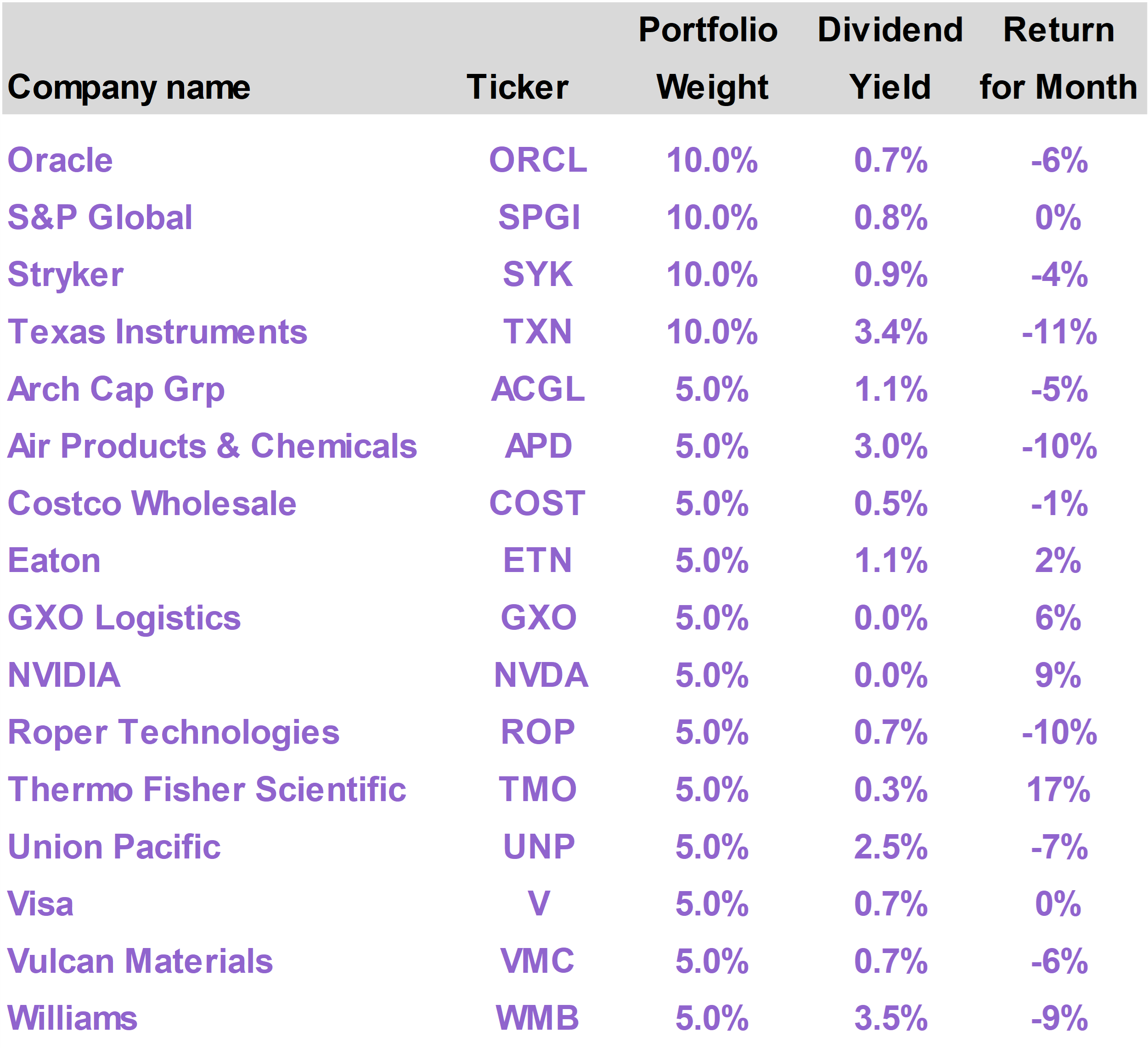

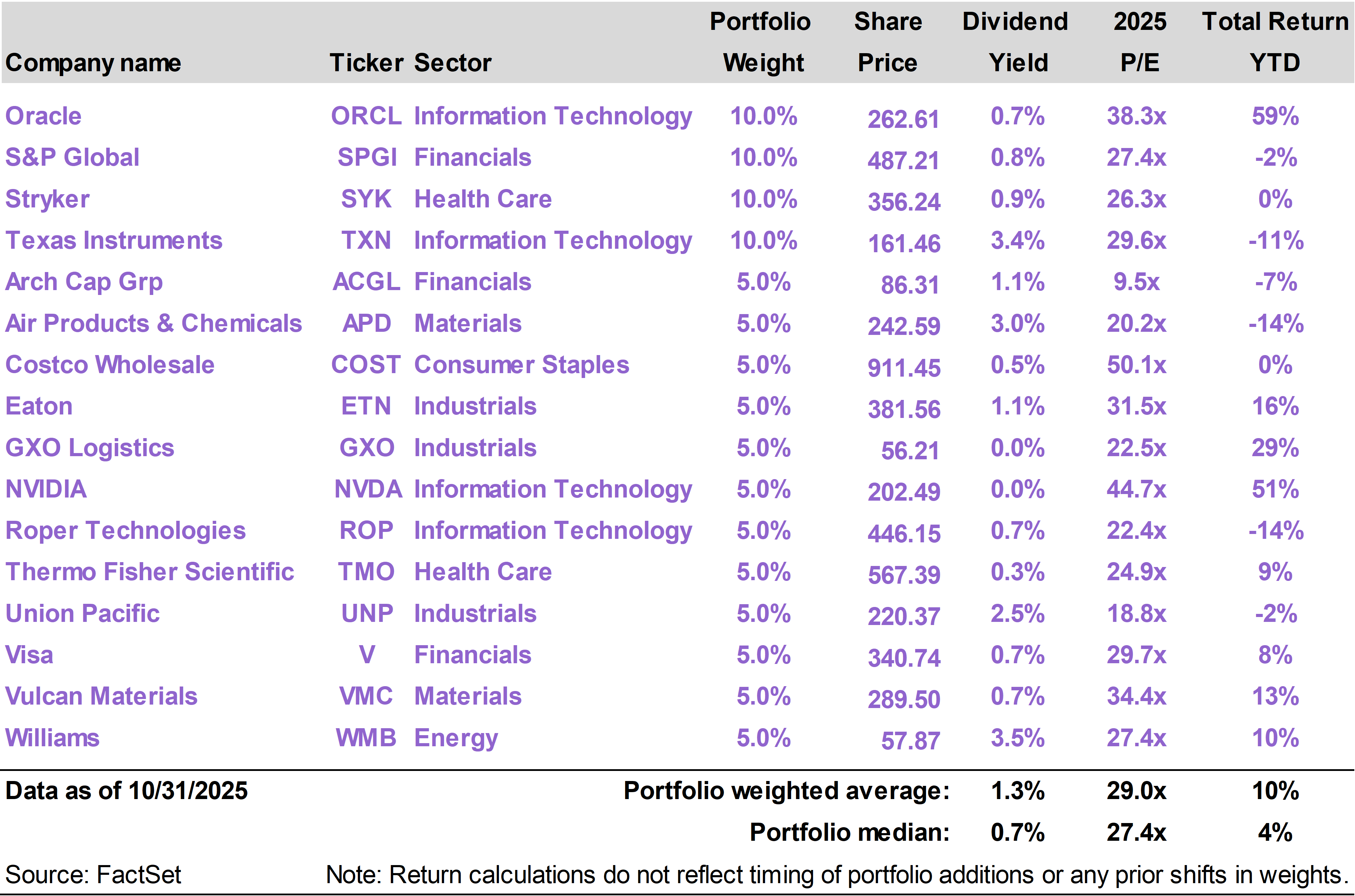

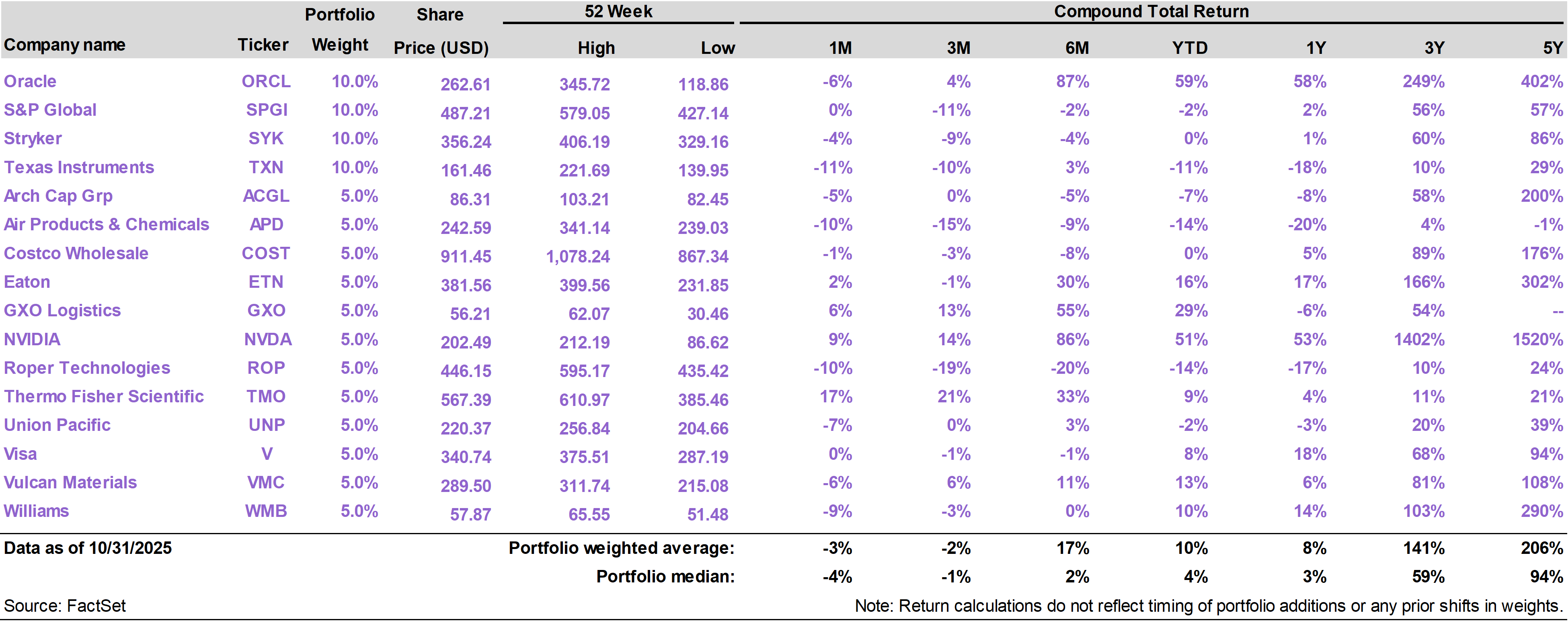

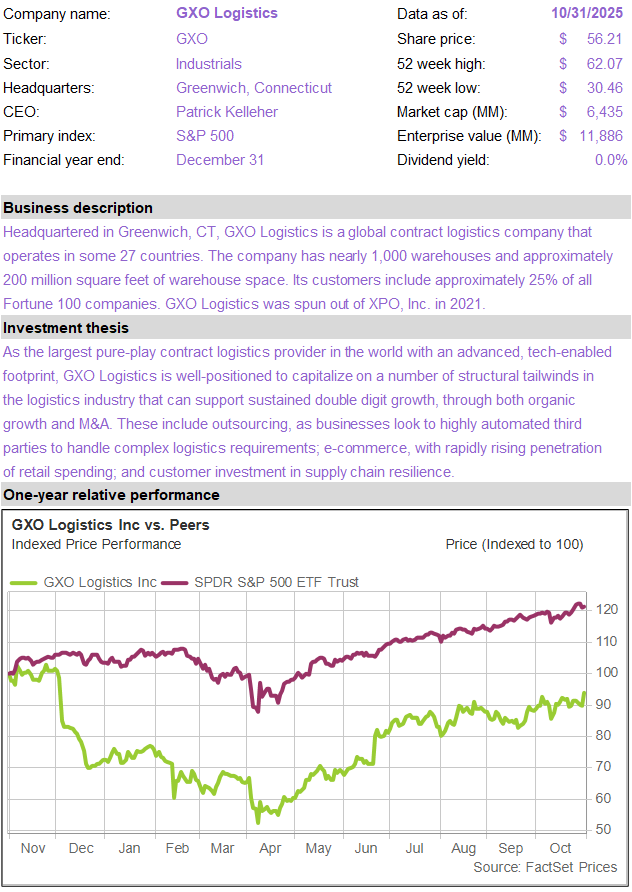

The top performing stocks in the portfolio in October were Thermo Fisher Scientific (TMO), which returned 17%; NVIDIA (NVDA), which returned 9%; and GXO Logistics (GXO), which returned 6%.

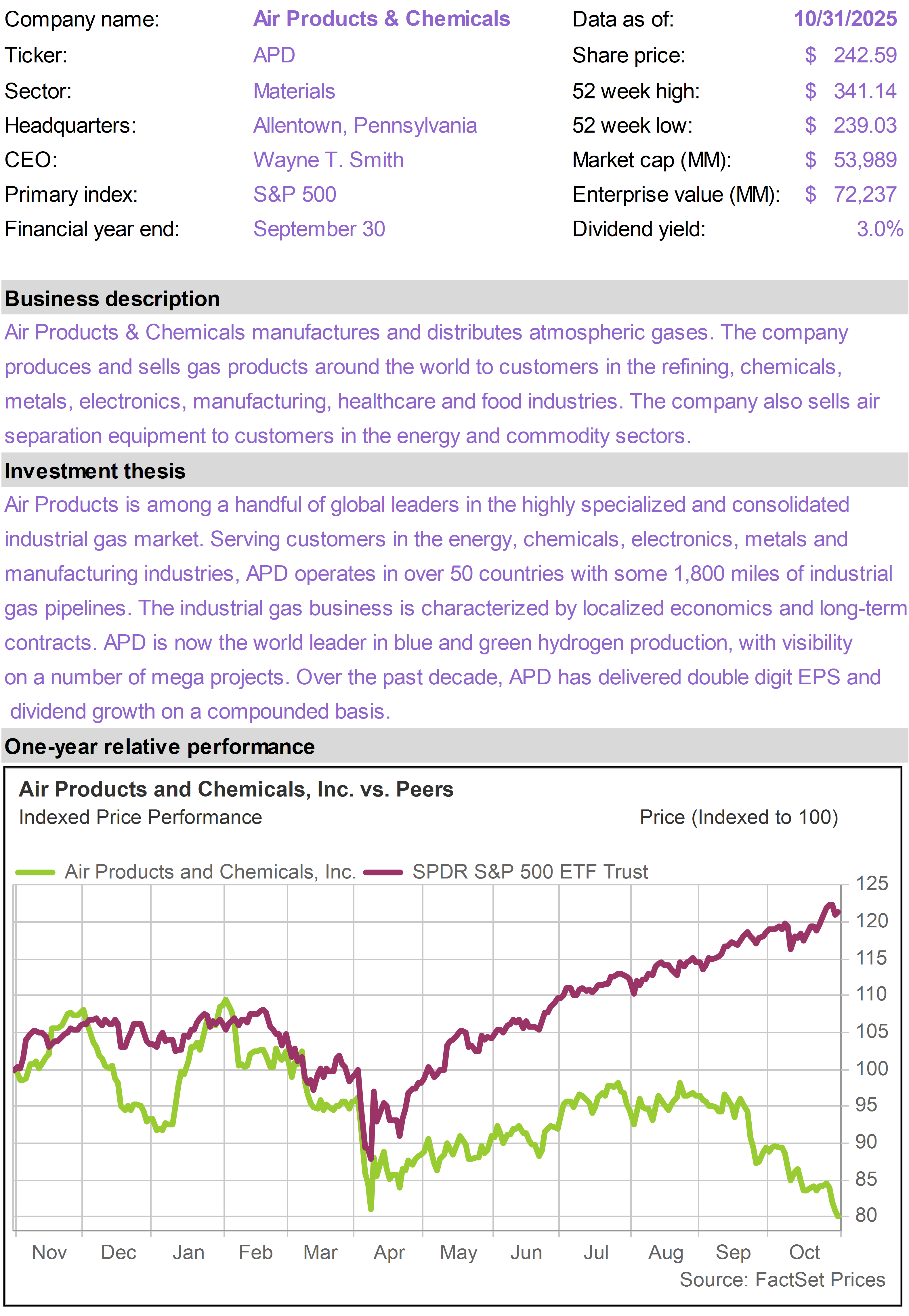

The worst performers in the portfolio this month were Texas Instruments (TXN), which returned -11%; Air Products & Chemicals (APD), which returned -10%; and Roper Technologies (ROP), which returned -10%.

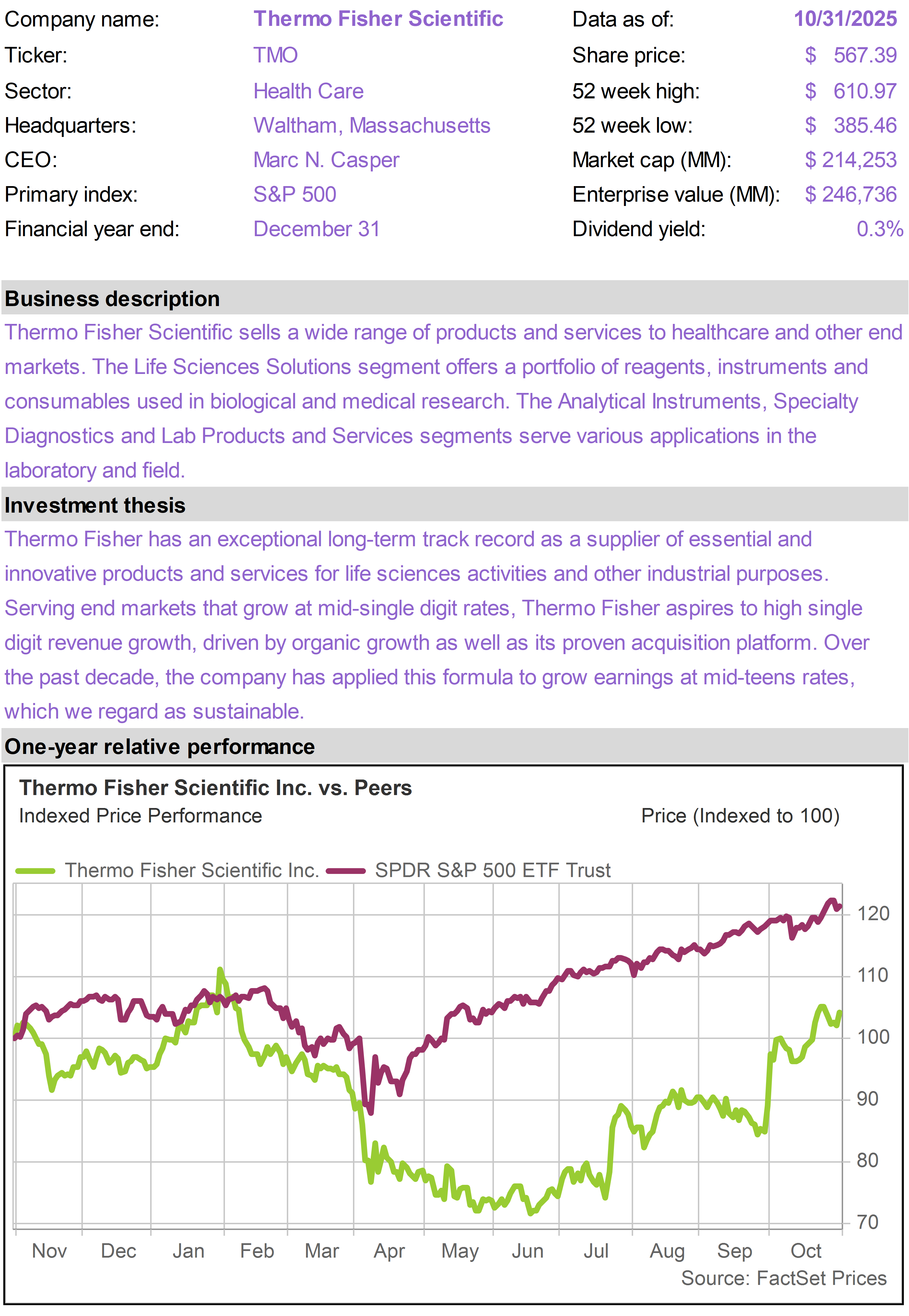

TMO is a good example of a high-quality stock, playing in an area that fell out of favor earlier in the year, that is now benefiting from a more reassuring outlook.

As a leading global provider of tools and equipment to the health care sector, TMO suffered from concerns around tariffs and reductions in health care spending.

In late October, the company reported strong third quarter earnings and provided reassuring commentary on end market strength, especially within academia and other areas of medical research.

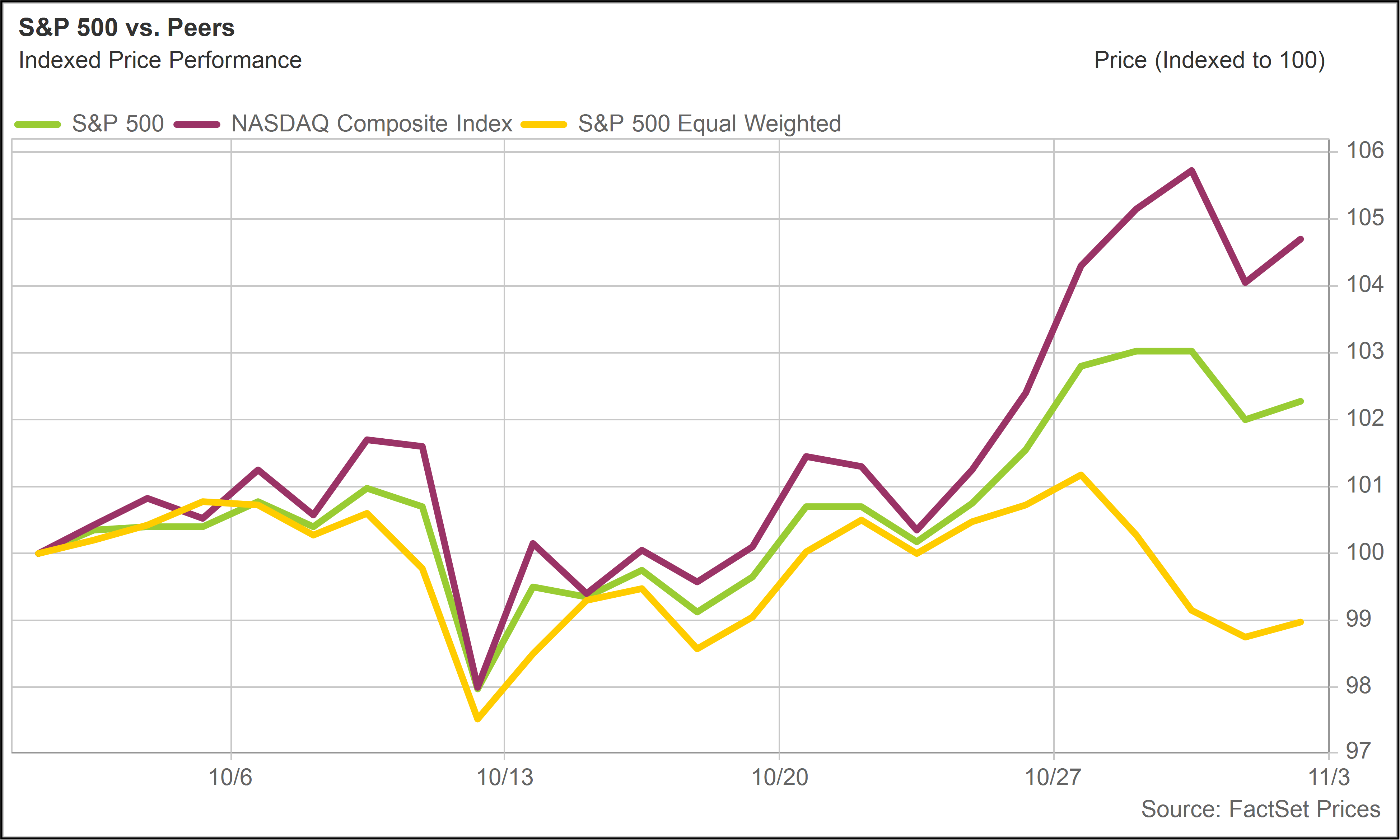

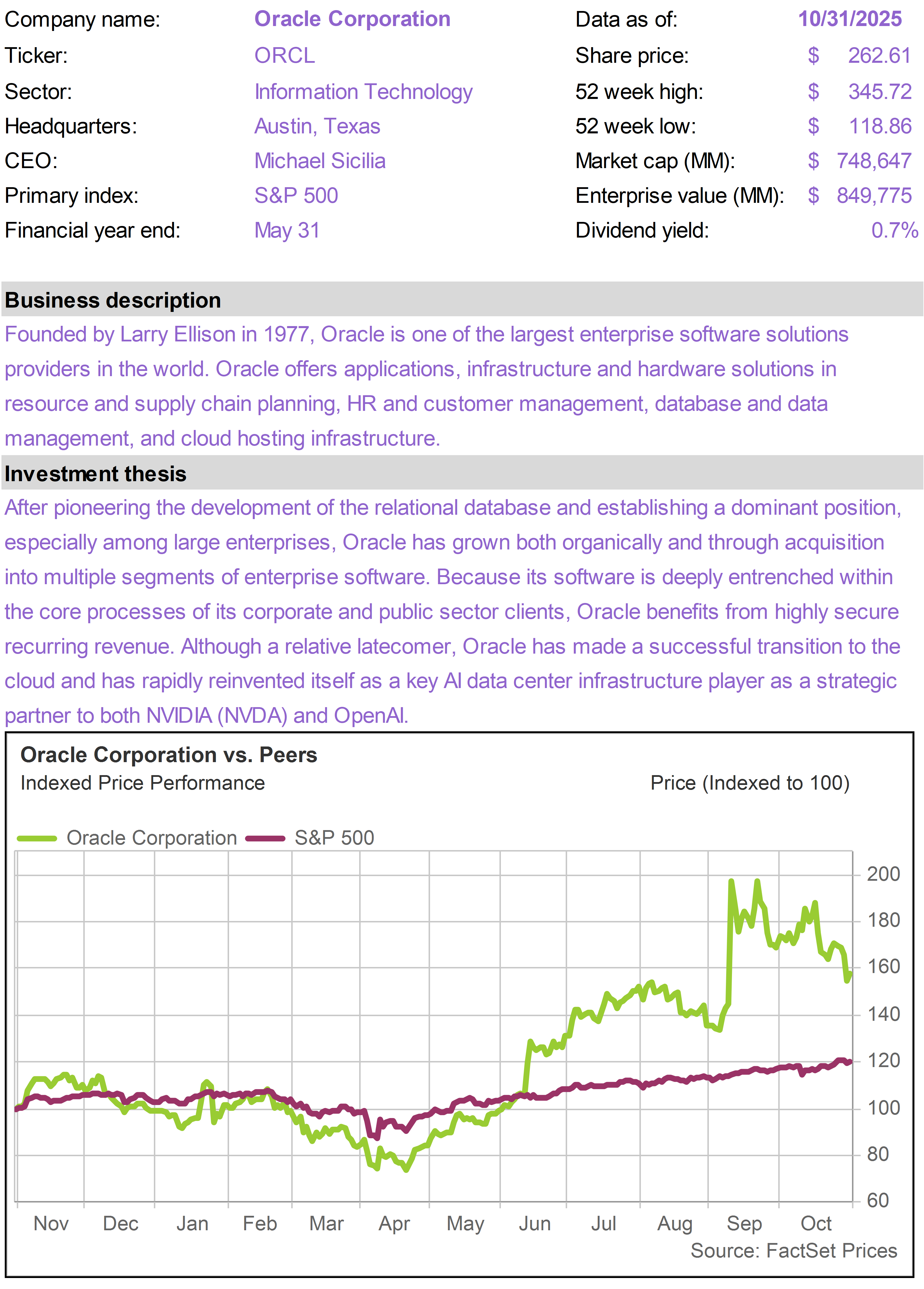

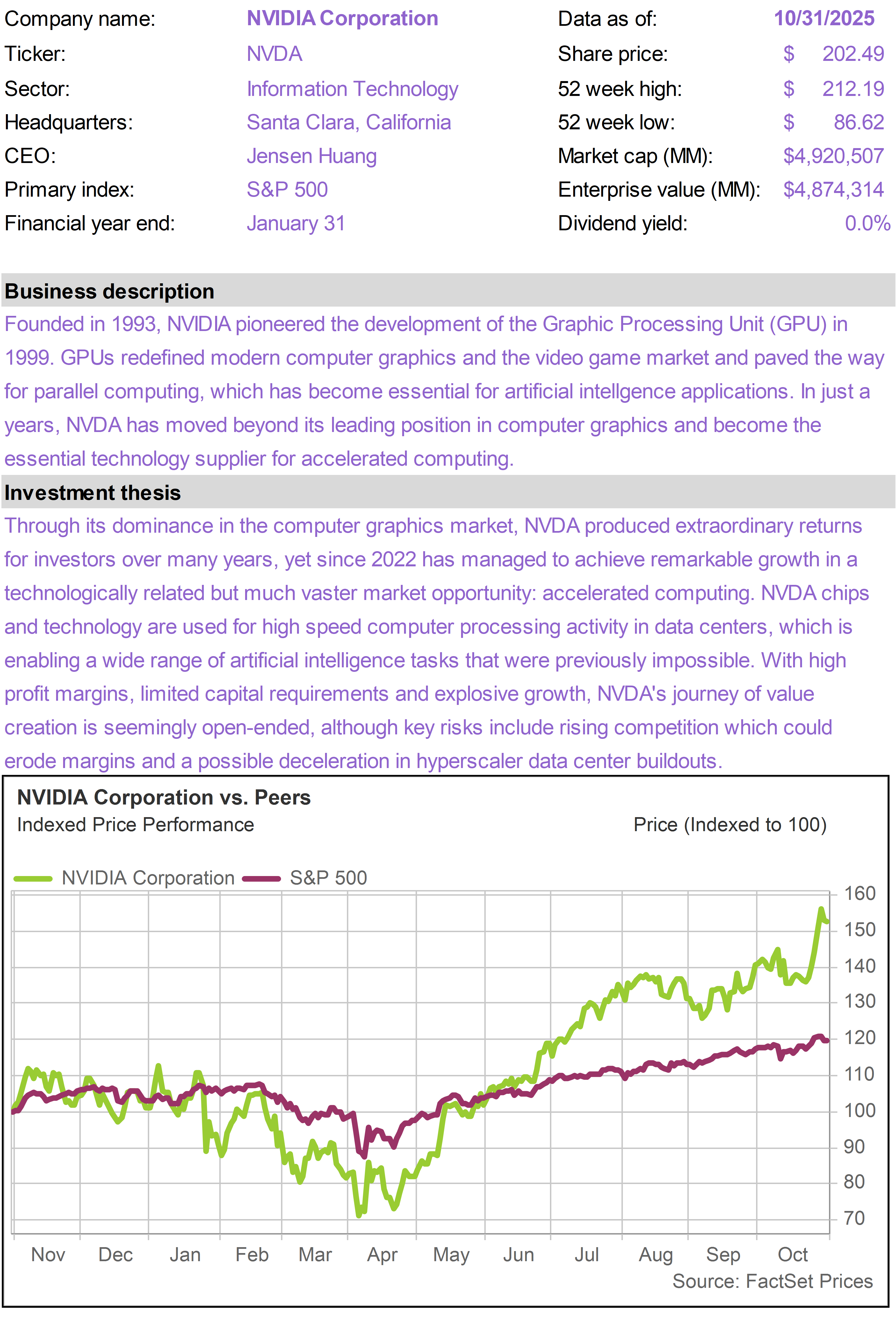

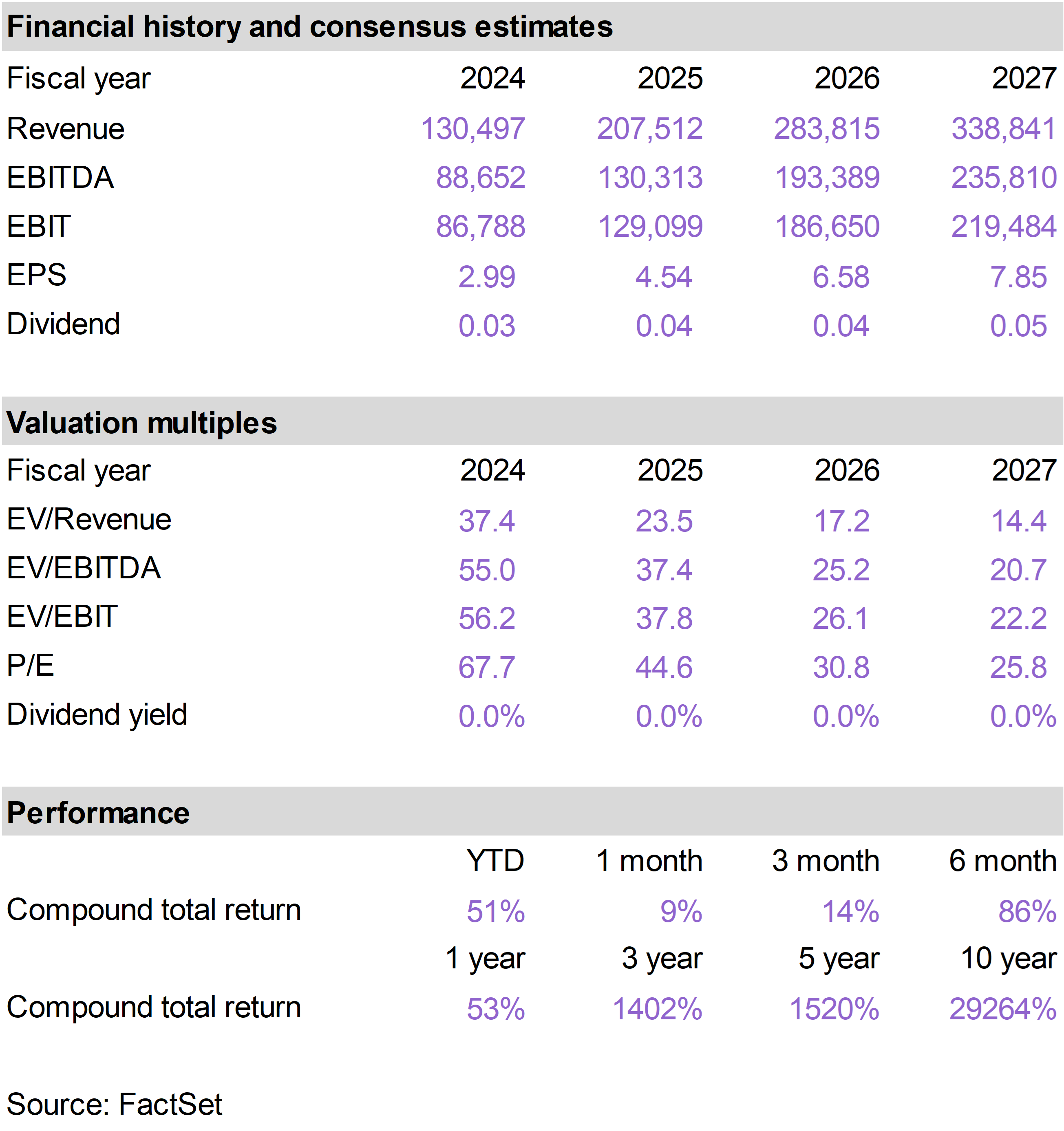

NVDA broke through $200 per share in October after CEO Jensen Huang provided the market with a series of important disclosures at the annual GPU Technology Conference (GTC) in Washington, D.C. on October 28. GTC is now the world’s premier AI developer conference, attracting more than 20,000 attendees, while millions watch online.

Jensen projected $500 billion in cumulative sales from the Blackwell platform and early Rubin ramps through 2026. Over the longer term, NVDA now sees $3 to $4 trillion of annual AI spend by 2030. These figures were significantly higher than consensus forecasts and lifted the stock.

NVDA also announced a number of exciting strategic moves, including a major collaboration with the Department of Energy to build what will become its largest AI supercomputer; a strategic partnership with Nokia, including a $1 billion investment to deliver next-generation 6G wireless networks; and several industrial partnerships with leading global manufacturers in robotics.

GXO designs and runs highly automated distribution centers, using robotics, conveyor systems, machine vision and AI-driven software. It is benefiting from an improved outlook towards the logistics space, which is now gaining momentum after a long digestion period following pandemic era capacity expansions.

A relatively small name for the portfolio, with a sub-$10 billion market cap, GXO is also now attracting interest from investors as it sits at the intersection between AI and e-commerce.

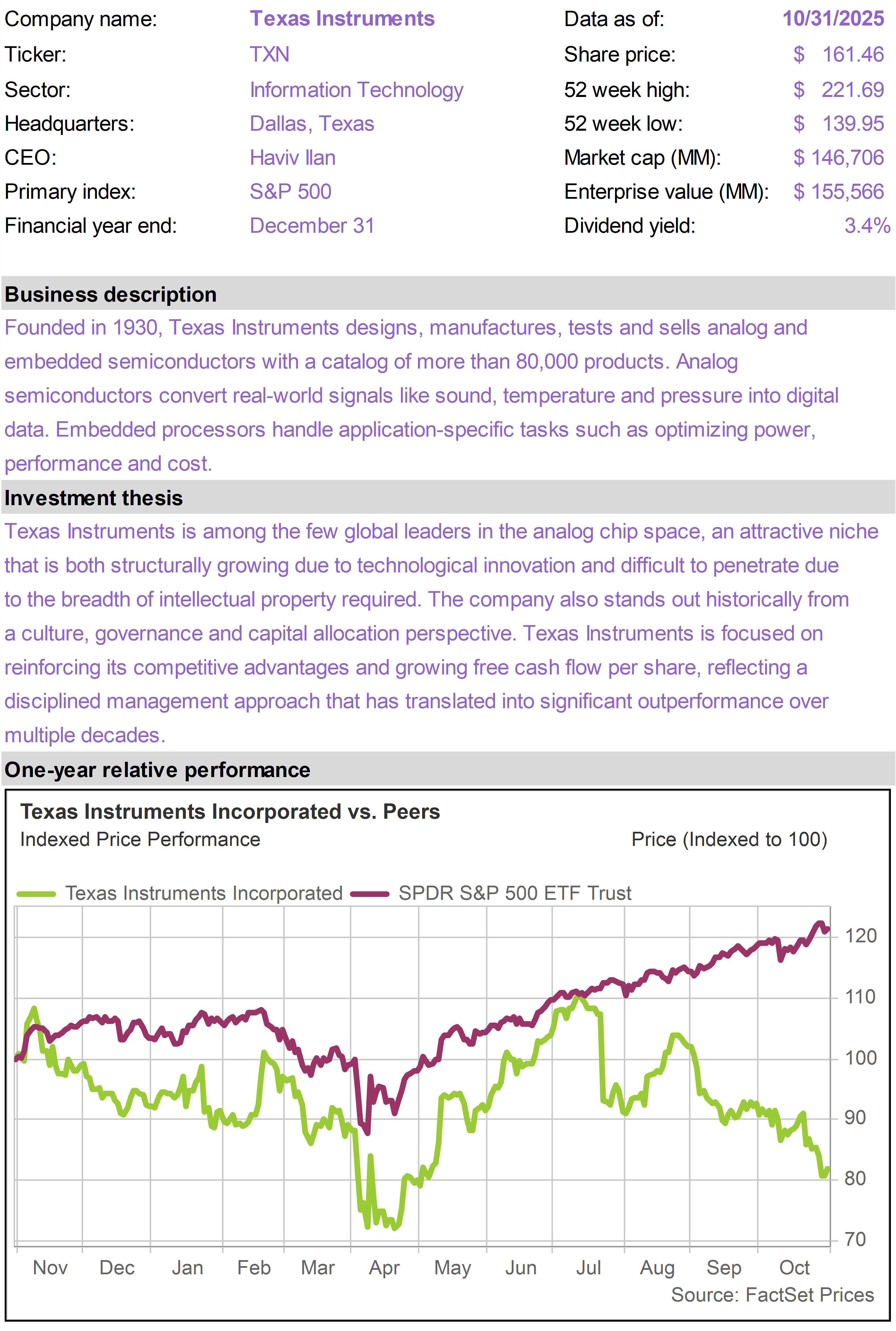

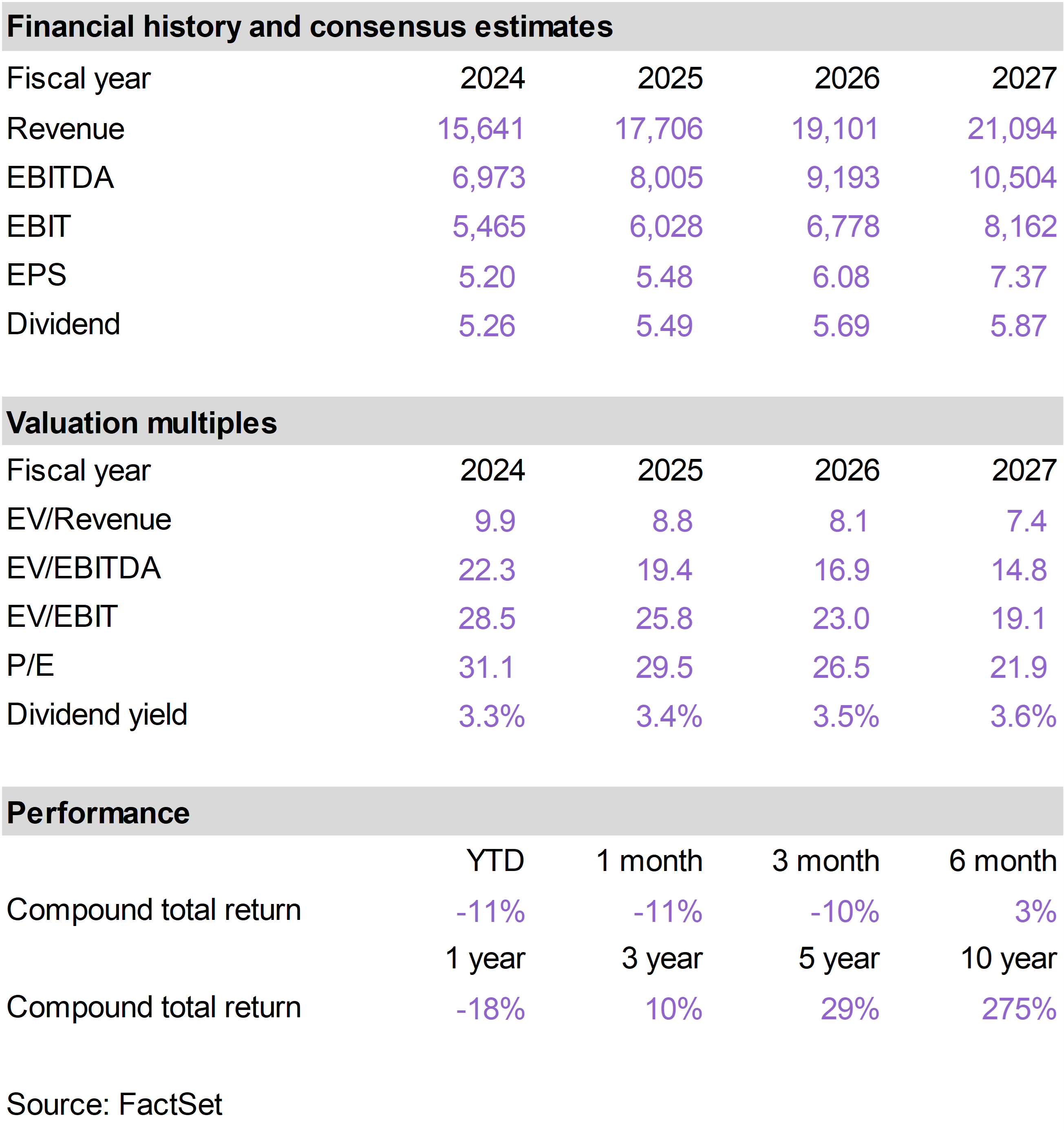

TXN shares declined following its third-quarter earnings report. While results largely met expectations, management guided to softer demand in the industrial end market for the upcoming quarter.

In a market where many technology companies are reporting accelerating growth tied to AI adoption, TXN’s slower cyclical recovery has tested investor patience. The near-term backdrop remains mixed, but the long-term strategic position is still highly attractive.

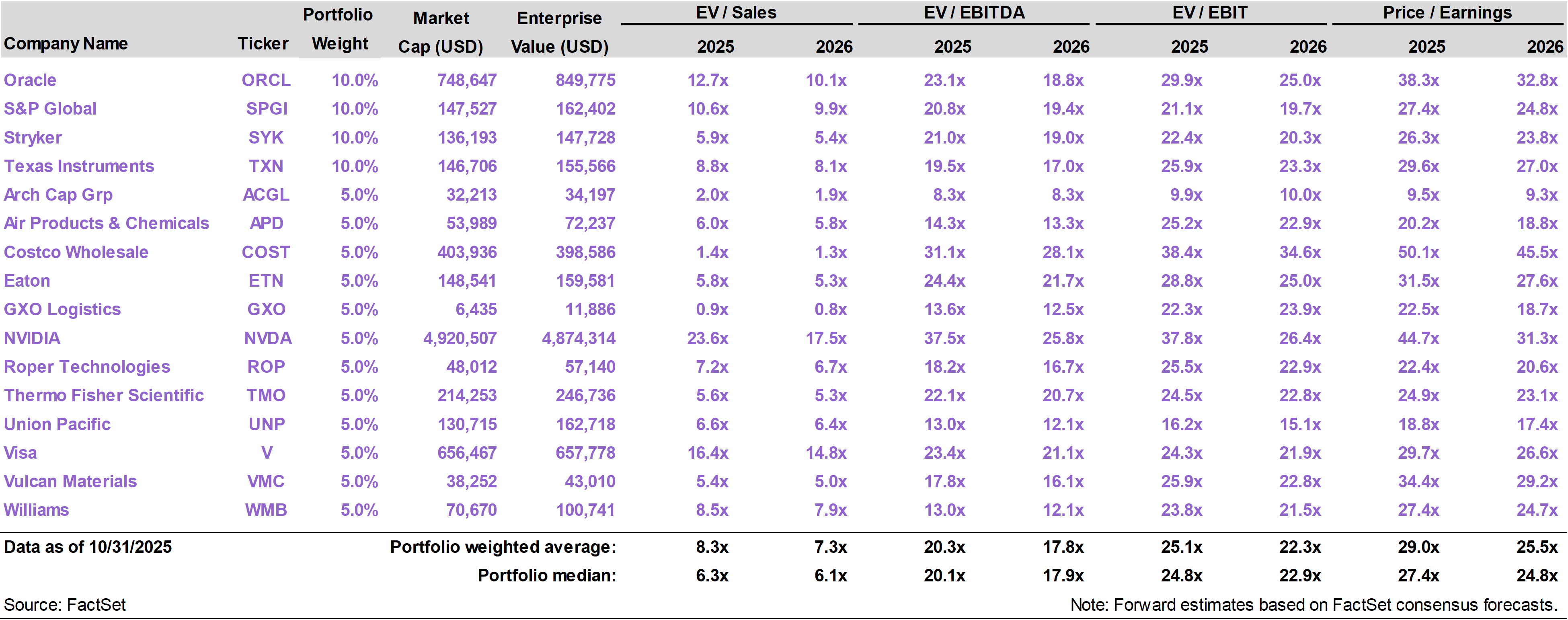

TXN is a market-leading supplier of analog and embedded processing chips that are essential for powering and controlling real-world systems. These are critical to data centers, robotics, factory automation, electric vehicles, and autonomous driving—all of which are long-duration AI-driven growth trends.

TXN has the world’s most advanced and efficient analog chip fabs located within U.S. borders. This positions it to be the low-cost, high-reliability supplier of choice to manufacturers in these growth areas.

As the industrial cycle stabilizes, TXN remains well-placed to expand margins and move closer to its long-term free cash flow targets. For investors seeking long-term exposure to AI without paying premium valuations, TXN offers a compelling setup at current levels.

As the company’s major fab expansion cycle winds down, capital expenditures are poised to decline meaningfully. At the same time, revenues are expected to grow steadily as industrial and auto demand stabilize. Together, these dynamics support analyst forecasts that call for free cash flow to nearly triple over the next two years.

Looking further ahead, AI-intensive markets—data centers, robotics, factory automation, EVs, and autonomous systems—will represent an increasingly large share of TXN’s business mix. As this transition unfolds, TXN’s long-term growth profile should improve, with structurally higher margins and more durable long-term demand.

APD did not report results in October but drifted lower as investors pulled capital from cyclical industrial names. APD will report in November, at which point we will gain better insight into current business trends.

ROP delivered solid third quarter results, with 14% total revenue growth and strong free cash flow margins. However, in a market environment with little tolerance for below expectation growth, ROP was penalized for a slight reduction in its organic growth guidance.

This reduction was driven by temporary, timing-related factors linked to the government shutdown and copper tariffs, which affected certain customers—neither of which reflects weakening underlying demand.

The company’s diversified portfolio of mission-critical vertical software businesses continues to generate high recurring revenue and attractive margin expansion. Management also announced a $3 billion share repurchase authorization, which adds another lever for value creation alongside its consistent M&A strategy.

ROP is also beginning to see tangible benefits from AI-enabled product innovation across its portfolio. As these solutions scale and shutdown-related delays roll off, organic growth is positioned to re-accelerate in 2026, supporting management’s goal of compounding free cash flow per share at mid-teens rates.