If you walked into the bedroom of a typical American middle school kid in the 1980s, you would probably not find a stack of company annual reports on the bookshelf. The same applies to the home office of a typical middle aged man in 2025, decades after the invention of the PDF file.

My upbringing was perhaps a little different from most.

Instead of Sports Illustrated, I collected glossy annual reports that my father would drop off in my room after we got them in the mail. And I’ve actually got a stack of them on my desk right now.

To be fair to my high school self, the annual report pile would later primarily function as a way of discreetly storing swimsuit issues in between. I wasn’t totally abnormal!

My investing “origin story”

Investing may not be the most common family pastime, but there are certain benefits if it is.

Children learn from their parents many things that they cannot learn in school—habits, attitudes, moral boundaries, life skills. So much of who we become as adults is connected to the patterns and behaviors we witnessed as children.

This very much extends to personal finance, especially since our K-12 education system barely touches the subject at all, which is unfortunate.

What most of us know and believe about spending, saving and investing, at least initially, is shaped by our parental role models.

I was lucky enough to have a father who was a highly engaged investor. He not only invested personally, but, as an economics professor, he even taught classes on investments.

My dad liked dividends. He still does. The Income Builder Model Portfolio is his personal favorite. He was also an investor in the dividend-focused mutual funds I previously managed.

He actually taught me the dividend discount model when I was in middle school.

It’s one of the original valuation methods for stocks—basically an algebraic formula that involves dividing the expected dividend by the assumed cost of equity minus the long-term growth rate.

Cracking the code

Companies still send annual reports to shareholders. (You can’t let them trick you into opting out of paper delivery.) Back then, well before the Internet, investors really relied on them for information.

One annual report that sticks out in my memory was the one from Beatrice Corporation.

The company no longer exists, but it was a giant food conglomerate that owned brands like Tropicana and Dannon. I probably was impressed by the fact that they made the orange juice and yogurt I always saw in the fridge.

I remember investigating Beatrice with my dad. I don’t recall the exact figures, but the stock definitely offered a nice chunky dividend.

Our investment research activities included trips to the local public library. We would go to the reference area upstairs in the “grown up” section and flip through the Value Line Investment Survey.

Back in the 1980s, this was a thick book with very useful one or two page company write-ups with key pieces of information… not too dissimilar from the Company Snapshots we now include in all of our Model Portfolio reports.

My father and I would look up stocks that we owned, like Beatrice, take some notes, and maybe even photocopy a few pages.

I enjoyed the trips. It was like doing detective work, or better yet, cracking some kind of secret code.

Beatrice provided what may have been my first lesson as a value investor.

It was eventually acquired in 1986 by Kohlberg Kravis Roberts & Co. (KKR) for over $6 billion. It was one of the largest leveraged buyouts at the time.

Shares rallied about 50% from where they were before the deal was rumored. We were quite pleased.

KKR ultimately sold off all the divisions within the company and made even more money. The businesses within Beatrice were worth way more than the stock market was giving the company credit for.

Beatrice was a cash cow, which the high dividend reflected. If you appreciated how valuable the underlying businesses were, you could have been a Beatrice shareholder as well and made a lot of money.

The appeal of investing

Investing has always been a major part of my life. I eventually became a professional investor, managing money for others, but have always invested my own money.

Probably the thing I like most about investing is the way it integrates basically everything in life… math, science, technology, psychology, politics, history. You’re constantly solving puzzles that challenge every part of your mind and understanding of the world.

The other nifty thing, of course, is being able to make a lot of money without really doing anything other than reading, thinking and perhaps performing some calculations.

The ability to turn a dollar into two with just a few keystrokes and a little time is pretty magical.

As a kid who liked to do his own thing, I understood that it’s definitely a better way of obtaining money than completing tasks that some other person tells you to do.

I was fortunate enough to have an influence in my life who familiarized me with investing and its potential pay-offs.

For many people, however, investing seems very complicated and intimidating. They keep their distance and as a result often miss out.

Extending the legacy

I have three sons myself now, two of whom are legal adults. They are attending or on their way to college and have set up their own independent brokerage accounts.

The youngest is not much older than I was when I would go on the fact-finding missions to the library.

I’m not pushing my sons to become professional investors themselves, nor am I discouraging it. I want them to find their own path and pursue their assorted talents as they see fit.

But whatever direction they go career-wise, I do want them to know as much as they possibly can about investing.

At this stage of my life, I appreciate how investment decisions I made (or didn’t make) decades ago have had major consequences for my family today.

So for the benefit of my sons, I decided to distill what I think are the key things they need to understand and prioritize as they begin their adult lives and investing journeys.

I also wanted to share these thoughts with our 76research subscribers.

Many of you, of course, have kids of your own. One subscriber in particular has mentioned to me that he uses our content to help his own son develop as an investor. Trish and I are thrilled to be helpful in that way.

NINE THINGS I WANT MY SONS TO KNOW

What follows below is not necessarily conventional financial advice. It reflects my own personal psychology around investing, convictions about how our economic system works, and attitude towards risk.

But after several decades as both a professional and private investor, this is where I land… and what I want my boys to know.

Take from it what you please!

(1) Never forget the basic arithmetic of wealth accumulation.

Let’s start with the easy stuff. This may sound painfully obvious, but too many people overlook it.

If you want to accumulate wealth, it breaks down to three main variables.

First, you have to figure out a way to earn money. So get a good job or maybe even start a business.

But remember, no matter how much money you make, you will literally have nothing at all to show for it, unless you actually save a portion of it.

In fact, someone who earns a lot and but fails to save could end up in even worse condition than someone who earns far less. Big spenders who suffer a decline in their income might struggle to maintain all their pricey possessions, which can turn into liabilities fast.

After you earn and save, you then need to generate high returns.

If you invest $10,000 at a 4% return (approximately equivalent to current savings account yields), it becomes around $22,000 in 20 years.

If you can get a 10% return (the approximate return of the S&P 500 over the past 10 or 20 years), it becomes around $67,000 in 20 years.

Your savings compounded at 10% over 20 years will be more than three times higher than it would be at 4%.

So compounding at this higher rate has the same long-term effect of either earning three times as much money at a given savings rate, or saving three times as much off the same level of income.

To sum it all up, if you want to accumulate wealth, you need to earn as much as you can, then save a lot of it, then try to get good returns. This applies to everyone and will always be true.

(2) You should be fearful of missing out.

Fear of missing out, also known as FOMO, is often depicted as a psychological weakness, especially in the context of people who may be spurred to action after seeing a stock or other investment rise a lot.

Chasing whatever may be hot at the moment is not necessarily a good idea. You don’t want to fall for every investment fad you encounter.

But you should have a healthy respect for the risk of missed opportunity. And don’t be too skeptical. An investment that appreciates rapidly can also signal genuine long-term potential.

Elon Musk is the richest person in the world because he imagines what’s possible. Every great investor I ever met has a certain optimism that allows them to think through and visualize upside scenarios.

Negative Nellies avoid mistakes but miss major opportunities because their minds don’t allow them to contemplate the possibility of great outcomes.

The stock market is constantly fluctuating, with all kinds of bubbles and crises along the way. Many people are paralyzed with fear of the next crash.

To be fair, there have historically been periods of poor returns that lasted years.

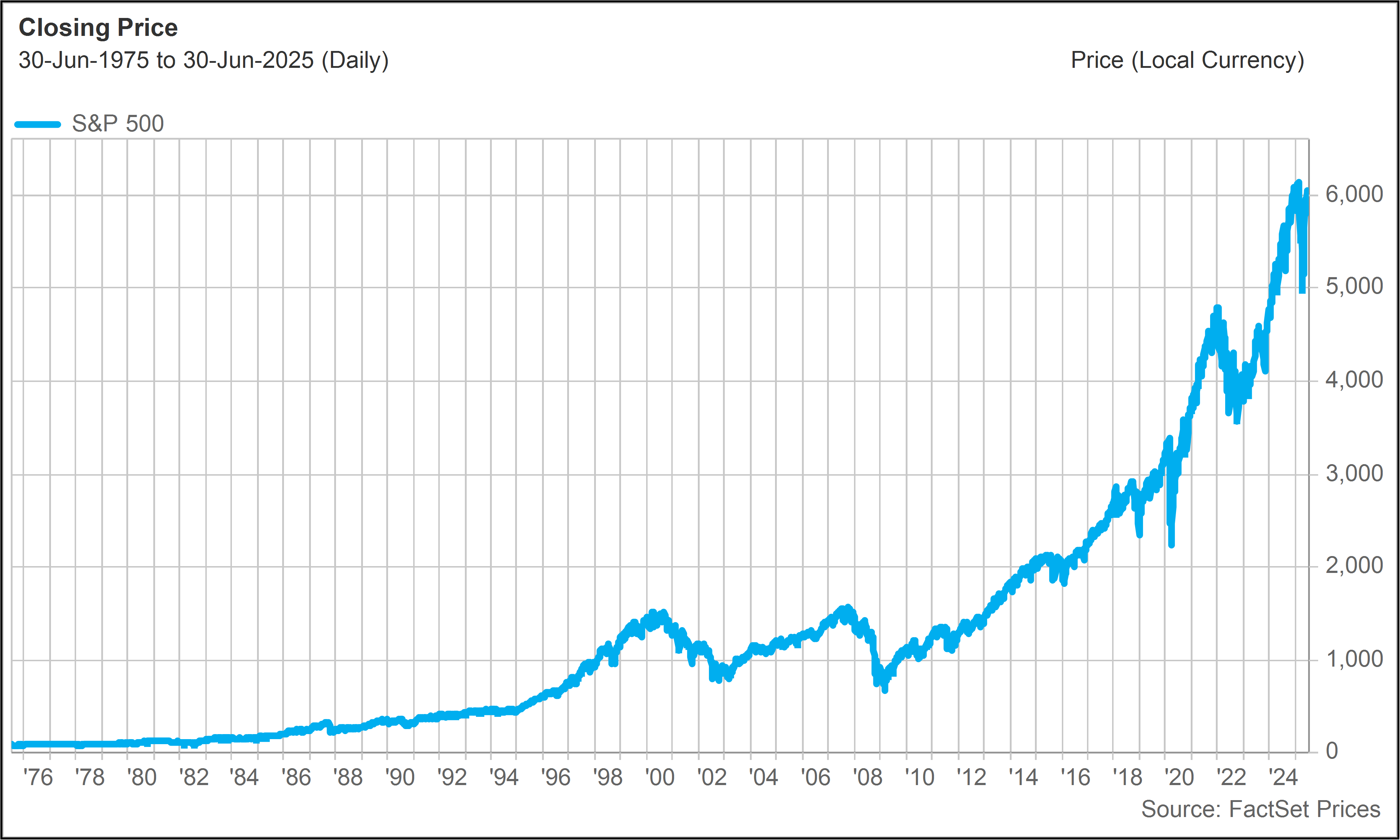

The long-term trajectory of the stock market is up, however, because businesses in a free market system are able to grow their earnings and because the money supply is constantly growing, especially in periods of market weakness.

Our economic system fundamentally relies on the stock market performing well. If earnings do not grow organically, the Fed makes sure they grow nominally.

If you are young and in the wealth accumulation phase, you may not even mind if you temporarily lose money in stocks.

You are continuing to earn money and save money. If stocks are out of favor and valuations are low, this just gives you more time to build positions at lower levels.

Short-term declines of 10%, 20% or 30% or more are not fun, but they get washed away over the broad sweep of time.

The S&P 500 Index was under 100 on June 30, 1975 and over 6,000 on June 30, 2025. Over 50 years, it became 65 times larger.