So what is really happening?

A pessimistic read on the gold rally is that the world is becoming unsettled.

If you dislike Donald Trump and have great distrust for his foreign and economic policy agenda—an attitude that is pervasive across the financial media and the mainstream investment community—you may be inclined to interpret the gold rally in this way.

The problem is that almost all the other financial and economic indicators are sending a different message.

While geopolitical and macroeconomic changes continue to play a role, there is another dimension to the gold rally that investors need to understand:

Gold is being accumulated because it is a supply-constrained store of value in a world that is in the early stages of an AI-driven productivity boom.

This boom has the potential to generate enormous wealth that needs to find a home.

Gold is not rallying because investors fear economic decline. It is rallying because gold offers a unique form of scarcity, and scarce assets tend to appreciate as wealth multiplies.

The link to monetary policy

Gold investors are very sensitive to perceived changes in monetary policy. Gold rallies when monetary policy is becoming easier. We saw this in the aftermath of the Global Financial Crisis, when gold more than doubled between 2008 and 2011.

There is a straightforward explanation for this. The more liquidity central banks like the Federal Reserve create (i.e., the more money they print), the more paper money is available to buy a limited supply of gold.

Monetary policy normally becomes much easier when central banks are confronting deflation.

In our highly indebted fiat money system, deflation poses unacceptable risks. Deflation makes debt more expensive in real terms (whereas inflation makes debt more manageable).

Debts burdens—whether at the government level or in the private sector—can quickly become unsustainable in deflationary scenarios, leading to defaults, bankruptcies and economic depression.

Inflation is bad, but deflation is a central banker’s worst nightmare. This is why the Fed informally targets 2% inflation rather than 0%—to provide a margin of safety against worst case deflationary outcomes.

After the 2007-2008 financial crisis, the Fed under Ben Bernanke was desperately afraid that excessive private market debt levels would lead to a deflationary spiral. For the first time, the Fed implemented Quantitative Easing (QE), a method of providing additional monetary stimulus when short-term interest rates were already at zero.

Back then, the deflation threat came from businesses, financial institutions and households whose balance sheets were obliterated by the bursting of the housing/mortgage bubble. The Fed went to extreme lengths to make sure this deflation risk did not materialize, and gold investors benefited.

Productivity-driven deflation

Deflation can be driven by a collapse of economic demand, but it can also be caused by falling prices as producers become more efficient. In contrast with the Global Financial Crisis, we see the deflation threat today coming from a much more benign source: productivity growth.

Productivity growth is accelerating. On January 8, 2026, the Bureau of Labor Statistics announced that third quarter 2025 productivity growth was 4.9%, versus 1.9% in the same quarter a year prior.

This is a rapid improvement. The U.S. economy generated 5.4% more output, while total hours worked only increased 0.5%.

Productivity growth is inherently deflationary. It signals that the economy is operating more efficiently, generating more output per unit of human labor.

Technological innovation is what makes that possible.

One of the starkest examples of productivity-driven deflation is flat screen televisions. Thanks to technological progress, the price of a typical television has plunged, even as quality has improved.

Consumer electronics have led the way in goods deflation in recent years and decades, but what if, thanks to AI and other advances in technology, many other sectors start to see falling prices as well?

Across industries, if businesses can generate more output with fewer workers, their costs go down. If the industry is competitive, as most are, this should lead to lower prices as businesses become more efficient and seek to grow market share.

Consider how this played out with televisions. Production costs went down, and profit margins went up. This allowed new entrants to come into the market and compete on price, sending prices down across the board.

Inflection point

We are potentially in the early stages of this productivity-driven deflation dynamic. Official inflation estimates are still closer to 3% than 2%— but there are signs it is happening.

The Fed started cutting interest rates in the second half of last year because it was observing decelerating inflation and incremental pressure on labor markets.

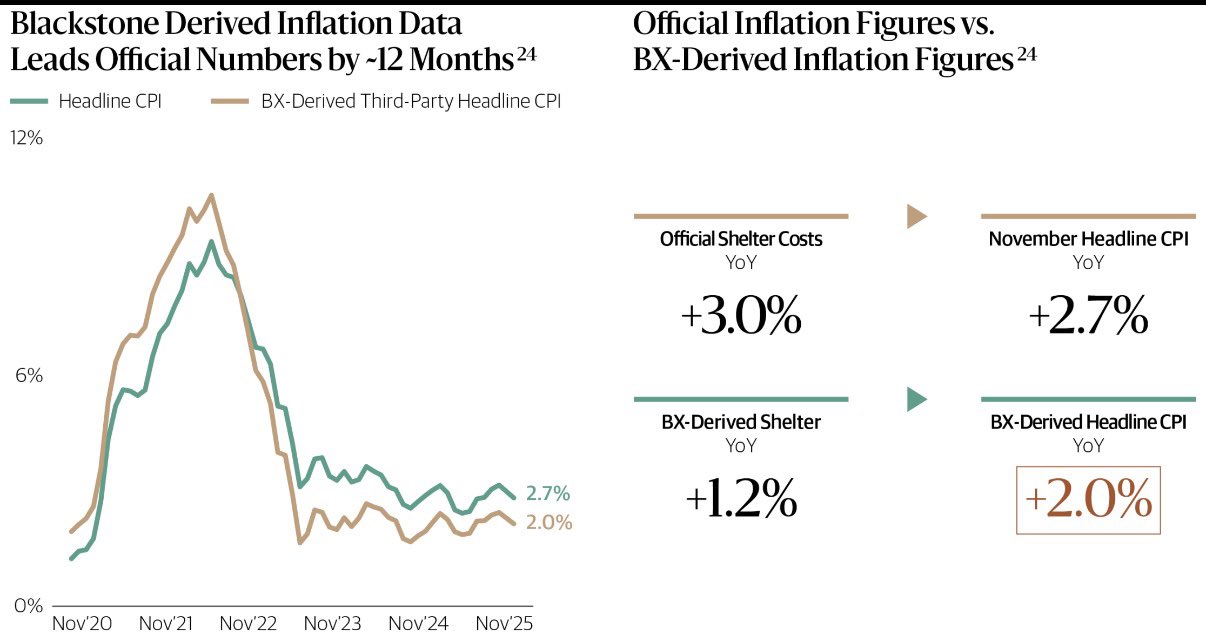

There is also evidence that current inflation is not as bad as official statistics.

Blackstone (BX) is the world’s largest commercial real estate owner with unique visibility into the housing market. Shelter costs are a major component of the Consumer Price Index (CPI) and among the most complicated to track because rents reprice only gradually.

According to BX, which uses its own internally generated data to track inflation, we are already at 2% inflation rates.