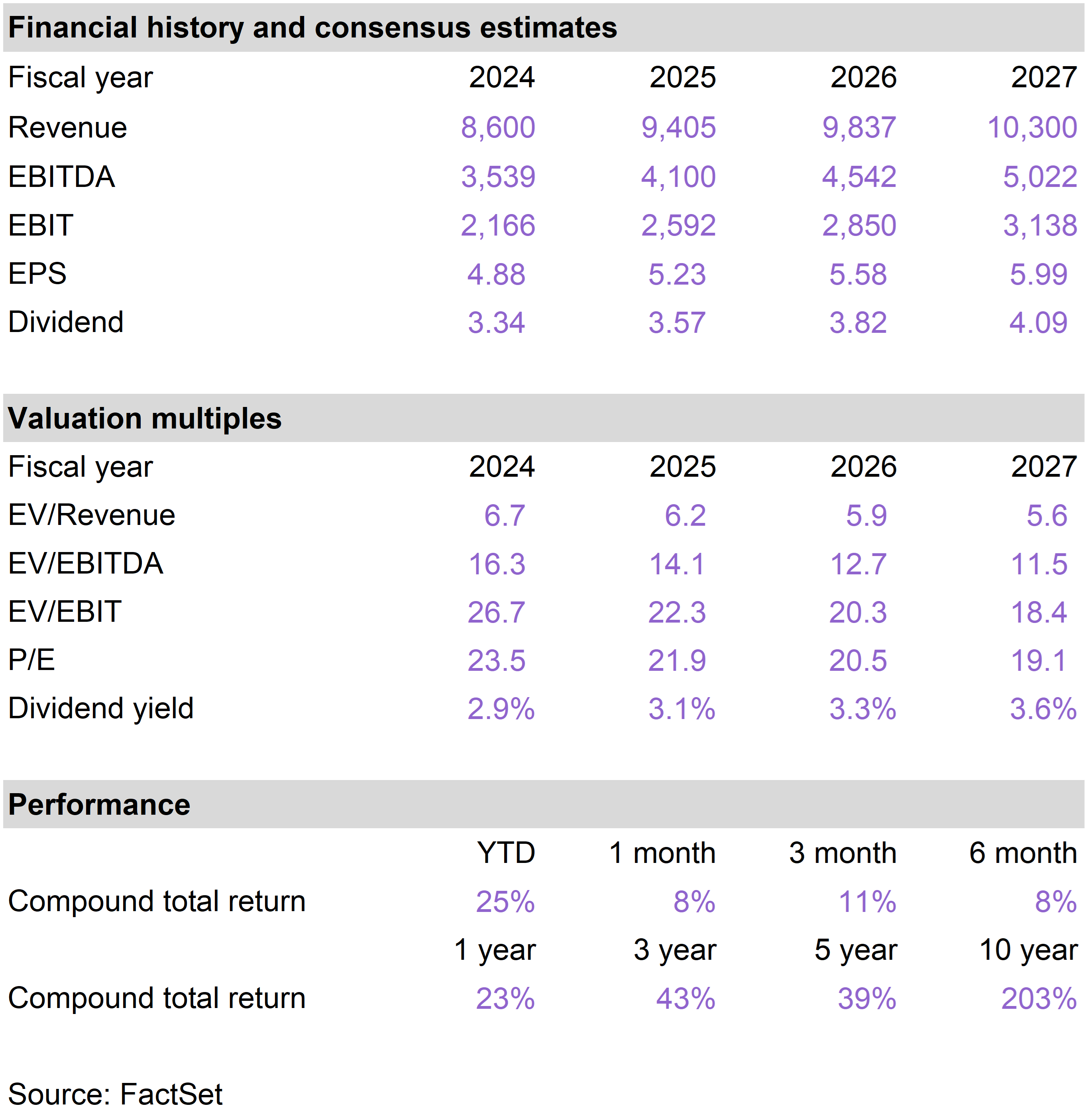

WEC, the portfolio’s other utility stock, advanced in September as well. The company’s regulated electric and gas utilities extend across Wisconsin and some other midwestern states.

Wisconsin may have a somewhat staid reputation. But the upper midwestern state’s solid, educated labor force and stable climate (with low risk of natural disasters relative to the rest of the country) are among the factors that are transforming it into an emerging data center hub.

In mid-September, Microsoft (MSFT) announced that it is committing an additional $4 billion to its Mount Pleasant, Wisconsin data center facility. This follows a $3.3 billion investment in the facility, the first phase of which is expected to launch in early 2026.

MSFT describes the project as “the world’s most powerful AI datacenter.” WEC will be providing the electrical power. WEC shares rose as analysts recalibrated their earnings growth estimates in the wake of this significant deal.

We continue to like WEC as a well-managed utility with stable and steady growth prospects that operates in a surprisingly attractive geography from a technology perspective.

We expect the region to thrive over time as more tech-driven investment flows into the I-94 corridor connecting Madison, Milwaukee and Chicago.

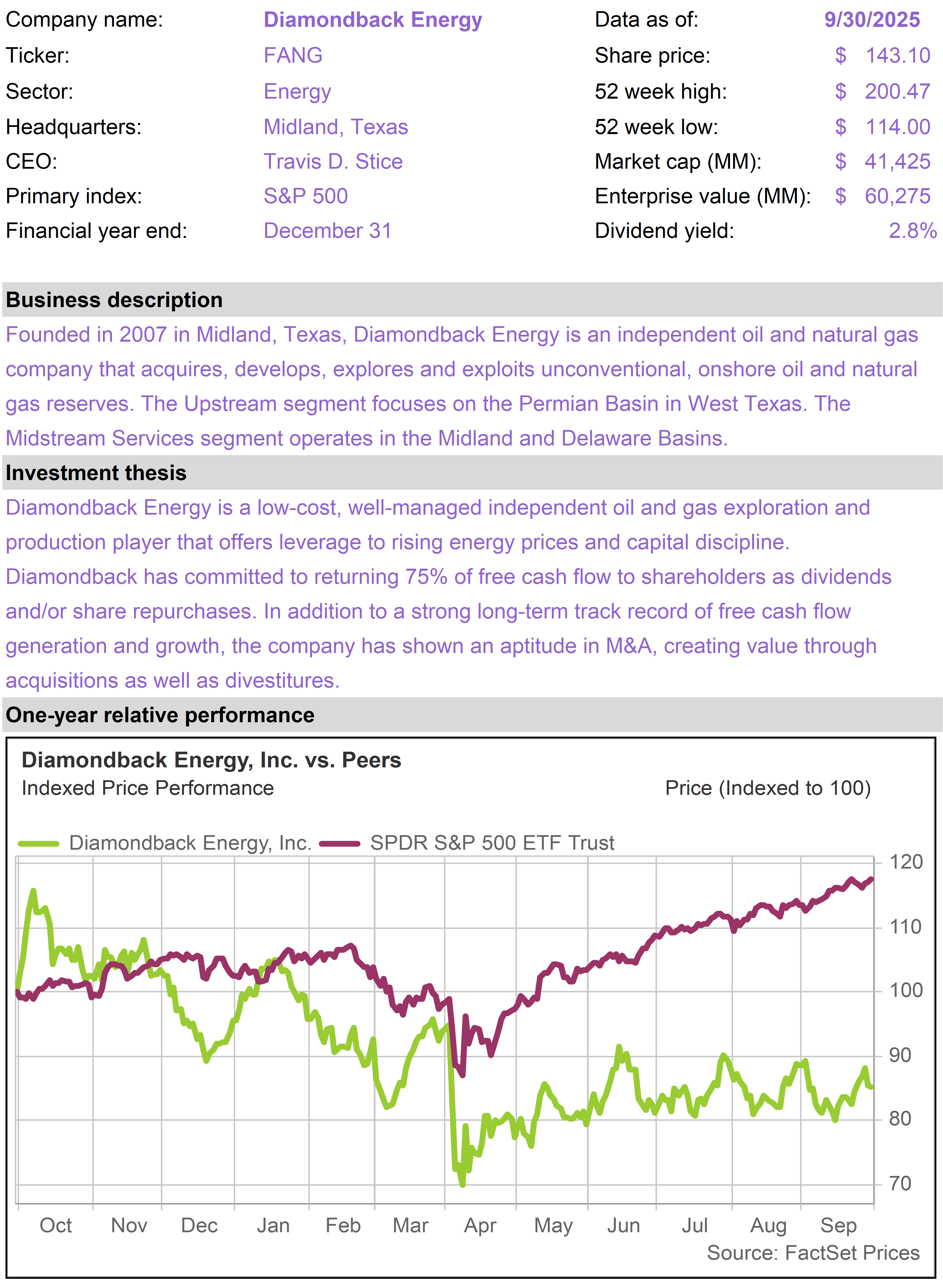

Shares of PR slid in September with oil price weakness. In early September, the company announced solid second quarter earnings results. Management continues to execute well but cannot control the oil price.

The shares are likely to remain out of favor so long as oil prices are soft, but they appear quite undervalued, even if one assumes a continuation of low oil prices.

By conventional valuation approaches, PR could fundamentally be worth as much as double its current share price. The company, which is relatively small, with very attractive oil and gas reserves, is also a long-term buy-out candidate.

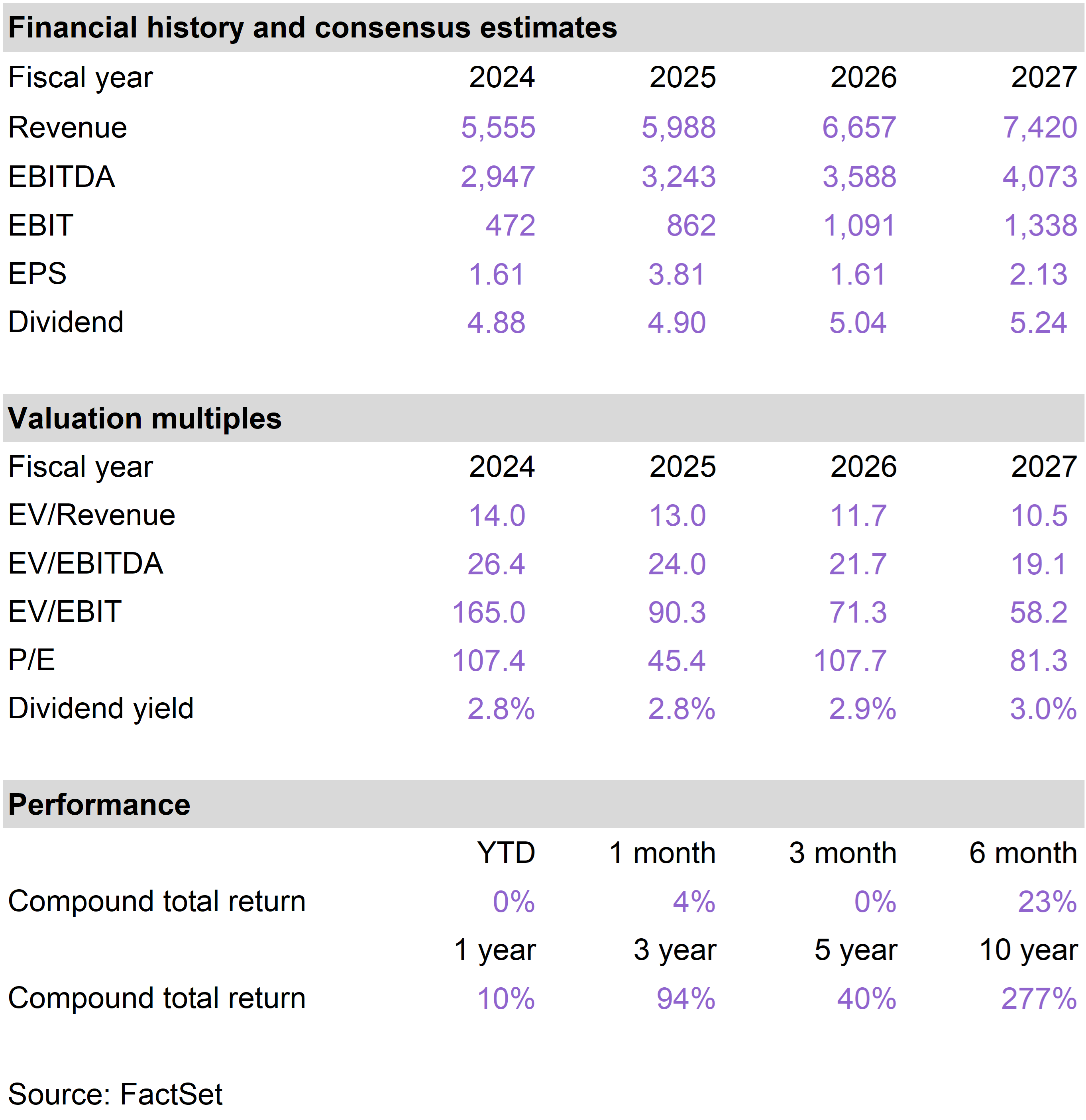

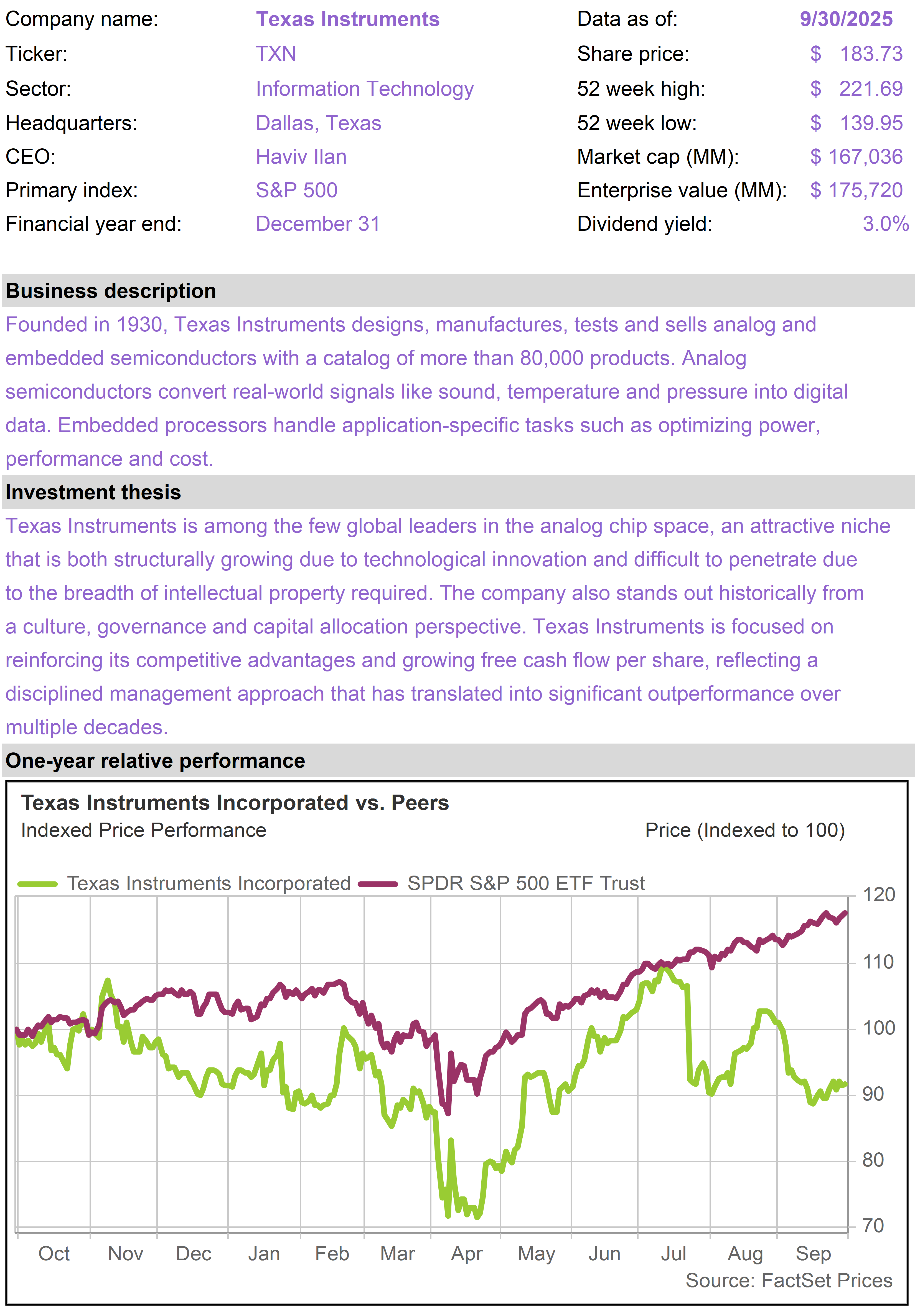

After a strong August performance, TXN gave back those gains. There was no specific catalyst but the weakness appears related to auto sector demand concerns as well as potential China tariff impacts.

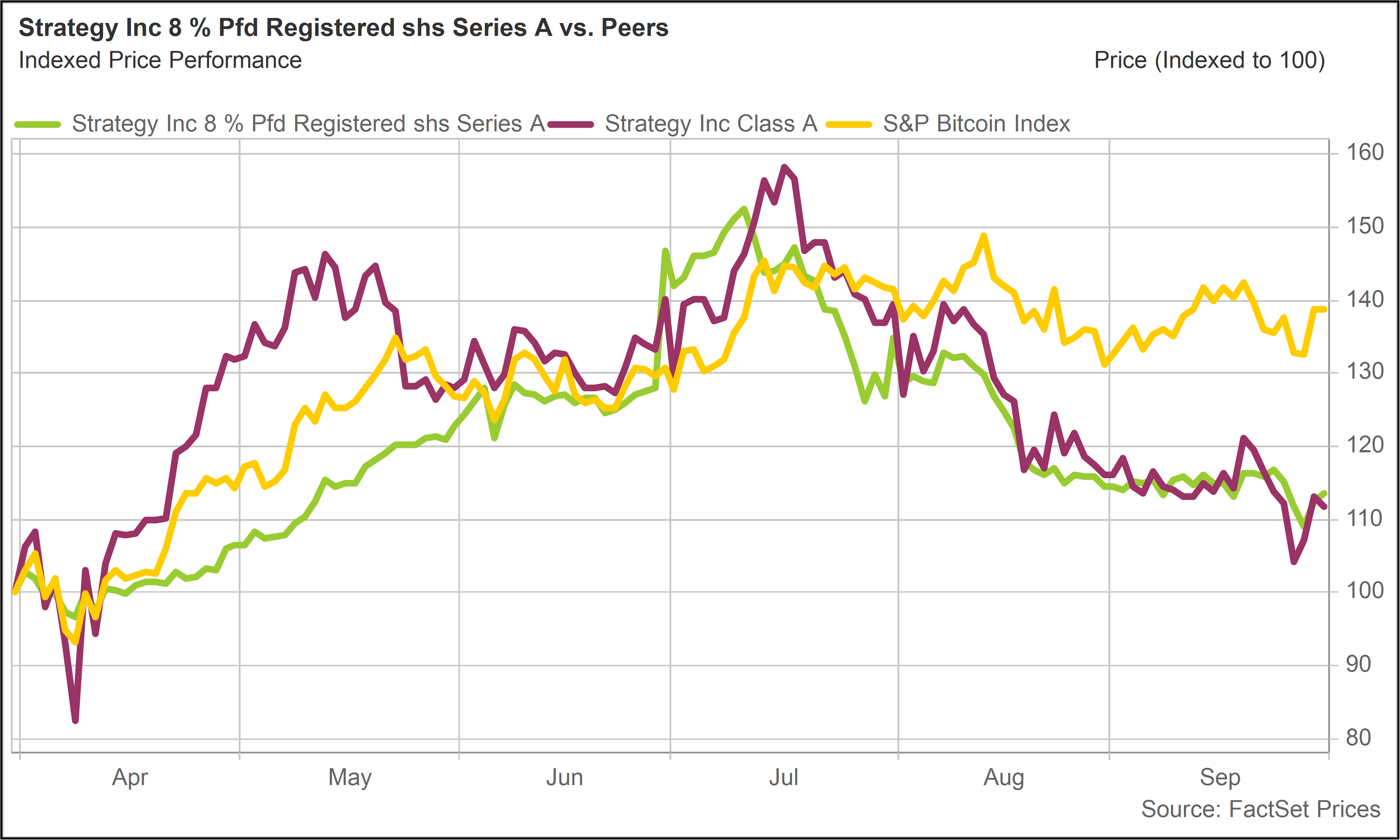

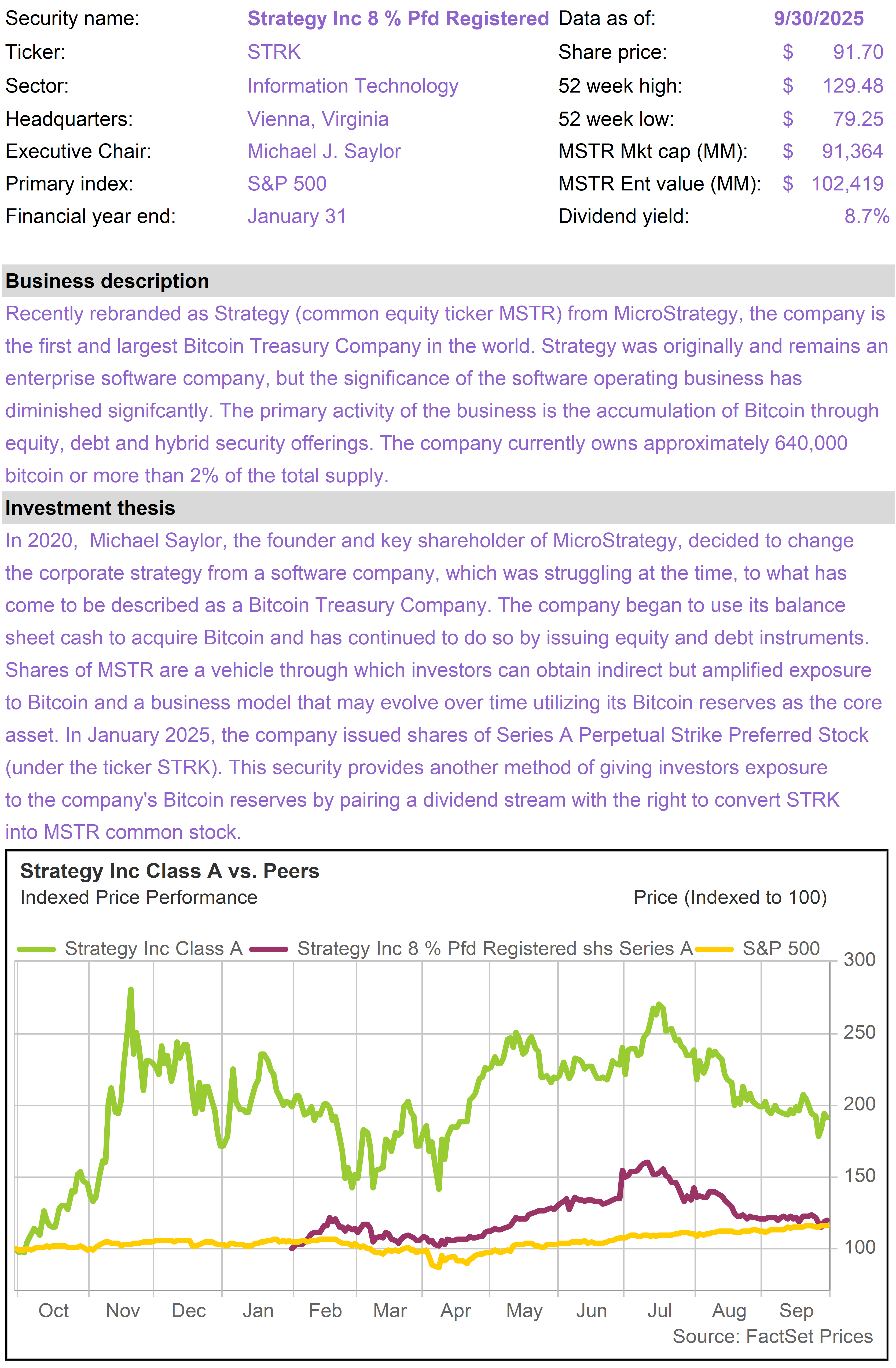

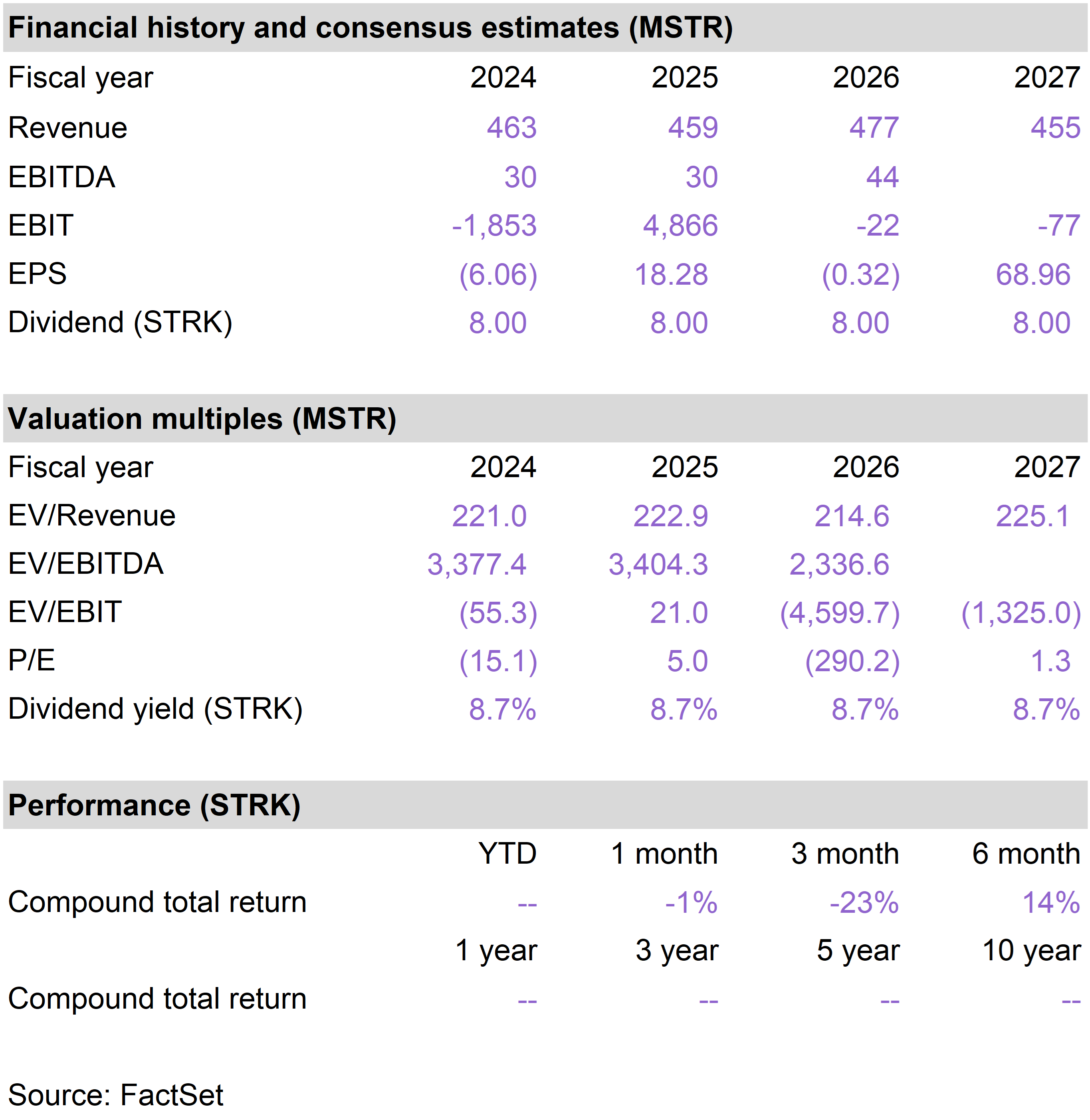

Adding STRK

We have written about STRK a number of times, initially on March 18, 2025 (High Yield with Bitcoin Upside). We encourage subscribers to review that note to understand how the security works.

Shares of STRK were around $85 at the time. They rose to as high as $125 in July but have since retreated to below $100.

In the meantime, Bitcoin has risen from about $83,000 to now, as we write, over $120,000, a few thousand away from its all-time high.

Although Bitcoin has performed well, investor sentiment towards Strategy (MSTR) has ebbed and its premium to underlying Bitcoin holdings has compressed.

Investors in STRK may have gotten a little overexcited this summer. The shares have since declined considerably, creating this current opportunity to add STRK to the portfolio.