In a meeting with House Republicans today, President Trump waved an unsent letter to Fed Chair Jerome Powell that told him he was fired. Trump asked his colleagues for their reaction to the idea and then said he would likely go ahead and do it.

In a dramatic twist, Trump later told the press that it was “highly unlikely” that he would fire him.

There is a high stakes battle underway over the future of the Federal Reserve. For several months, Trump has been harshly criticizing Powell over his stance on short-term interest rates, which remain historically high.

Back in April, Trump stated he would not fire Powell after a similar public spat. The law seems clear that he can only fire him “for cause,” meaning serious misconduct, rather than over a policy disagreement.

If Trump did attempt to fire Powell, there would likely be major litigation. Powell’s heavy spending on the Fed’s new headquarters building might serve as an official basis, but there are questions as to whether it would be sufficient after judicial review.

Trump got the public’s attention yesterday when he said, “I think it sort of is,” after he was asked if Powell’s lavish spending on the Fed’s headquarters represented a fireable offense.

Gold and Bitcoin both advanced today as news of Powell’s potential firing surfaced. The dollar was somewhat weaker. Stocks were basically flat, despite the uncertainty.

If Trump actually does fire Powell, it would be a highly unconventional move that in the eyes of many would undermine the institutional independence of the central bank.

Hence, the positive reaction from gold and Bitcoin, non-sovereign monetary assets that tend to rise when faith in fiat money declines. Both are trading close to all-time highs and continue to prove their value as must-own assets in any portfolio.

While potentially somewhat destabilizing, if Powell is removed or resigns under pressure and is replaced with a more dovish Fed Chair, easier monetary policy bodes well for stocks.

Whatever becomes of Powell, it seems obvious that Trump will choose a successor who aligns with his own perspective on the economy.

Powell’s term ends in about ten months anyway. The next Fed Chair will almost certainly be more dovish than the current Fed Chair, which raises what may actually be the most important question facing investors…

Could Trump actually be right on interest rates?

The answer to this question hinges on whether or not rate cuts would be inflationary.

We believe there are some compelling reasons why lower interest rates would not be inflationary, which is positive for investors whether Powell’s term ends tomorrow or next spring.

Trump argues that inflation is under control and high rates are simply making deficits worse by driving up interest expense on the government’s vast debt load.

Powell has argued in favor of a “wait and see” approach. He is also concerned tariffs could be inflationary.

Powell’s stance is generally aligned with mainstream thinking. But is “Too Late” Powell being too cautious?

What if high rates are no longer necessary and are doing more harm than good?

Trump’s view of the matter is perhaps unconventional—but there are indeed reasons to believe the economy can get the benefit of lower interest rates without stoking inflation.

The limits of conventional wisdom

Conventional wisdom holds that the economy is performing well, and inflation is still somewhat higher than target levels, so additional stimulus via rate cuts is probably not necessary.

The Fed actually has various ways of manipulating the money supply in an effort to regulate inflation and employment, its dual mandate.

Adjusting the Fed Funds rate, the short-term rate used by banks for overnight borrowing, is the one most widely watched and understood. Other balance sheet operations can be just as impactful, however.

When the Fed moves interest rates up or down, the basic idea is that it’s a throttle for the economy.

Lowering rates adds more “gas” into the system. People borrow more, spend more, and invest more, so demand for goods and services increases, and prices tend to rise.

When interest rates are lifted, people do the opposite, and there is less pressure on prices.

But the relationship between interest rates and inflation is in many ways more complicated than this. Just look at the experience of other countries.

Japan had ultra-low rates and low levels of inflation, if not deflation, for decades. Emerging market countries with consistently high interest rates have consistently experienced high inflation rates.

We do believe inflation is fundamentally a monetary phenomenon—the more units of money circulating within an economy, the higher prices have to be in terms of those units.

Low rates certainly can increase the money supply by stimulating borrowing, but they also have other impacts.

Shelter costs

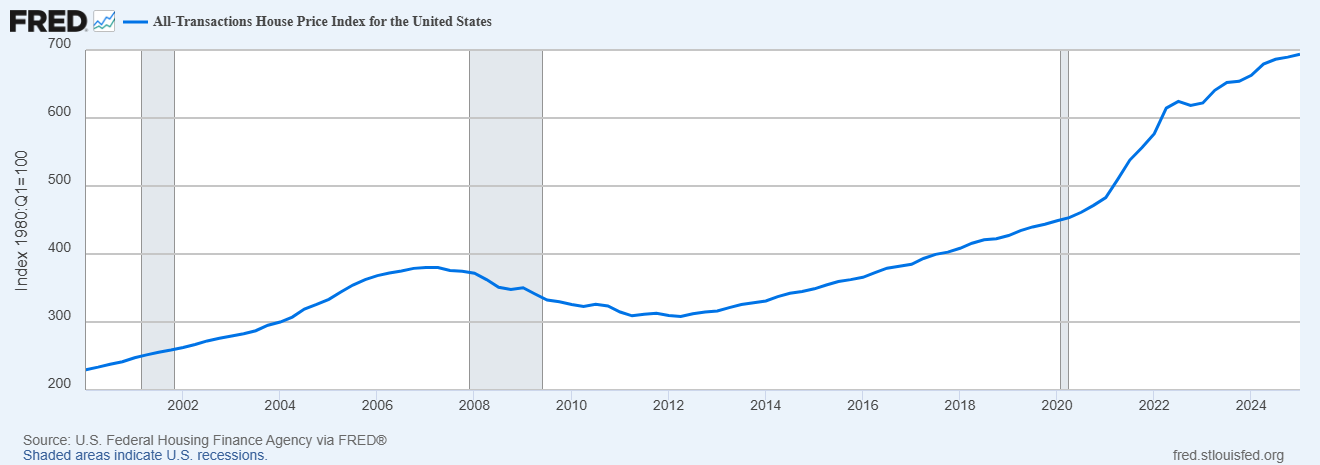

One important area where the interest rate relationship becomes murky is housing.

Shelter, i.e. money spent on your home, is about one-third of the Consumer Price Index (CPI) and just about one-sixth of the core Personal Consumer Expenditures Index (PCE).

Very low interest rates can drive housing prices up, like we saw after the pandemic. But very high interest rates can also deter homeowners from selling, because their new home would require a higher interest rate mortgage than what they might already have.

Consider the hypothetical, and very typical, example of a retired baby boomer couple.

They may want to downsize, but if they do, they have to relinquish their low interest rate long-term mortgage and take on a much higher rate one.

This dynamic effectively traps people in homes and distorts the supply-demand picture in the housing market. Younger families have a reduced supply of homes from which to choose, putting upward pressure on house prices.

Another key factor is new housing starts.

We have record high house prices in the United States currently. One would think homebuilders would be out there aggressively creating new supply to take advantage of high prices.