Tariff pros and cons

Prevailing economic models depict tariffs as harmful. The thinking is that tariffs make everyday goods more expensive and disrupt how markets normally work.

By taxing imports, tariffs push companies and consumers to buy higher-cost alternatives instead of cheaper or better ones from abroad. That raises prices and lowers purchasing power.

Tariffs can also hurt businesses that rely on imported inputs. They can trigger retaliation from other countries, reducing exports and global trade.

In these widely accepted models, tariffs make the economy less efficient overall, with slower growth and lower living standards—even if some domestic industries receive short-term protection.

What the conventional wisdom on tariffs arguably misses, however, is that tariffs can drive better economic outcomes as a negotiation tool. Just as they can cause harm through retaliation, they can create benefits from compliance.

The threat of tariffs (or higher tariff rates) has persuaded other countries to make significant investments in the United States, which helps boost growth. The threat of tariffs has also driven other concessions, like facilitating more U.S. exports.

Tariff critics tend to overlook another important point. Yes, tariffs can be damaging as a form of taxation… but they allow for lighter taxation elsewhere in the economy.

The federal government needs to generate revenue somehow. Tariffs create certain inefficiencies but so do personal income taxes, taxes on investments, and taxes on corporate profits.

Any revenue generated from taxes gives the government leeway to tax other economic activities less heavily. Standard economic models tend to look at tariffs in isolation.

Beyond tariffs

As interesting as the tariff debate is, it is possible, if not likely, that it is also a bit of a distraction.

In mid-December, New York Fed President John Williams estimated that tariffs added 0.5% to inflation in 2025. He also shared his view that this impact was a one-time event.

Half of one percent is not zero, but in the grand scheme of things, it is somewhat insignificant.

The Consumer Price Index (CPI) rose 24% over the past 5 years, with the vast majority of this occurring prior to Trump taking office. If Williams is right, tariffs accounted for only 2% of the inflation we have experienced since the end of 2020.

The reality is that the U.S. economy is influenced by many factors other than the fees assessed on foreign imports.

To attribute everything that happens to the economy to tariffs, good or bad, is like thinking a car’s tires are all that matter as far as how well it can perform. Sure, the quality of tires can make a difference, but other variables, like how big the engine is, or how skilled the driver is, count much more.

The financial media seems to like to dwell on tariffs because it is the key economic policy controversy that separates Trump from the mainstream. If the economy falters, for whatever reason, they can point to tariffs as the cause—a self-inflicted wound for which Trump alone is responsible.

The media may continue to cling to its narratives, but investors should focus on what really matters, especially as tariff impacts recede into the rearview mirror.

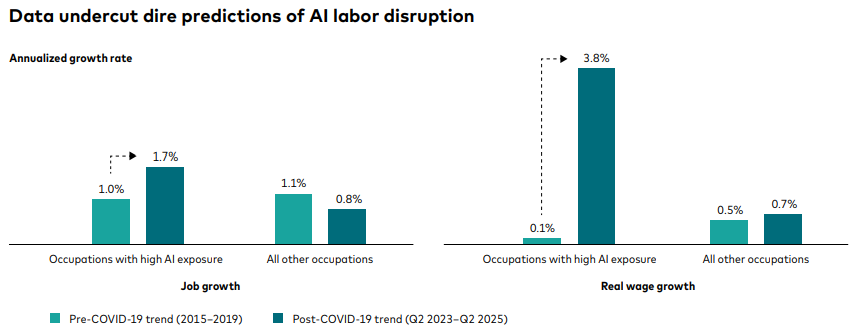

What is really making the difference in the U.S. economy now is innovation-driven growth, particularly as it relates to AI. And we are now seeing it show up in the numbers in the form of strong productivity growth and mild inflation.

What about jobs?

Not everything is perfect. GDP growth may be high, inflation may be coming down… but the unemployment rate has in fact been rising.

The unemployment rate was 4.6% in November 2025, up from 4.2% when Trump was elected in November 2024.

Rising unemployment is both a frightening headline and, for many Americans, a practical reality they encounter in their own lives.

The increase in the unemployment rate also aligns with emerging fears that AI will lead to widespread joblessness. This helps explain gloomy public sentiment, which Trump’s political opponents are certainly keen to promote.

In early December, Senator Bernie Sanders called for a moratorium on all new AI data center construction, claiming among other things the potential risk of 100 million jobs disappearing.

While there is much to criticize in Sanders’ desire to bring technological progress to a halt, his stance on AI points to a more general concern—and it is a valid one—that the AI economy is “K-shaped.”

Many Americans are not at the moment benefiting in a direct way from the strong stock market and the tech sector boom.

Those at the top are thriving—well-paid, with growing portfolios.

Those at the bottom, including the 40% of the U.S. population that has no ownership of stocks, are legitimately worried that their livelihoods, from cab drivers to call center workers, will soon be eliminated by technology.

Rising unemployment rates are naturally alarming, especially when they are paired with hard to decipher technological change. But a closer look at the details of recent employment trends should provide some comfort.

Job losses are largely public sector

Almost half the rise in the unemployment rate over the past year is explained by shrinking federal government payrolls. The Trump administration has deliberately reduced the federal government’s footprint.

Federal government employment is down 271,000 since reaching a peak in January 2025. This is against a base of approximately 160 million public and private sector jobs in the United States.

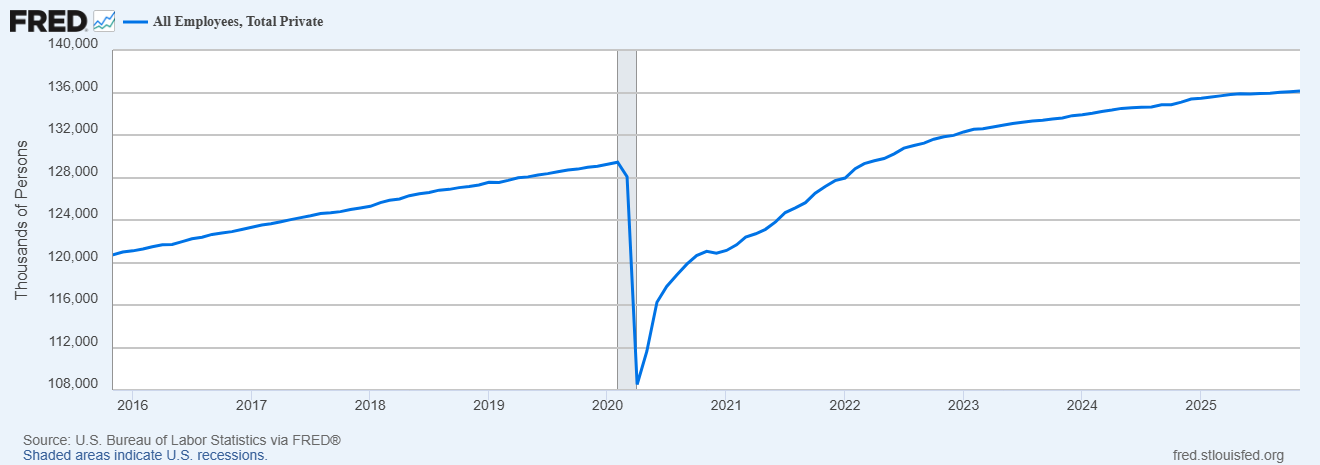

Meanwhile, private sector employment continues to grow, albeit at a slightly slower pace than it has over the past few years.