Two parallel economies

As we recently discussed (Is the Stock Market Too Hot?), the U.S. economy has been splitting into two increasingly disconnected halves.

On the one hand, you have the red hot high-tech economy, fueled by massive investments in AI and wealth effects. Stocks, especially large cap stocks and tech stocks, tend to represent this part of the economy in a disproportionate way.

On the other hand, you have the economy that is experienced by the average American worker and consumer, which is more connected to food, housing and transportation than AI data center buildouts.

The post-Covid inflation wave, which was a function of very easy monetary policy and high deficit spending during the Biden era, is the reason the Fed was forced to make a hard pivot in the direction of high interest rates.

Working and middle class Americans are now dealing with the consequences of this as they struggle with high interest rates on homes, cars and credit card balances.

The Fed’s intention in hiking interest rates was always to suppress consumer demand and slow the economy down. With labor market growth potentially stalling, especially in rate sensitive sectors like housing, it may now be time to provide ordinary Americans some relief.

But the Fed cannot cut interest rates for some businesses and consumers and not others. Even though the high-tech economy probably does not need additional stimulus, it appears to be on its way.

Hints of fiscal dominance

Fiscal dominance, a concept we have been writing about for some time, is getting more attention recently, including in the reaction to Powell’s speech.

The basic idea behind fiscal dominance is that the central bank loses independence and becomes beholden to the fiscal predicament of the national government.

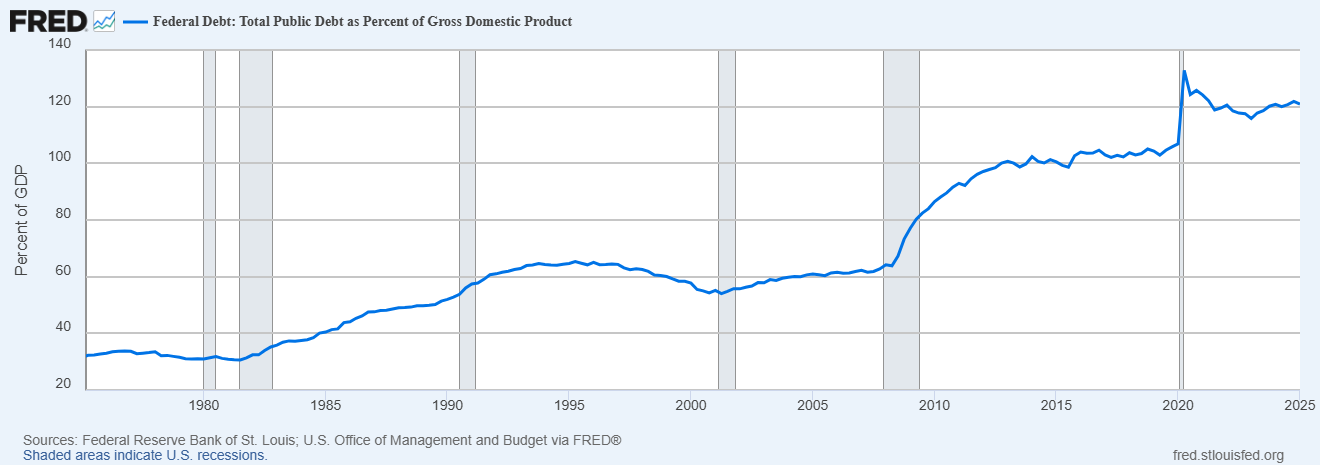

While fiscal dominance is historically a phenomenon that affects highly indebted third world countries, the United States now has some $37 trillion of federal debt and generationally high (and growing) debt-to-GDP.