As businesses increasingly shifted computing and data storage needs off-premises and into the cloud, demand for data center capacity exploded.

Over time, DLR evolved from a niche infrastructure landlord into one of the most important owners of digital infrastructure in the world, operating more than 300 data centers globally.

For years, the business model was relatively straightforward and highly successful.

DLR leased highly secure, power-intensive facilities to enterprises, telecom companies, and cloud providers that needed reliable computing infrastructure. The business generated recurring rental income, steady cash flow growth, and attractive, growing dividends.

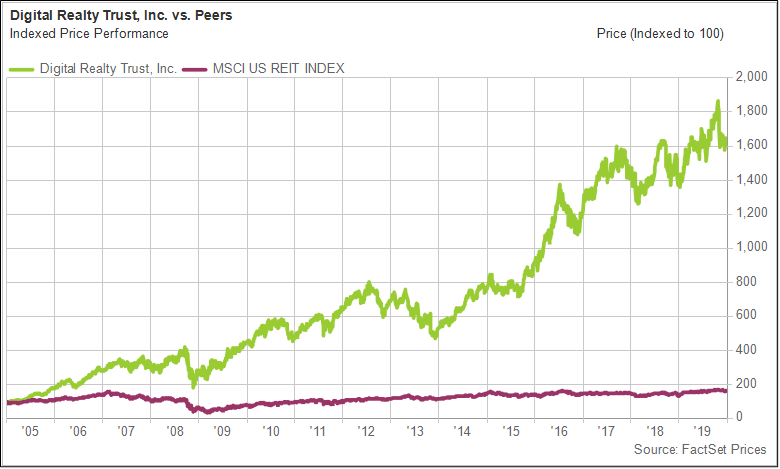

Along with long-term annual returns that nearly tripled the performance of the market, DLR was for many years a dream investment.

Too good to be true?

Then AI arrived—and suddenly many investors believed the old data center model was at risk of becoming irrelevant.

One of the most vocal skeptics was famed short seller Jim Chanos. Chanos argued publicly that traditional data center REITs like DLR faced a structural problem in the AI era.

Modern AI clusters consume vastly more power and generate far more heat than legacy enterprise workloads. In addition, older facilities built around traditional CPU-based computing were generally not designed to support the ultra-dense GPU environments required for large-scale AI training.

In short, Chanos believed many older data centers would become functionally obsolete.

To be fair, there were some elements of truth to his claims, which have weighed on investor sentiment toward DLR and other data center REITs.

The architecture of data centers has indeed evolved. The newest GPU clusters require direct liquid cooling systems, highly specialized networking infrastructure, and enormous power density.

The largest and most advanced AI data centers getting built today do differ in material ways from the fleet of data centers that companies like DLR have assembled over time.

Why Chanos was wrong

The bearish thesis overlooked a few extremely important nuances, however.

One critical assumption the shorts made was that AI demand would be confined to only the largest hyperscale GPU training clusters. What has actually happened is far broader.

AI is moving beyond experimentation and into deployment across the real economy. Enterprises are increasingly building AI-enabled workflows, autonomous software agents, inference systems, recommendation engines, retrieval systems, and internal productivity tools.

Those types of workloads still require enormous amounts of traditional computing infrastructure. In fact, one of the most important developments in AI over the past two years is that AI systems are becoming more infrastructure-intensive—not less.

Modern AI systems require multiple layers of computing that operate simultaneously—leading to an “all hands on deck” scenario.

GPUs handle the massive parallel processing and model inference. This places a higher burden on CPUs to manage memory allocation, run software logic, preprocess data, and continuously feed information into GPU clusters.

Massive storage environments, networking infrastructure, and interconnection layers tie the entire system together. This helps explain why traditional data center infrastructure has remained so resilient.

The market initially viewed AI as replacing traditional computing infrastructure. In reality, AI is layering itself on top of existing infrastructure while dramatically increasing total compute demand.

Contrary to the short sellers’ predictions, the rise of AI did not eliminate the need for CPUs or enterprise data centers. It expanded their role.

Proof is in the pudding

We are arguably now at a point where the debate has been settled. If AI were truly going to damage data center REIT fundamentals, we would have seen it by now.

Rather than contracting into functional obsolescence, DLR is thriving. The stock recently hit an all-time high above $200 per share as it benefits from robust tenant demand and pricing power.

On its most recent earnings call, DLR reported the second highest bookings quarter in its history, record leasing activity in its smaller enterprise-oriented deployments, and rapidly growing AI-related demand.

Management specifically noted that AI-oriented requirements represented a record portion of its leasing activity.

While its existing assets continue to see strong demand, DLR is also leveraging its deep operational expertise to grow through new development. DLR recently signed the largest lease in company history—a 200-megawatt AI-oriented deployment with a hyperscale customer in Charlotte.

Importantly, demand is not coming solely from giant AI model developers.

DLR highlighted growing deployments from pharmaceutical companies, biotech firms, enterprise software providers, cloud businesses, and global technology platforms building AI-enabled infrastructure.

DLR’s growth demonstrates that the AI economy is broadening. This is precisely why NVDA’s move into CPUs matters so much and has the potential to help accelerate the trend.

Jensen’s pivot

Vera CPUs are not designed to compete with legacy desktop processors. They are purpose-built AI infrastructure chips optimized to operate alongside NVIDIA GPUs inside AI factories.

That has several important implications for DLR.

First, NVIDIA’s Vera CPUs have the potential to substantially improve the productivity of existing data center assets, making them more valuable.

Across much of the United States and Europe, power availability has become one of the single greatest bottlenecks facing AI infrastructure deployment. In many markets, securing new multi-megawatt grid connections can take years.

Investors like Chanos frame DLR’s early positioning in the data center business as a liability. But as an early entrant, DLR secured access to power in prime locations before it became such an extremely scarce commodity.

This dynamic helps explain why DLR’s backlog has exploded to record levels and why pricing across the industry continues moving higher. AI infrastructure is increasingly constrained by the availability of deployable power—and DLR was there first.

NVDA has stated that its Vera CPU will deliver materially better performance-per-watt than traditional processors. In practical terms, that means tenants can generate significantly more computing output within the exact same power envelope.

If a tenant operating inside a DLR facility can suddenly double the amount of AI inference without requiring additional megawatts from the grid, the economic productivity of that facility rises dramatically.

In traditional real estate, increasing revenue often requires constructing another building. In AI infrastructure, improving chip efficiency can instantly increase the economic yield of the exact same powered land.

A useful analogy here might be a parking garage that implements a lift system and can suddenly house twice as many cars. Or a pizza parlor that procures new high-tech ovens that can now bake twice as many pizzas per hour.

By making the machinery that lives inside the data center more powerful, NVDA has the potential to make DLR’s existing global footprint of powered campuses and utility relationships even more valuable to its customers.

Second, NVIDIA’s CPU strategy is accelerating a future where AI infrastructure extends far beyond a handful of giant GPU campuses.

The market is gradually shifting from a world dominated primarily by centralized AI model training toward one that is increasingly driven by inference and autonomous AI systems.

Training is the process of teaching an AI model by feeding it massive amounts of data. It can be done in almost any location and requires enormous hyperscale campuses built specifically for ultra-dense GPU clusters.

Inference is the process of actually using the trained model to generate responses, make decisions, and perform tasks. Inference is essentially the AI model getting put to work in the real world.

As AI becomes embedded into software, coding assistants, robotics, search, cybersecurity, and autonomous workflows, companies increasingly need broader computing infrastructure surrounding the AI model itself. This includes CPUs to manage workflows, networking to move data, and storage systems to support continuous real-time operation.

Here again, DLR’s status as a legacy data center operator represents a competitive advantage—not a liability.

Many of those workloads can operate efficiently inside upgraded traditional data centers because they are not quite as energy-intensive as large-scale model training.

On top of this, proximity to the customer and its data becomes extremely valuable as the world moves toward AI inference.

Training large AI models can occur inside giant remote campuses built around cheap power. But inference-oriented AI systems need to sit closer to businesses, applications, cloud networks, and end users in order to reduce latency and move data more efficiently.

Ironically, this proximity is exactly what DLR’s data center portfolio was originally built for.

Long before the AI boom, DLR spent decades building highly interconnected facilities located near major population centers, enterprise customers, telecom networks, and cloud ecosystems so businesses could access data quickly and reliably.

That legacy footprint leaves DLR extremely well-positioned for the next phase of AI infrastructure, which requires physical closeness to actual customers.

First mover advantage

Concerns from a few years ago that traditional data center footprints were becoming obsolete are giving way to a very different reality.

Older data center facilities may be less optimized for massive AI model training, but they are becoming increasingly relevant as AI infrastructure spreads across the real economy.

NVDA helped define the modern AI market. Now the company is signaling where the industry is headed next.

Ironically, that direction looks increasingly similar to where the data center business originally began: infrastructure located close to businesses, networks, cloud ecosystems, and end users.

DLR’s portfolio was built around exactly this type of proximity. For decades, the company assembled highly interconnected facilities in prime connectivity hubs where access to power, fiber, and low-latency networks was most valuable.

Thanks to the strength of this footprint, DLR is already benefiting from favorable supply-demand dynamics across its markets. We see this in consistently strong leasing activity and substantially higher renewal rates as leases expire.

Now, with NVDA moving aggressively into CPUs, we may be in the very early stages of a major new wave of demand for space inside DLR facilities.

For more than two decades, DLR has been methodically assembling a global data center portfolio. As competition for access to this supply-constrained infrastructure intensifies, DLR shareholders stand to reap the rewards.