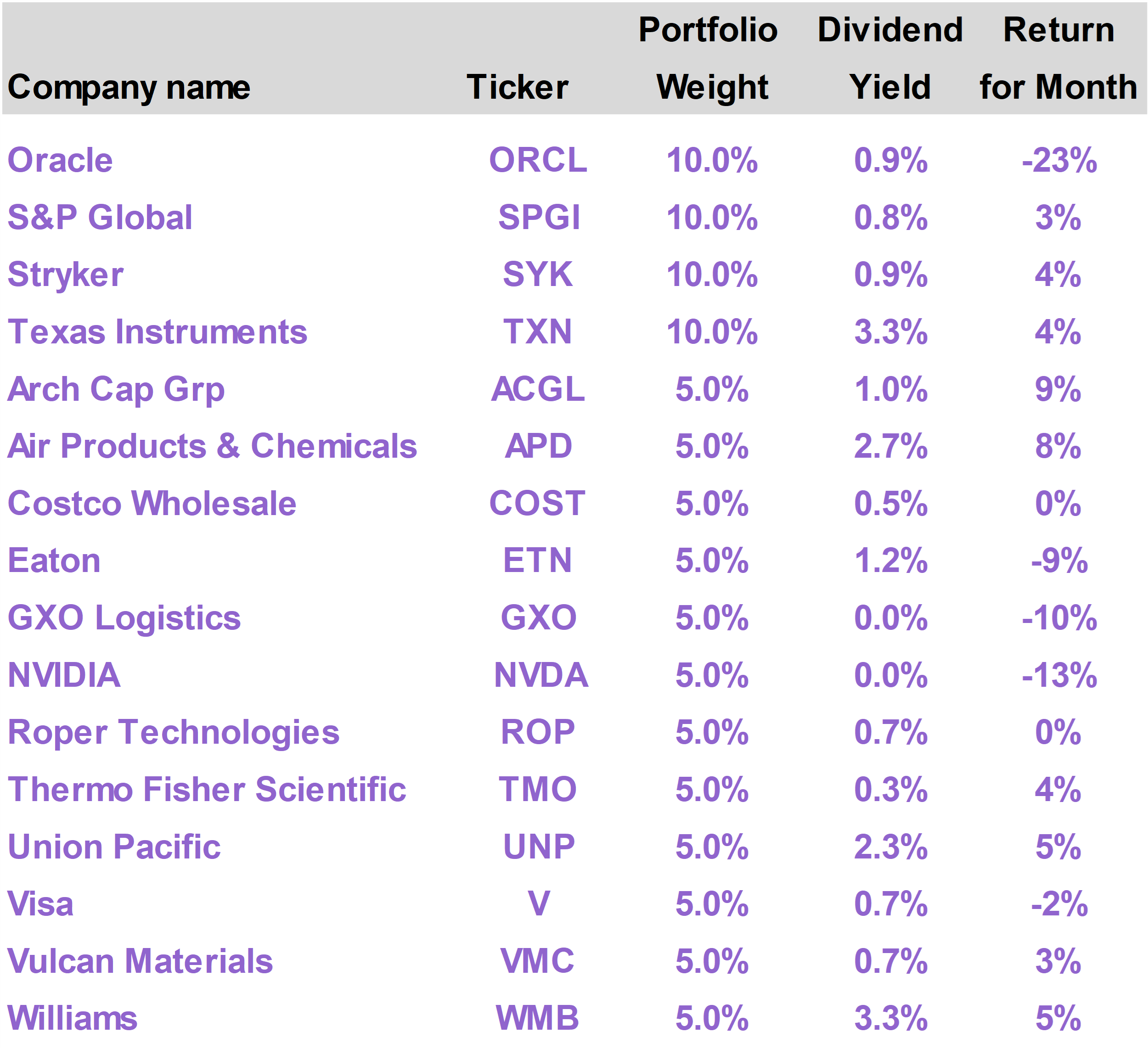

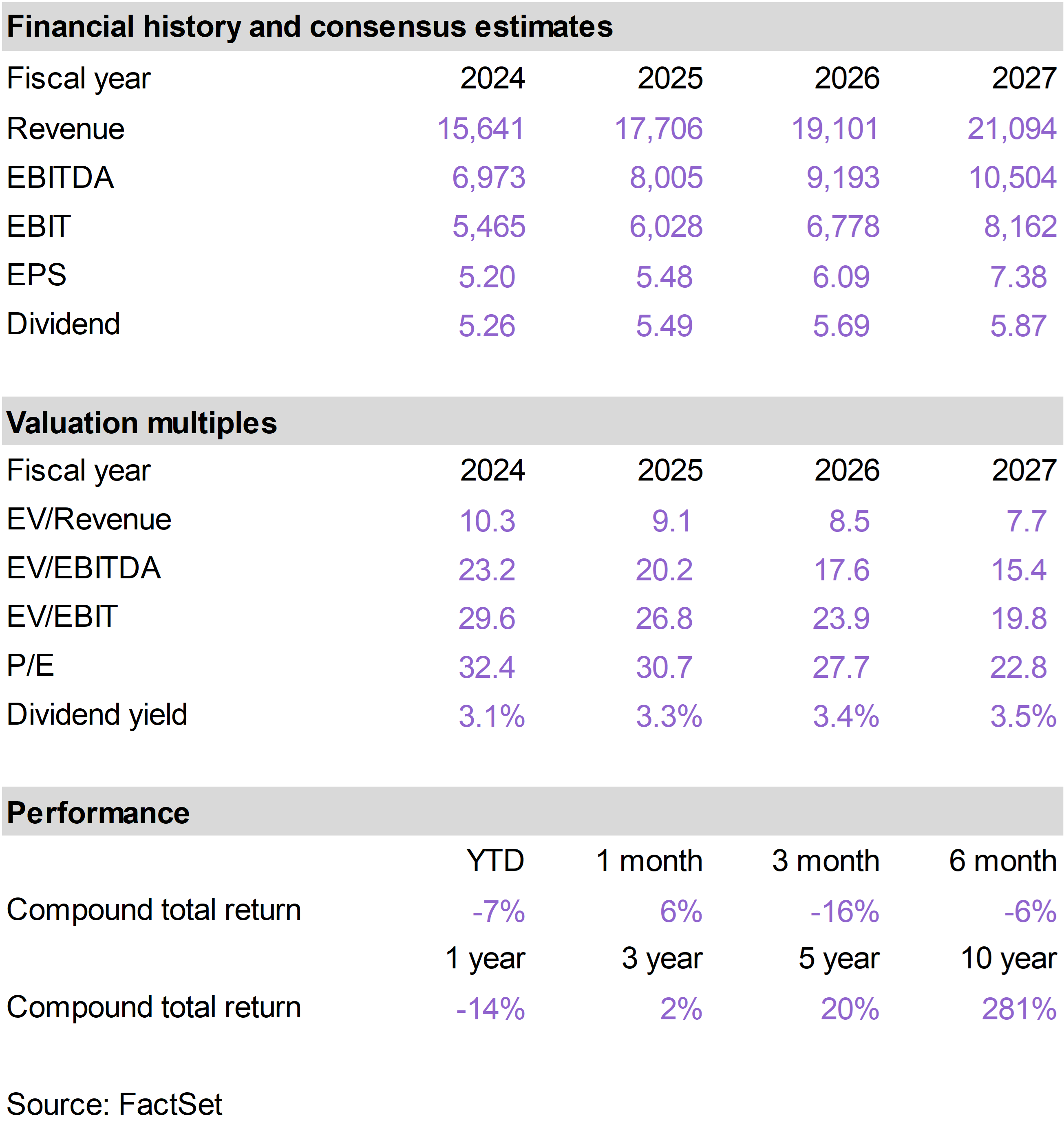

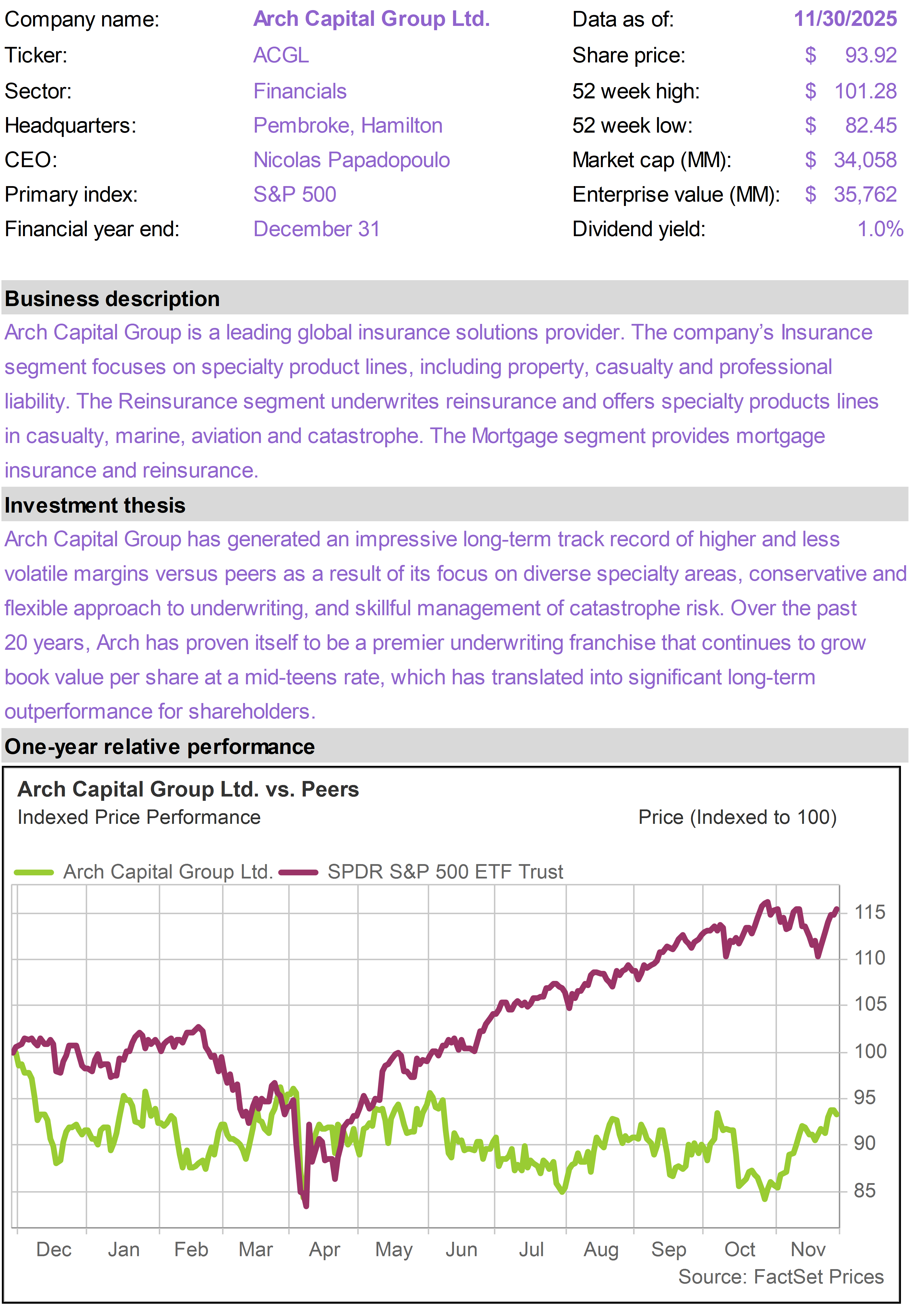

ACGL shares gained momentum after a solid late October earnings beat and well-received conference call. The insurer is benefiting from strong underwriting conditions, with loss ratios trending favorably across its property and casualty and mortgage lines.

Reinsurance pricing remained firm entering year-end, creating further confidence in ACGL’s ability to generate mid-teens returns on equity. This consistent execution has made ACGL one of the most reliable long-term performers in the insurance sector.

ACGL likely also benefited from sector rotation. From a valuation perspective (price to book and price to earnings), the stock’s valuation is now modest by historical standards.

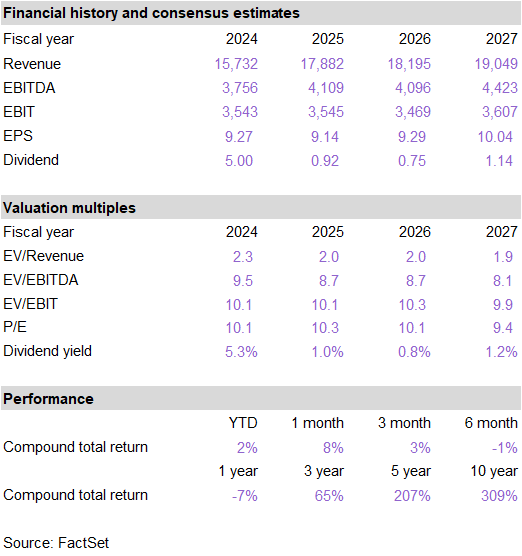

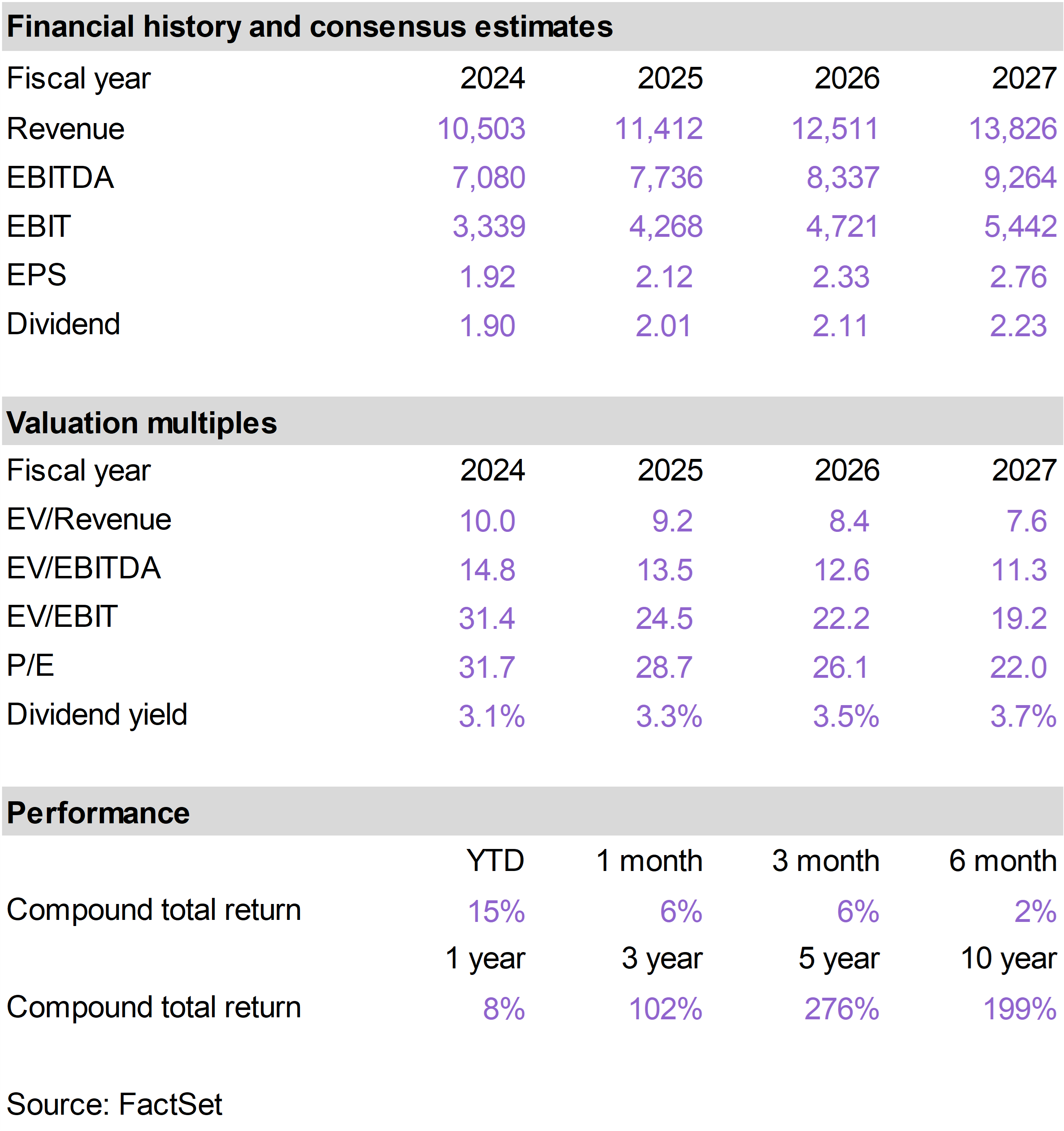

APD continued to rebuild investor confidence under its new CEO. In November, APD delivered its second consecutive earnings beat and guided 2026 earnings growth to 7–9%, slightly above consensus, helped by better pricing, improving cost discipline, and progress on exiting underperforming projects.

Margins improved during the quarter, and APD reiterated its focus on traditional industrial gas projects where returns are more predictable. With clearer execution, a more achievable capital spending plan, and signs that earnings growth is stabilizing, investors gained confidence in the company’s ability to deliver on its multi-year growth outlook.

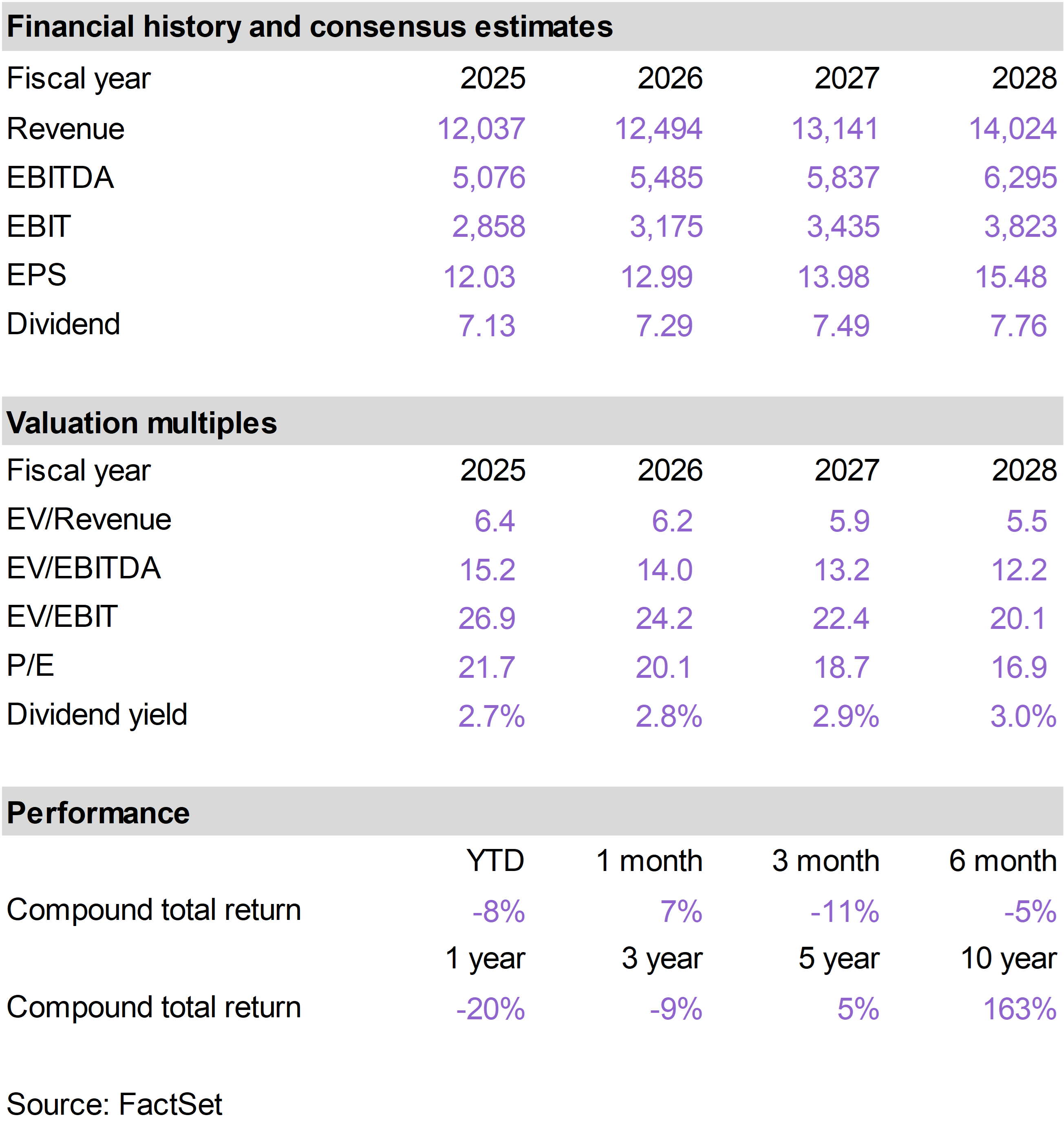

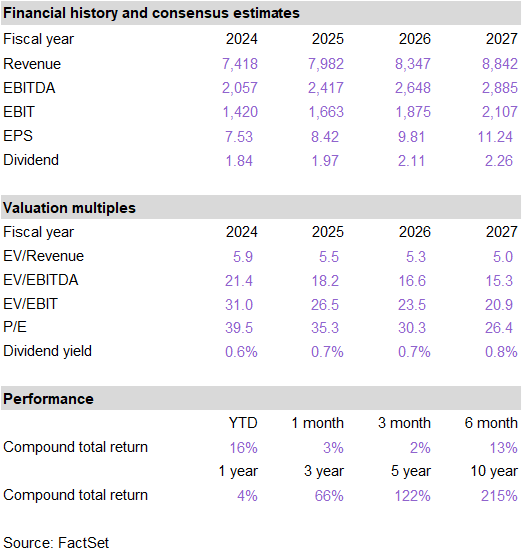

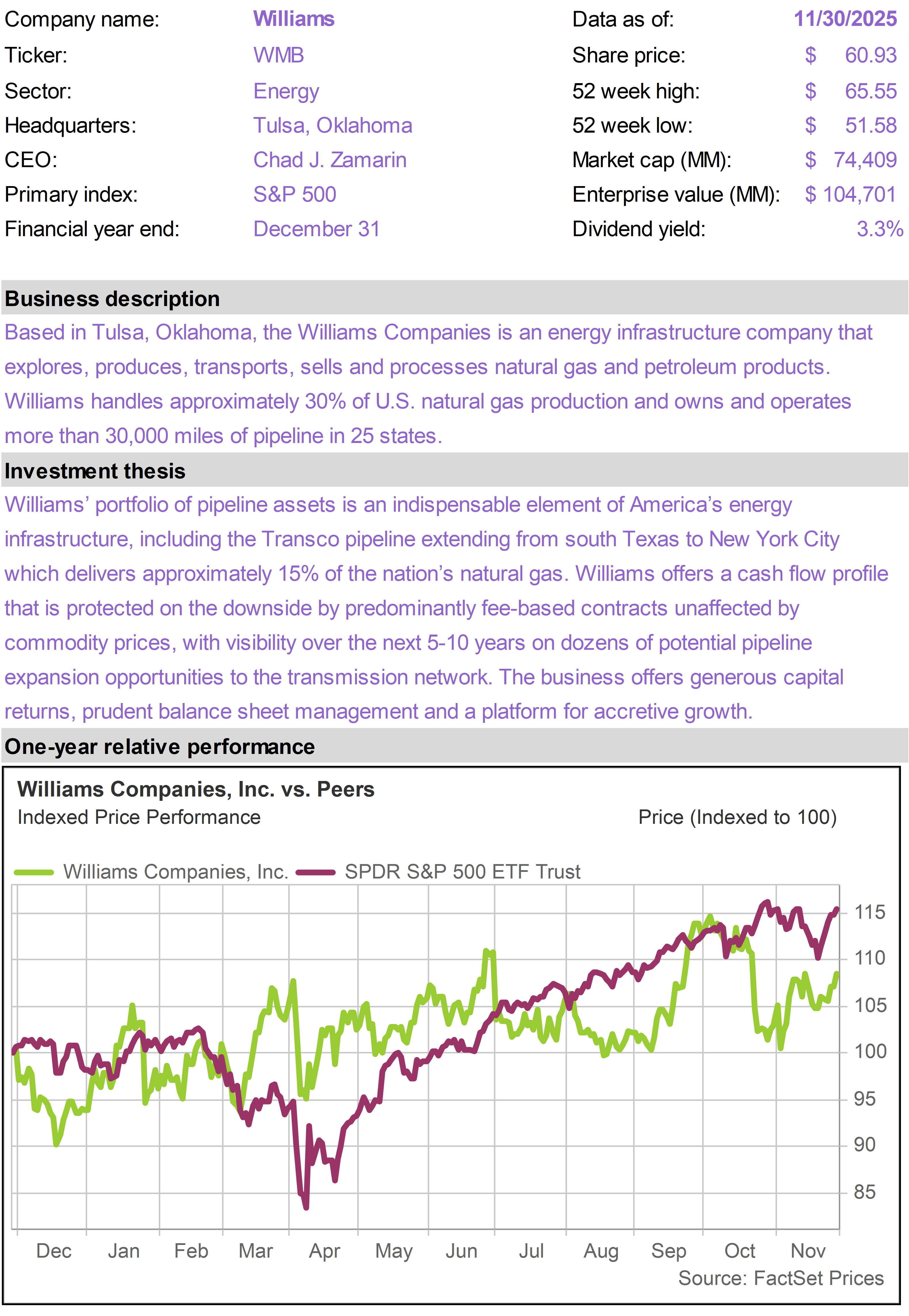

WMB reaffirmed its 2025 EBITDA guidance and delivered steady, fee-based third quarter results. Several new pipeline and storage projects were announced, adding to the company’s long-term growth pipeline.

In February, WMB will host its Analyst Day, which could serve as a meaningful catalyst for the stock, with a potential upward revision to its long-term EBITDA growth outlook. WMB has guided investors toward 5-7% long-term growth but has averaged 9% over the past five years.

As the largest natural gas pipeline operator, WMB is a major beneficiary of AI data center demand for electrical power, given that natural gas is the most important fuel for power generation in the U.S.

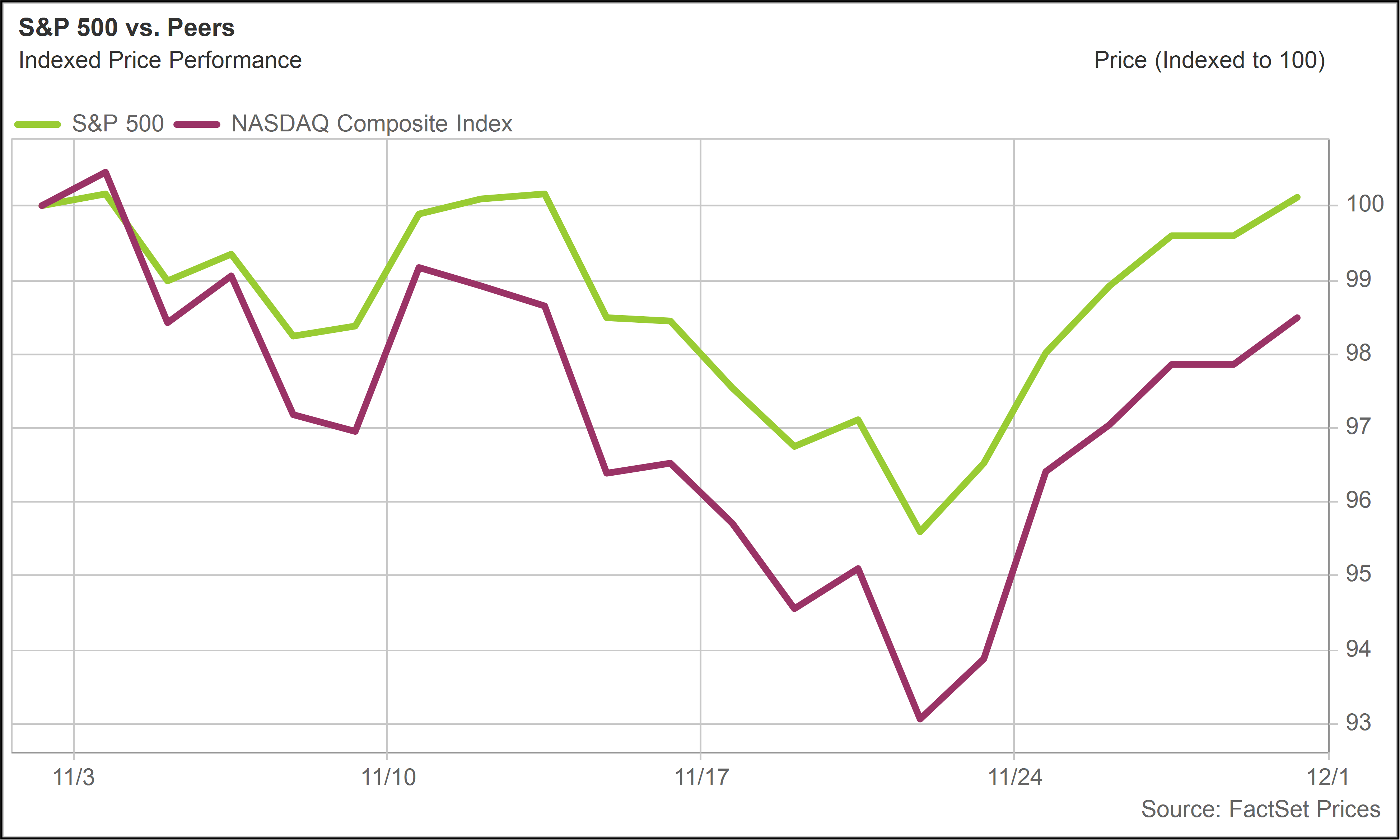

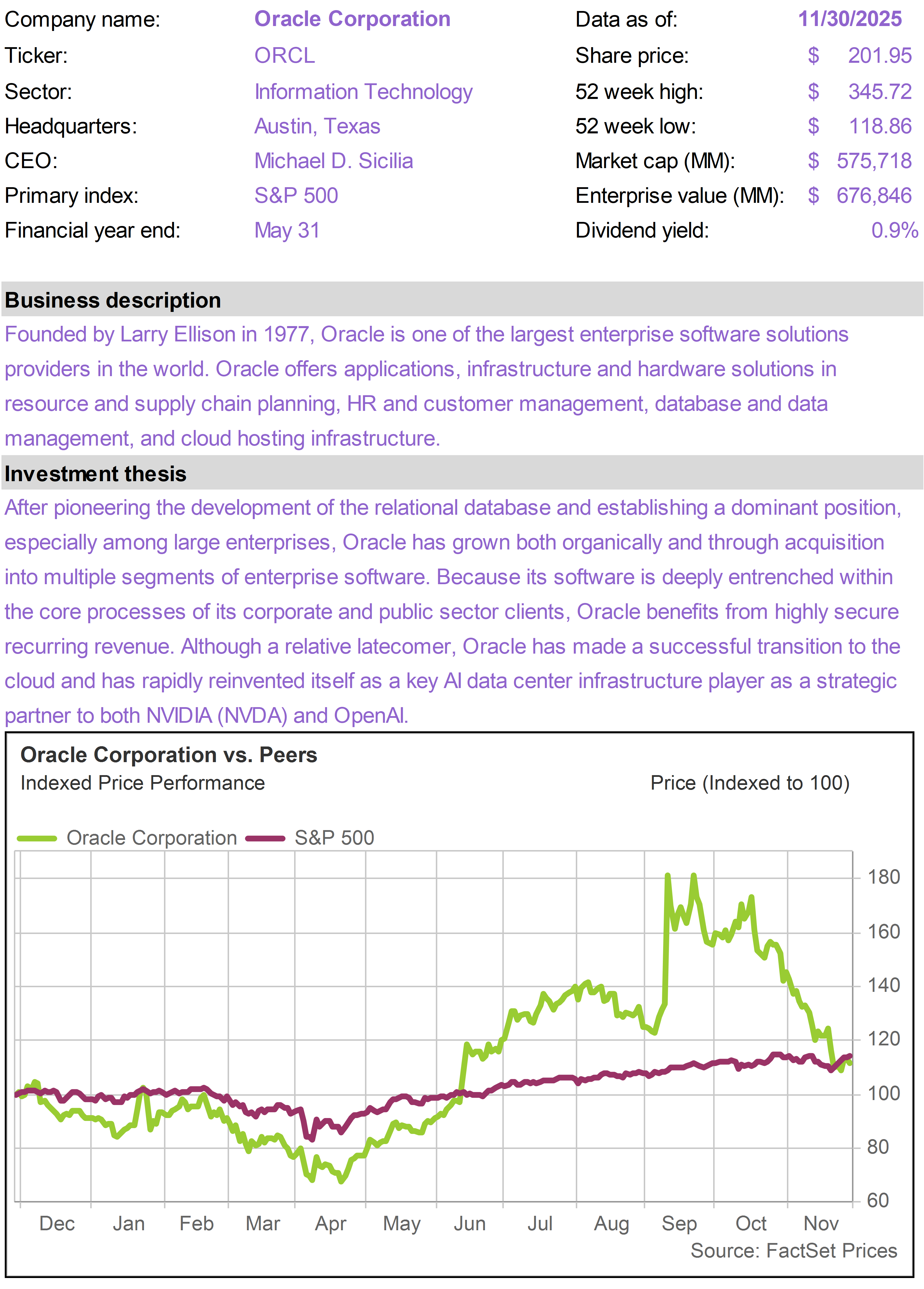

ORCL has been at the center of the AI mood shift. After soaring in recent months following disclosure of bulging order backlogs, largely driven by OpenAI, shares have declined sharply.

Investors have become concerned about the ability of OpenAI to fund its ambitious growth plans, and they are concerned about the debt ORCL needs to incur to fund its own capital spending plans.

We view the current weakness in ORCL as a compelling opportunity. Concerns about OpenAI are valid, but it is not ORCL’s only customer or long-term potential customer.

The rapid reversal in the share price overstates the risk and valuation impact. Consensus estimates still forecast ORCL earnings per share more than tripling over the next five years.

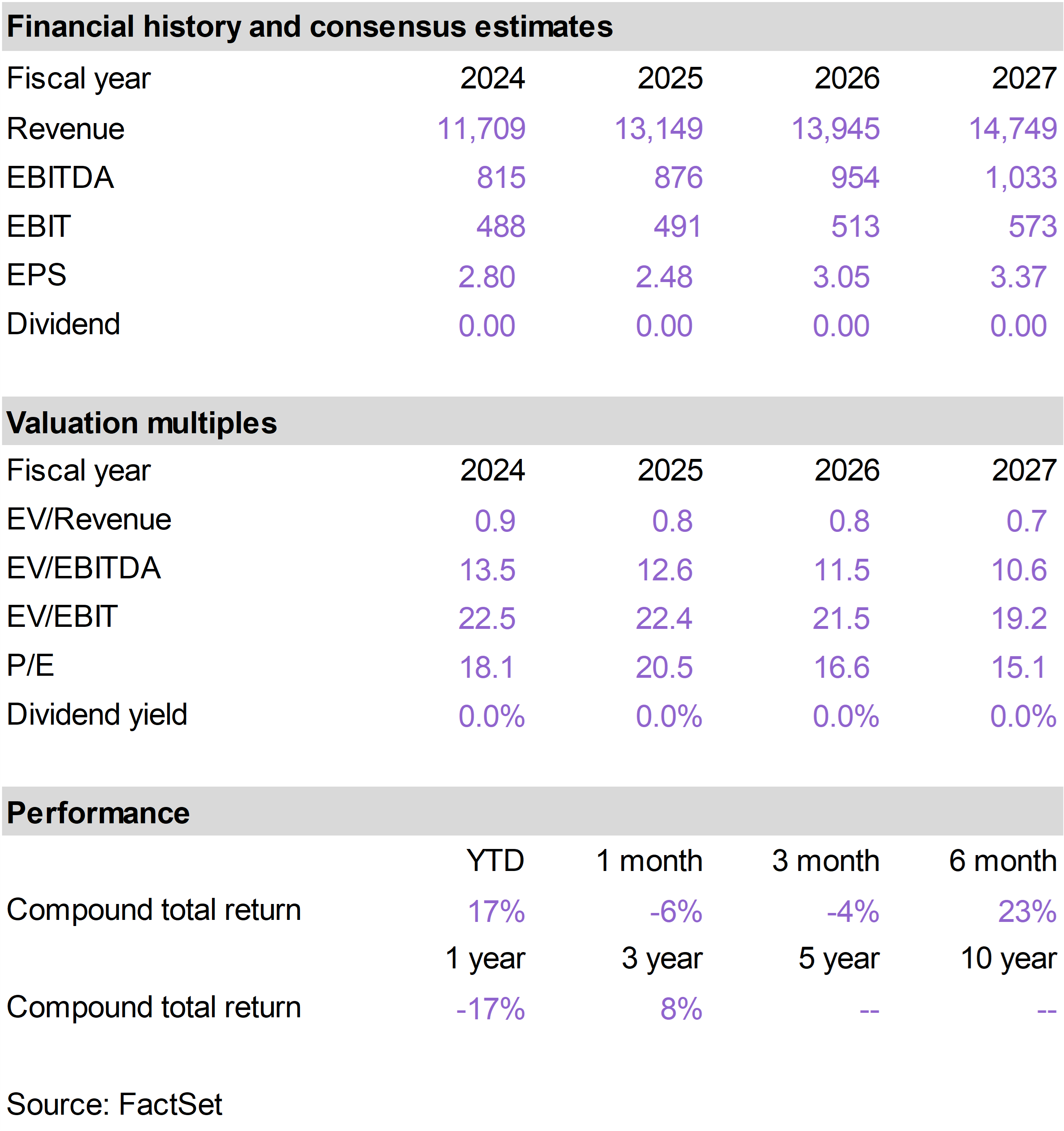

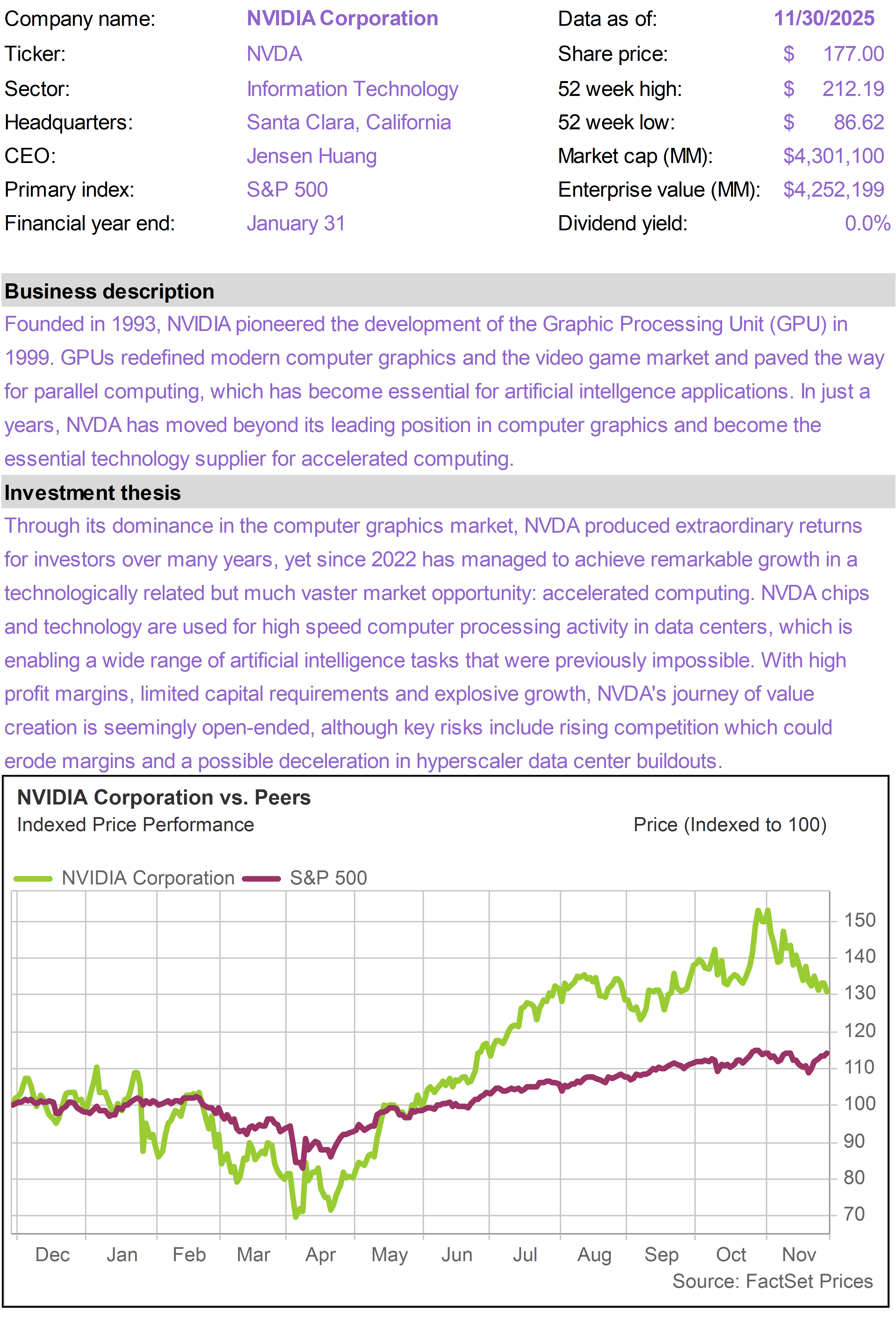

Weakness in NVDA in November is linked to the negative sentiment toward ORCL.

OpenAI’s funding uncertainty raised concerns about the stability of near-term demand, since ORCL is now one of NVDA’s largest hyperscale customers. At the same time, Alphabet (GOOGL) delivered strong results from its Gemini AI model, which added to the narrative that Google may continue leaning into its own internal AI hardware.

Google is increasingly training and running Gemini on its specialized Tensor Processing Units (TPUs), whereas Graphic Processing Units (GPUs)—where NVDA dominates—are more general-purpose hardware.

These headlines overshadowed what were, in reality, excellent earnings from NVDA: data center revenue surged, gross margins expanded, and demand remained exceptionally strong across every major cloud provider.

Progress in TPU development does not necessarily threaten NVDA; in many cases, it can accelerate it. Faster model development at Google raises competitive pressure on other hyperscalers—most of whom rely heavily on NVDA—and expands the total compute footprint required to train, deploy, and fine-tune next-generation models.

While TPUs may play an important role as AI evolves, we are not alarmed. GPUs remain the industry’s foundational compute layer—supported by the unmatched breadth of NVDA’s CUDA software ecosystem, the flexibility to run every major AI model, and a roadmap that continues to define state-of-the-art performance.

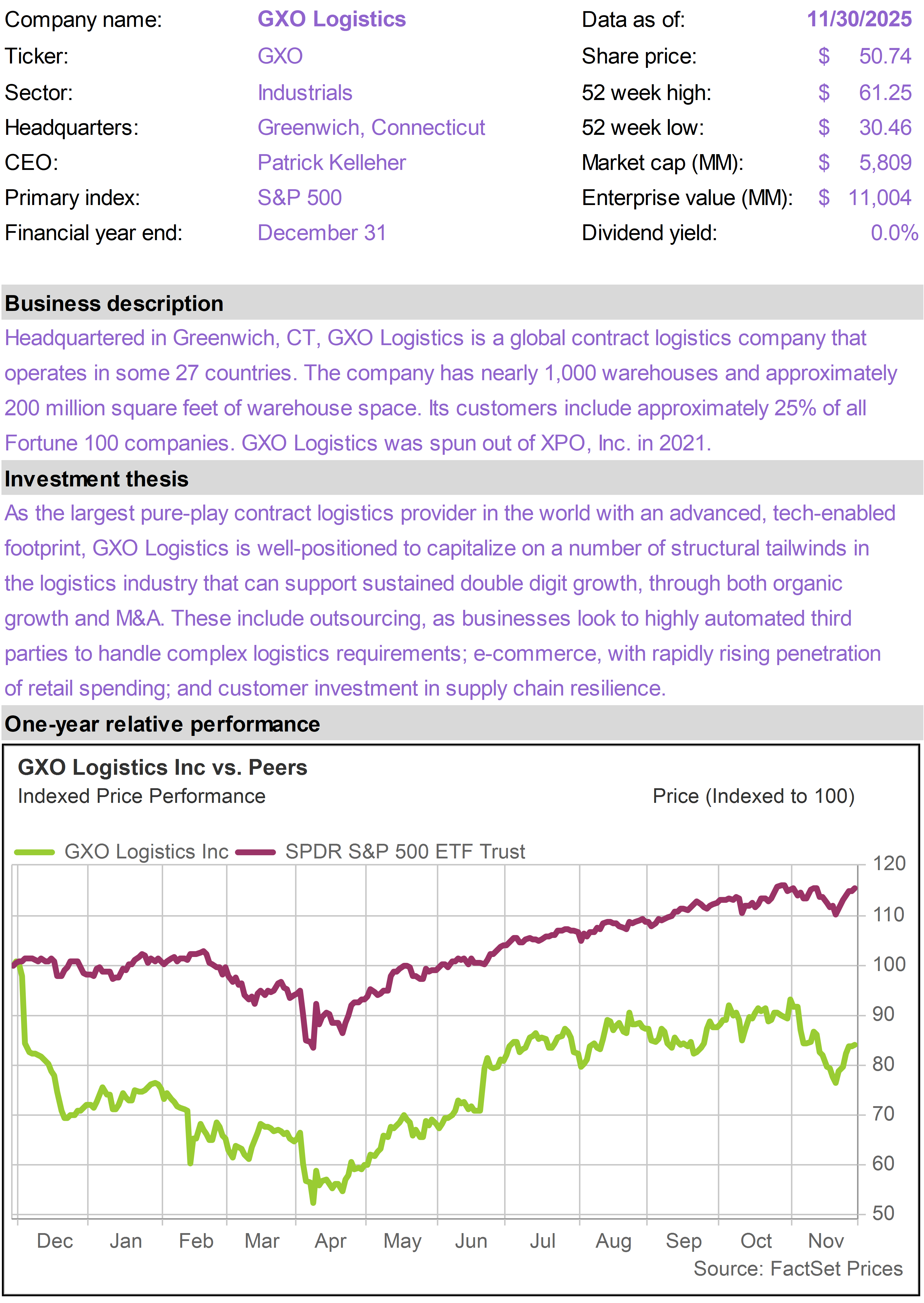

GXO, a provider of advanced outsourced logistics services, underperformed as several retailers and industrial customers signaled more cautious inventory management heading into year-end. Investors also grew concerned that macro uncertainty could delay new outsourcing decisions.

With structurally rising demand for logistics efficiency, robotics, and supply chain resilience, we believe GXO remains well-positioned once cyclical pressures ease.