Productivity growth is inherently positive, not just for investors but everyone in the economy. Productivity is prosperity itself—having more with less effort.

Corporate layoff announcements coming out of Amazon and elsewhere are disconcerting, especially from the standpoint of white collar professionals seeking to maintain gainful employment. But it’s a good news for shareholders.

Labor costs as a percentage of corporate revenue are typically about equal to operating profit margins (around 10% to 15%).

If human beings are effectively being replaced by AI systems, saving money for companies, this clearly justifies demand for AI equipment. It also means higher corporate profits and/or lower prices (as firms become more efficient and compete with lower cost structures).

To the extent unemployment rises and wages stagnate, this may weigh on consumer spending and confidence… but as we are already seeing with the Fed’s response to softer labor market conditions, it also means easier monetary policy.

I have long-term confidence in the economy and the stock market based on my belief that AI will yield substantial productivity benefits. This will manifest as rising corporate profits and lower levels of inflation, which will allow monetary policy to be highly accommodative to support job creation.

Growing earnings, low inflation and easy money are what every investor in the stock market should hope for.

(2) Volatility is possible/likely. Just be prepared.

Even if the long-term trajectory of the stock market is up and to the right, there will of course be bouts of volatility along the way. There always have, and there always will.

April 2025 was a prime example. Trump came out with a surprisingly tough initial stance on tariffs, and stocks went into freefall. It was scary and painful at the time, but the right thing to do in retrospect was (a) not to sell and (b) buy if you could.

The economy is rapidly changing, in my view, for the better, but these changes can be disruptive and may lead to episodes of risk aversion. Personally, I just try to be mentally and financially prepared for this.

I tend to maintain some dry powder (cash or short-term bond investments) that I can deploy in periods of turbulence to take advantage of market dislocation. At the very least, it helps satisfy the psychological itch to “do something” amidst all the uncertainty.

(3) They will print.

Let’s assume, for argument’s sake, this really is an AI bubble. In this scenario, AI is overhyped. We don’t need all these data centers. Tech stocks are overearning. Tech growth rates are way overestimated. The capital spending boom comes to a halt.

Ironically, this scenario, were it to play out, might look a lot more like the 2005-2008 housing bubble than the late 1990s tech bubble.

In the housing bubble years, we had a major asset class (real estate) that was totally overvalued, thanks to bad government policy, crazy lending practices by banks and fraudulent behavior in the mortgage-backed securities market.

During the housing bubble, the economy was booming as home prices surged and new homes and entire communities were being built at an aggressive pace. Single family homes were the data centers of that era.

When the music stopped, we saw a dramatic reduction in household wealth. Capital spending also plunged because the housing market was now massively oversupplied. Because of vast leverage, the housing bubble led to a financial crisis, which severely exacerbated the problem.

Fortunately, there is much less financial leverage involved in the AI buildout, which is largely financed by corporate cash flows and equity rather than debt.

In addition, the banking system is (hopefully) more resilient today given legislative changes that came out of the financial crisis. In any event, it is certainly less leveraged.

To the extent AI, which is now the economy’s primary growth engine, turns out to be a bubble that bursts, we would likely see a sharp collapse in demand across the economy.

But this would almost certainly be followed by a profound monetary response.

The reality of our highly leveraged fiat money system is that it cannot tolerate a collapse in asset prices. Progressive taxation means the government is largely funded by taxes on the highest earners.

If these taxpayers—the 10% of the U.S. population that owns 70% of total household wealth—go down, the federal government goes down with them.

We saw this movie after the tech bubble burst, after the housing bubble burst, and during the pandemic. If there is a major economic disruption, the Fed steps in, cuts rates, initiates quantitative easing, and floods the economy and the financial system with liquidity to protect asset prices and keep the economy moving.

When paper money gets printed, supply-constrained assets usually perform well. Gold historically tends to be a great hedge in scenarios like this. Bitcoin could emerge as one as well.

Interestingly, both the best case scenario (productivity boom) and worst case scenario (bubble burst) would logically lead to aggressive money printing.

In the productivity boom scenario, the Fed eases to create jobs and counteract productivity-driven disinflation. In the bubble burst scenario, the Fed eases to create jobs and counteract deflation from collapsing demand.

Gold and Bitcoin will arguably do well either way. There is a reason we write about these two assets a lot!

(4) It’s still early.

While I always worry about market volatility, my biggest regrets as an investor have been missed opportunities as opposed to sustaining temporary losses during market corrections.

We are really only about two to three years into a technological wave that will touch every single industry and household in the world (with the possible exception of members of tribal cultures buried deep within the rain forest).

Some people are terrified by the prospect of loss. They toss and turn at night worrying about the next catastrophe on the horizon. Some people, like my friend Chuck West, stay up all night figuring out how they can win.

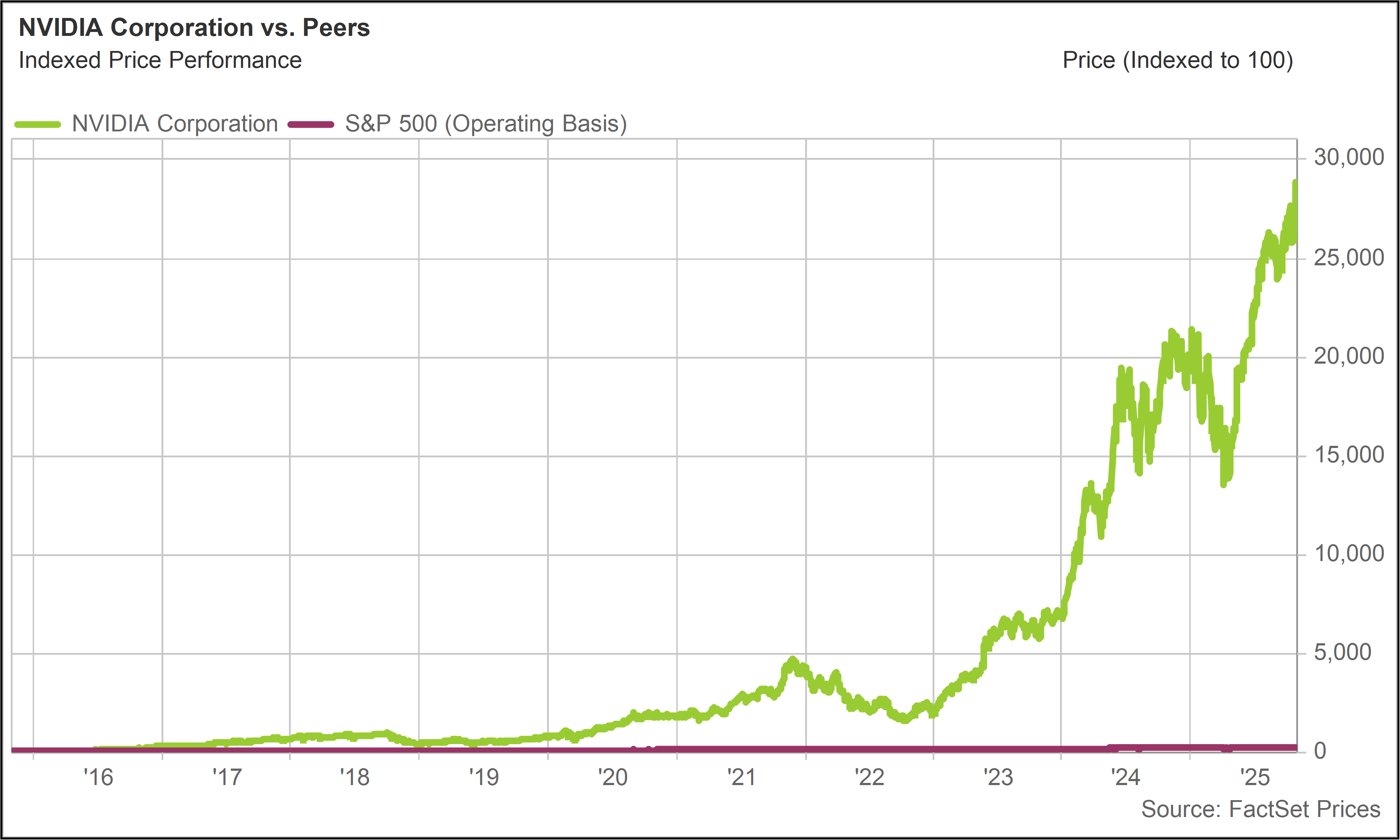

With no real training whatsoever in finance, business or technology, Chuck may have gotten lucky with NVDA. Or maybe his mind is so dialed into what it takes to succeed, he was able to intuitively put the pieces together and figure out this business was something special.

Either way, as he would say, he made a ****load of money.

The changes underway in the economy are unsettling, but they are exciting. We can and probably will see some turbulence along the way.

Personally, I want to maintain my diversified exposure to the enterprises that are changing the world and the scarce assets that may appreciate substantially in a world of AI-driven abundance.