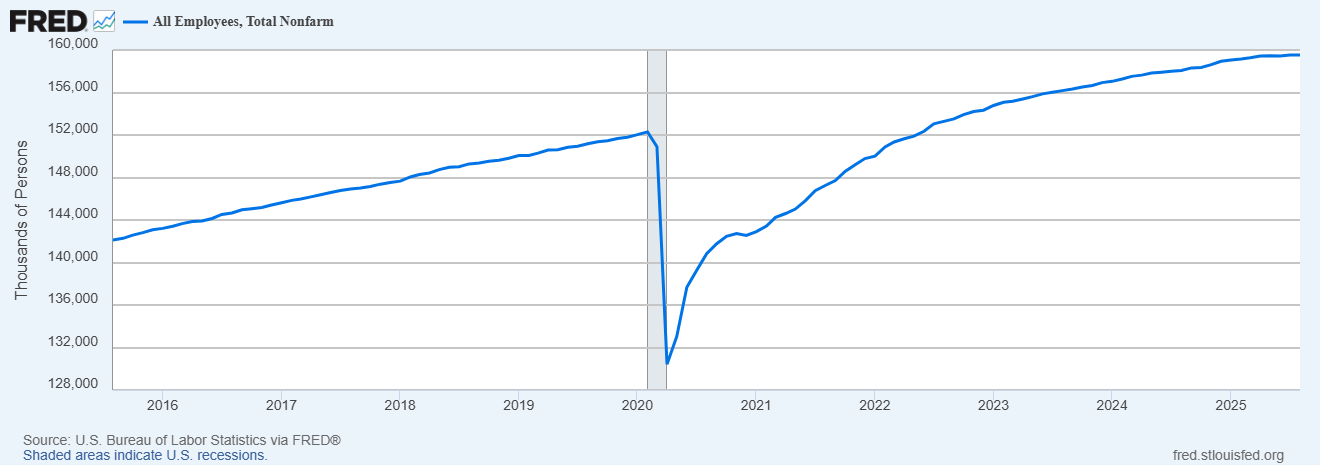

The economy is now arguably back to full employment levels. With monetary policy still restrictive and ongoing reductions in government headcount (potentially exacerbated by the recent shutdown), hiring has slowed considerably.

The most recent ADP payroll report showed a net decline in private sector jobs of 32,000 last month.

So while stocks are benefiting from anticipated rate cuts and easier monetary policy, there is some concern about the overall health of the economy, with unemployment rates expected to tick up.

From a stock market standpoint, one positive offset to the negative demand impact of rising unemployment and lower consumer confidence is that it puts less upward pressure on wages. Rising unemployment is bad for sales but helpful for operating expenses.

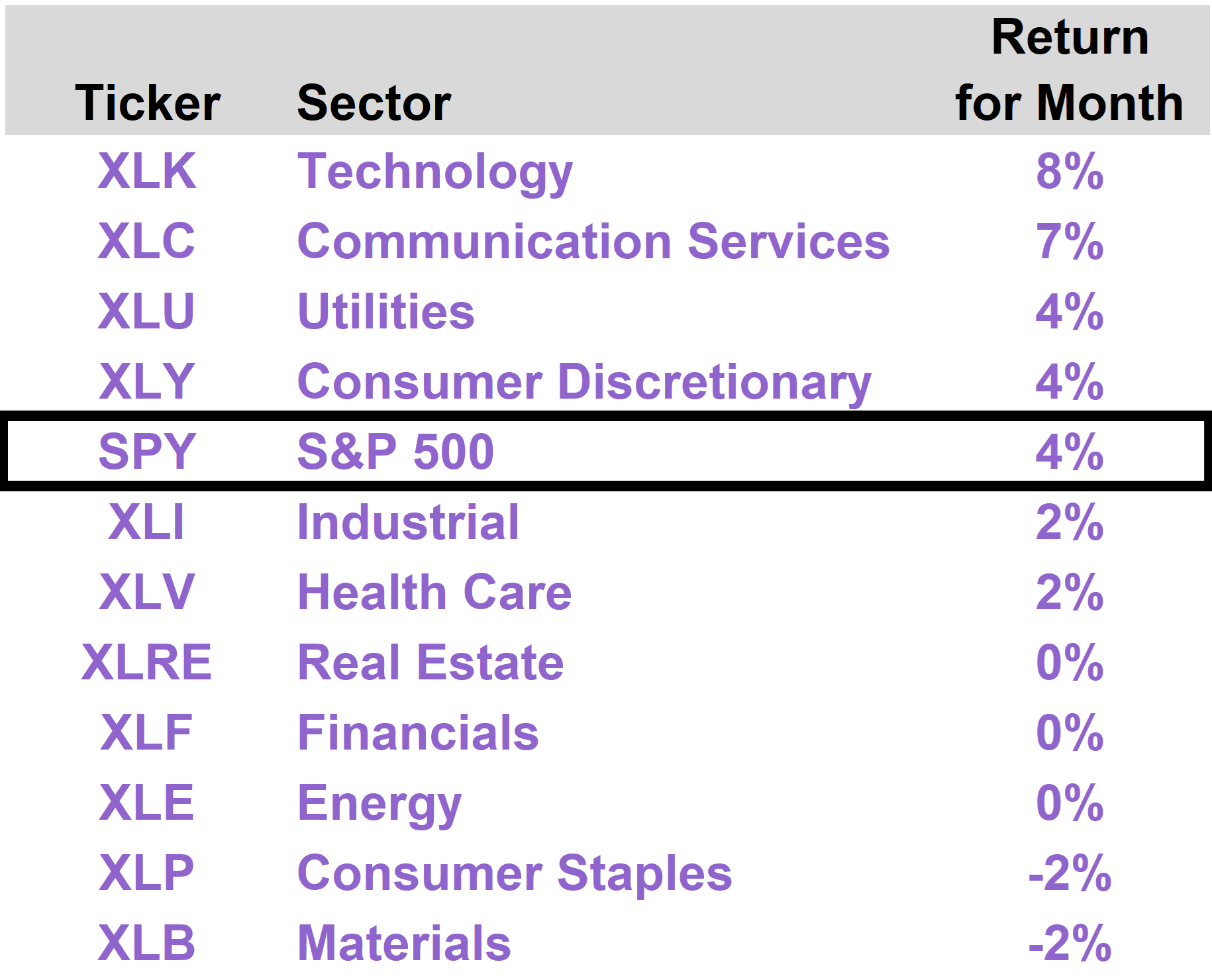

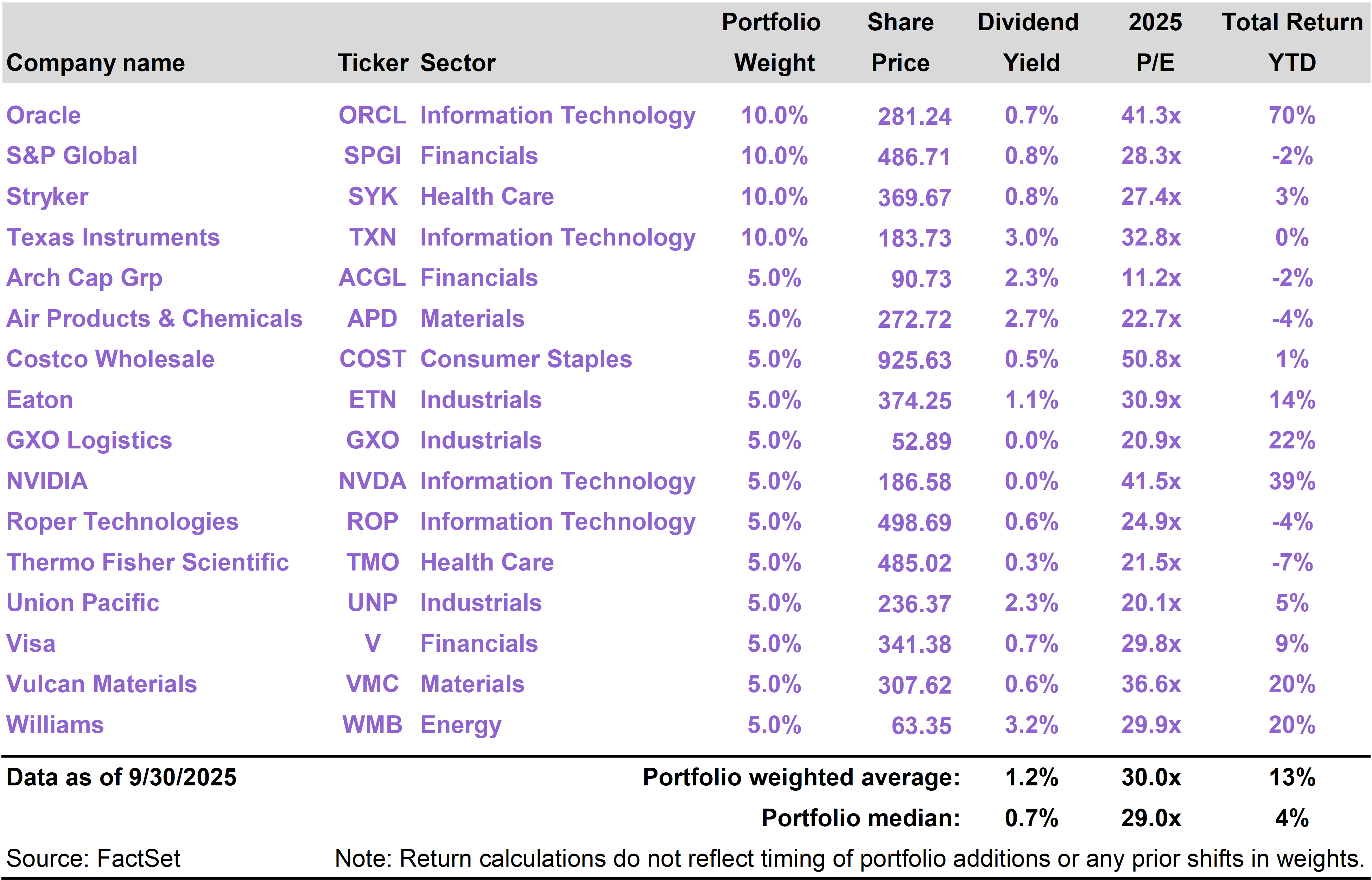

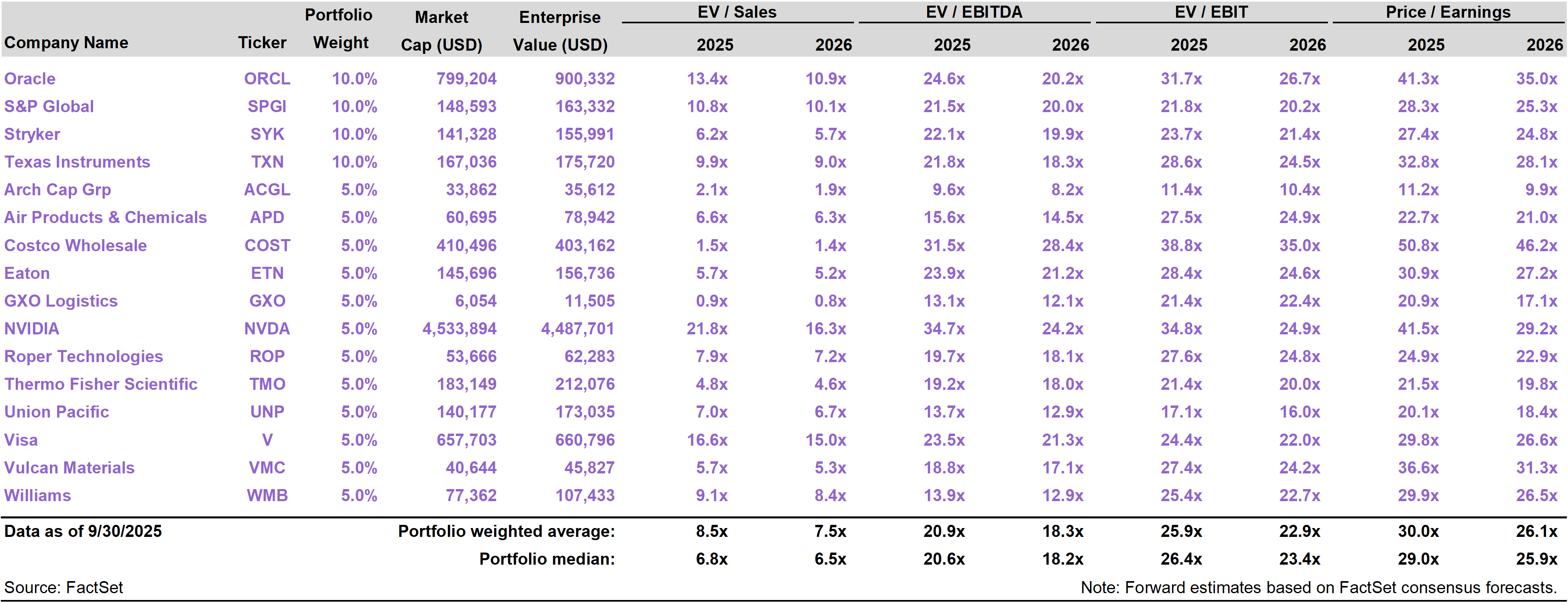

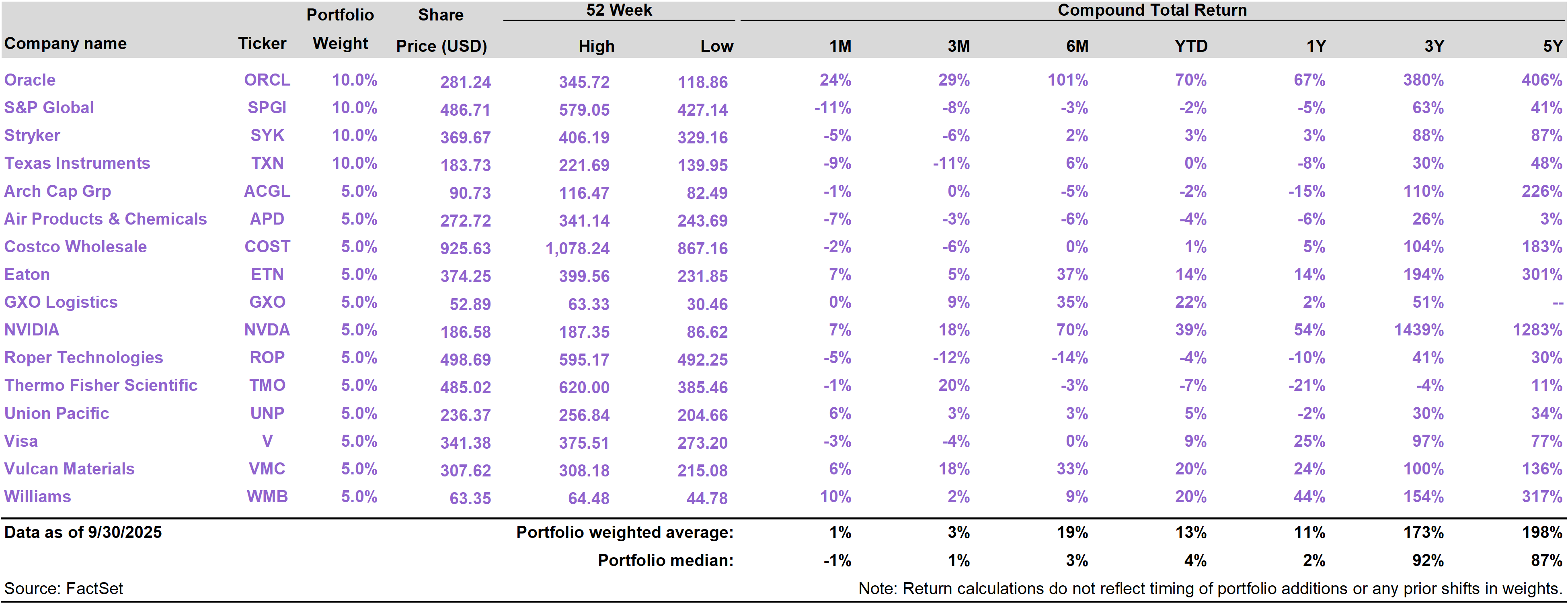

Concerns around the general health of the economy and the consumer likely contributed to the divergence we saw in sector performance.

As AI stocks advanced on reassuring news flow, stocks in sectors that are more cyclical, like Energy, Consumer Staples and Materials, stagnated or retreated.

The “circularity critique”

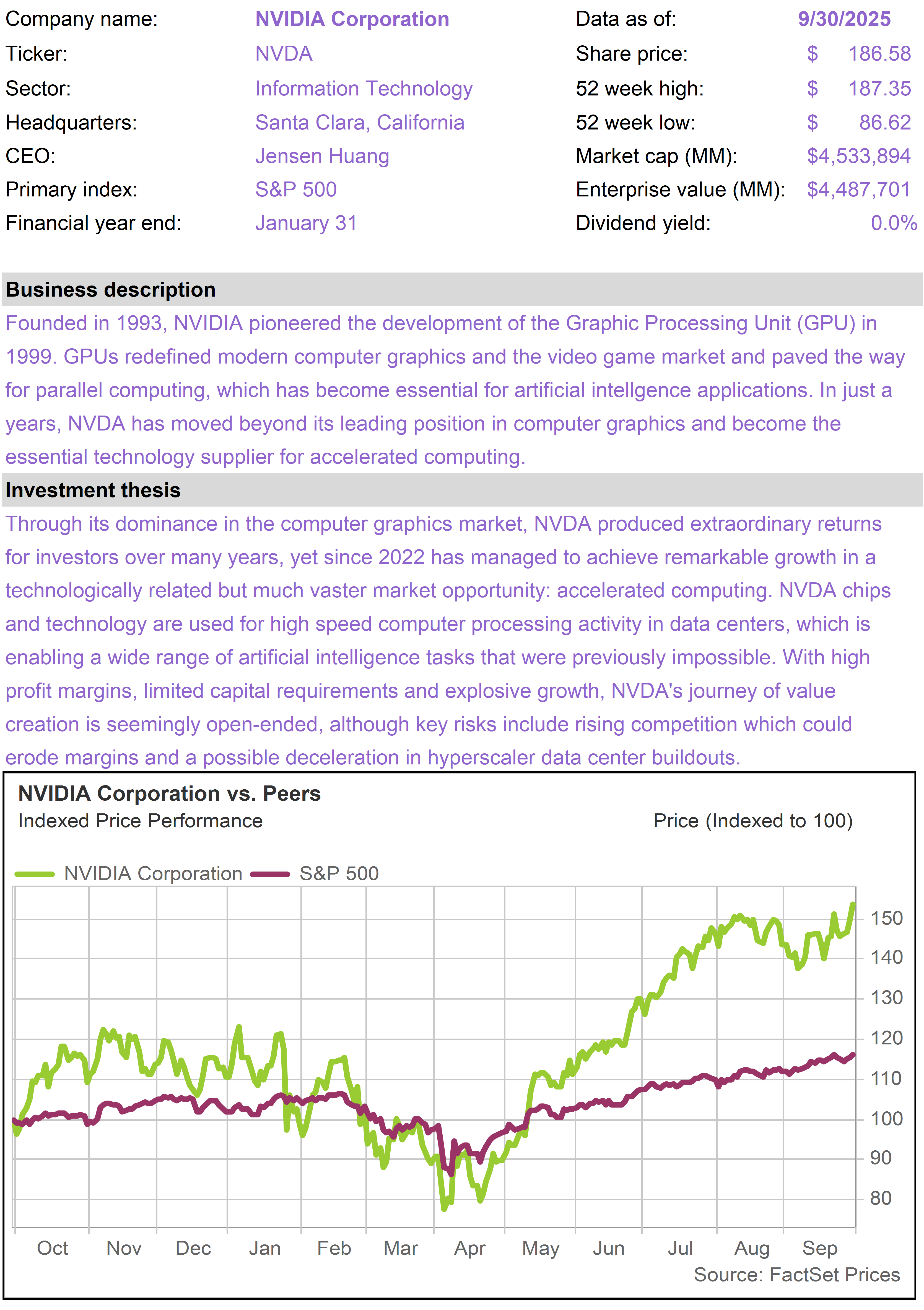

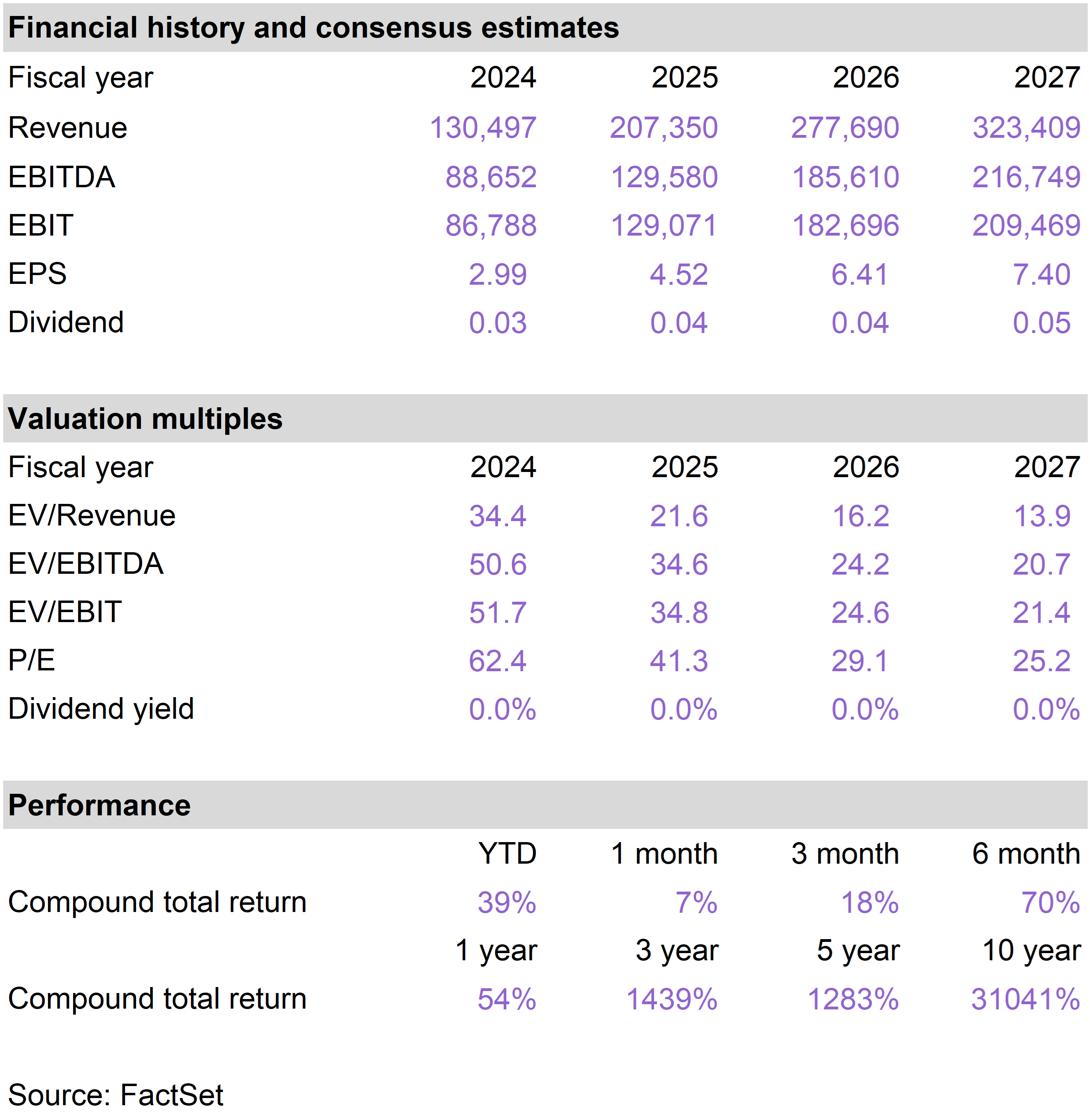

While AI stocks in general performed well in September, skeptics of the AI boom note that much of the demand for AI has been generated by the AI companies themselves.

For example, NVIDIA’s proposed arrangement to invest in OpenAI—which involves commitments by OpenAI to purchase NVIDIA equipment—has been described by some as a prime example of “circular” funding of the AI buildout.

Parallels have also been made to “vendor financing,” with the suggestion being that there is not authentic customer demand. Other examples include NVDA funding AI startups.

While we acknowledge the criticism, we interpret NVDA’s recycling of its vast profits into downstream AI business models as a rational and strategic use of its resources, especially given how it reinforces its own technological grip on the industry.

By making minority investments in these companies, NVIDIA is able to avoid antitrust scrutiny, while still creating favorable conditions for itself as the dominant supplier.

Lower rates either way?

We are optimistic that we are still in the early stages of spending on AI infrastructure, but it is true that AI-related capital spending has become a key pillar of the economy, as other parts of the economy (such as the public sector and housing) have weakened.

To the extent the AI spending boom decelerates, this should only intensify the need for easier monetary policy to offset lower investment demand.

On the other hand, all of this AI spending—should it be sustained or even accelerate—has the potential to drive a disinflationary productivity boom. Knowledge workers will effectively be replaced by much cheaper AI agents.

So even in the context of sustained heavy investment in AI, which would only be justified by real productivity gains, the conditions are created for easier monetary policy.

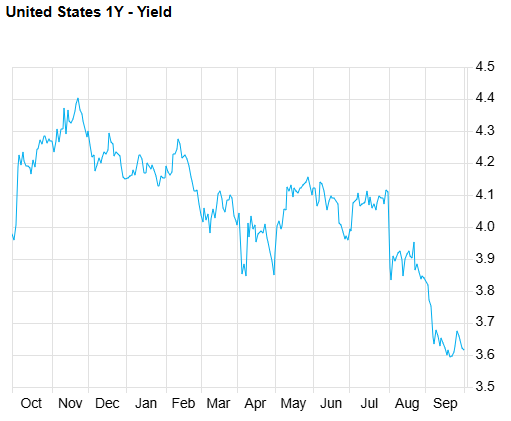

These are longer term considerations. Meanwhile, in the here and now, unemployment rates are ticking up and Trump is preparing to install a new Fed Chair by next May who will undoubtedly be inclined to cut interest rates.

With long-term and short-term indicators pointing in the direct of easier monetary policy, we are not surprised to see gold and Bitcoin attracting capital.

Both of these hard money alternatives—one ancient, one still a teenager—performed well in September.

Gold crossed $3,900 per ounce and is up more than 45% year to date through the end of September. After some recent weakness, Bitcoin is reapproaching all-time highs and has crossed $120,000 as October begins, up nearly 30% year to date.