Gold is actually quite abundant within the earth’s crust, but it is also extremely expensive to find and extract. Despite the impediments to gold mining, the supply of gold does increase over time, typically 1% to 2% per year.

Bitcoin was specifically designed such that its supply growth going forward will be very limited. Only 21 million Bitcoin will ever be mined, and the last Bitcoin block is expected to be mined in 2140.

The supply of Bitcoin is expanding at less than 1% per year currently. This “inflation rate” will continue to decline over time.

Bitcoin’s supply is still growing, but the rate of growth is so negligible that it can almost be ignored now.

While the total nominal value of other forms of money grows because of supply growth, increases in the value of Bitcoin flow directly into the price.

So as Bitcoin takes market share of the total global money supply from gold, U.S. dollars, Euros, etc., this gets manifested as price growth in Bitcoin. Fewer new units are being created, so the units are getting more valuable.

An even larger addressable market

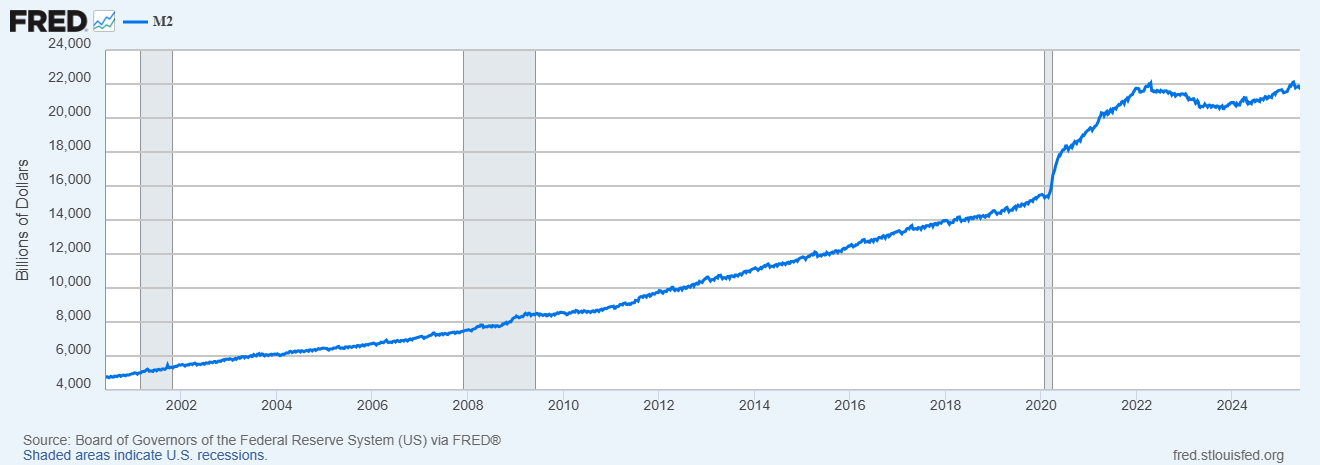

It may be limiting to think of Bitcoin as competing only with gold and M2 money, which is basically bank deposits. M2 money is just money that is lent to financial institutions that can be accessed in short-order.

There is much more money in longer term financial obligations, i.e. bonds.

There is not a tremendous difference between a bank deposit and a bond. A bond is just a promise to pay certain amounts of money to other parties at agreed upon dates.

Like bank deposits, bonds, generally speaking, have no direct connection to any other asset. They are promises to receive payment in a particular currency on a particular timeline.

A depositor is also lending his money to another party. His ability to access that money may be greater and its vulnerability to fluctuations in value may be much lower, but the arrangement is fundamentally similar.

Both bank accounts and bonds are just ways to store money. Bank accounts have better liquidity and offer stability of principal, whereas bonds carry higher risk and typically offer higher returns.

The global bond market is estimated to be around $300 trillion.

So if we add bonds to global M2, the total market for pure monetary savings instruments (which have no value beyond the currency in which they are denominated) is some $400 trillion or more.

Bitcoin currently represents about 0.6% of the addressable market, defined in this manner. An argument could be made to include other assets (stocks, real estate, commodities) as well, but it’s unnecessary, since Bitcoin’s share is still so small.

Based on this math, if Bitcoin appreciated by a factor of 10, it would still only be 6% of the addressable market. And this ignores how the addressable market continues to grow every year from constant fiat money creation.

Why it could happen

The main reason any system or technology prevails over another one is that it’s better.

Email at some point early on may have seemed like a gimmick.

Before internet-based email took off with services like Hotmail and Gmail, it was somewhat difficult to use and required access to some kind of corporate or institutional computer system.

The U.S. Postal Service has reported an approximately 50% decline in physical mail delivery over the past 20 to 25 years. Meanwhile, the number of emails sent globally has ballooned to nearly 400 billion per day.

Snail mail still has certain advantages, but email has emerged as a superior communication method across a wide range of use cases.

Bitcoin similarly represents a technological innovation that addresses some key flaws of fiat money as well as gold.

Bitcoin is not controlled by any government entity, and it has a fixed supply schedule. So it is not vulnerable to debasement and dilution (i.e., supply growth via money printing).

Bitcoin is globally accessible and fundamentally does not require participation in any government regulated financial network.

Large quantities of Bitcoin can be purchased, sold or transferred almost instantaneously, while sending money through traditional methods can take a long time and involves fees and third parties.

The incumbent’s advantage

Fiat currency will not disappear anytime soon. Even if Bitcoin represents a superior savings technology, a premise that is open for debate, there is enormous inertia supporting the fiat system.

Like Bitcoin, fiat money is not backed by any other asset, notwithstanding historical linkages to gold and silver.

One can think of fiat money as comparable to a ticket one receives to purchase rides and food within an amusement park.

In order to participate in the amusement park called the U.S. economy, which includes the ability to pay taxes to the U.S. government, you need to operate in U.S. dollars.

The desire to have access to the U.S. economy is what fundamentally creates demand for dollars. The same applies to other countries that operate with a currency that they print and control.

Sovereign currency issuers have the coercive power of the state behind them, yet Bitcoin is making incremental gains around the world. And Bitcoin can be easily traded in and used to provide access from one theme park (country) to the next.

Network effects

Like email, Bitcoin is being driven by network effects. The more capital that gets invested into Bitcoin, the larger the ecosystem becomes.

Bitcoin’s success is driving its own success. This extends into the political realm.

Pro-Bitcoin voters, who skew young, are motivated and have become influential, no doubt affecting the current administration’s pro-Bitcoin stance.

Bitcoin’s growth as an asset is also driving more innovation and new business models. We now have a rapidly growing collection of Bitcoin Treasury Companies that pursue various strategies involving Bitcoin as the core asset.

Will AI accelerate adoption?

The proliferation of Bitcoin and crypto generally coincides with huge advances in artificial intelligence.

Elon Musk’s xAI launched Grok4 in recent days, which represents a significant leap forward in AI processing capability.

All the major tech platforms are competing aggressively to have the most robust AI capability. Anyone who plays with AI services like OpenAI’s ChatGPT and Google’s Gemini can appreciate the rapid progress now being made in AI.

As we discussed in How to Use AI to Become a Better Investor, we highly recommend becoming familiar with these services as they get better and better with each passing day for a wide range of uses.

AI is arguably the next major frontier for Bitcoin.

An AI agent is like a virtual assistant—an autonomous software system that takes actions to achieve specific goals with little or no human input. It makes decisions based on rules, learned behavior and real-time data.

The financial services industry, including even money management, is making rapid advances in deploying AI agents across a wide range of purposes.

Bitcoin is more likely to be used by AI agents than fiat because it’s programmable, permissionless and available around the clock. It enables instant, borderless, low-cost transactions without banks or intermediaries.

Purely digital actors need purely digital money. Fiat money is poorly suited for autonomous agents that engage in real-time, global, machine-to-machine financial interactions.

Major financial institutions are now spending billions of dollars on AI agents. As AI changes the nature of financial transactions, this represents yet another tailwind for purely digital money.

Thoughts on allocation

Bitcoin maximalists recommend you put every last cent into Bitcoin. They obviously have high conviction in Bitcoin’s success and the likelihood of seeing massive additional price appreciation.

Bitcoin skeptics recommend no allocation at all. They expect it will ultimately be worthless.

We find both positions equally irrational.

The Bitcoin story is extremely promising, but it is not risk-free. As with any investment, especially one linked to technology, something can go wrong.

Bitcoin could fail. If it does, an investor who had all his eggs in the Bitcoin basket would also fail.

Meanwhile, if Bitcoin’s value is truly going to soar, one does not need to take such extreme risk to get the benefit of the upside. A sizeable (rather than total) investment should do the trick.

By the same token, having zero exposure to Bitcoin could be a problem if Bitcoin truly takes over in the decades ahead.

Investors should think about this defensively, not just in terms of chasing upside. In a world where monetary value shifts in the direction of a new form of money, if you are stuck in the less valuable money, you will have less.

A good analogy could be citizens in a country where the currency collapsed because the government went under.

The citizens who took their cash and bought American dollars, or gold, or anything else, would have survived, whereas the ones who only had bank accounts in the destroyed currency were left with nothing.

To some extent, in the battle over the future of money, it is a zero sum game.

Position sizing

If Bitcoin were a stock, its current market capitalization would make it about a 4% allocation within the S&P 500. That strikes us as a reasonable reference point in terms of a potential weighting within a portfolio relative to the portfolio’s overall equity exposure.

For example, if someone had 70% of his assets in stocks, this would translate into an approximate 2.8% allocation to Bitcoin (4% of 70%).

Investors can work from there to figure out an appropriate allocation relative to their conviction level in Bitcoin’s growth and their tolerance level for Bitcoin’s volatility.

There is one critical factor to consider, especially if Bitcoin ends up being a relatively small allocation, for whatever reason.

In order to benefit from the hyper-bitcoinization scenario, an investor would need to hold his Bitcoin along the way, rather than rebalance and reduce the position as it appreciates.

To be positioned for the Bitcoin dominance scenario, whether or not it occurs, one needs to own it for the long-term rather than take profits as it rises.

The probability of hyper-bitcoinization is impossible to know, but even if one assumes it is quite low, Bitcoin is compelling, even at current levels, from a pure risk-reward perspective.

Given the vast upside potential, even Bitcoin skeptics may want to consider buying some and just forgetting about it.